Key Stats for Qualys Stock

- Past-Week Performance: -5%

- 52-Week Range: $85 to $155

- Current Price: $87

What Happened?

Qualys stock (QLYS) sits dangerously close to its 52-week low of $85.14, with shares trading at $88.25 on February 24, a 43.3% collapse from the $155.47 peak that signals the market is aggressively repricing this cybersecurity platform’s near-term growth story despite a Q4 earnings beat across every major metric.

Selling pressure intensified after Qualys delivered its February 5 earnings report, where management guided full-year revenue to $717M–$725M, implying a deceleration to 7%–8% growth from the 10% pace it sustained throughout all of fiscal year 2025, prompting analysts holding 16 “hold” ratings to stand firm rather than defend the stock.

The deceleration concerns stem from Qualys’ net dollar expansion rate slipping to 103% in Q4, down from 104% the prior quarter, with management explicitly guiding for no material improvement in 2026, signaling that its Enterprise TruRisk Management upsell motion into the existing VMDR customer base has yet to hit a meaningful inflection point.

Despite the selloff, the market’s mental model around Qualys is quietly shifting from a legacy vulnerability management vendor toward an agentic AI-powered risk operations platform, as ETM bookings contributions, Patch Management reaching 8% of total bookings, and the new Agent Val exploit-confirmation workflow collectively reframe Qualys as a pre-breach automation company rather than a scanner.

CEO Sumedh Thakar stated on the Q4 earnings call that “the future of pre-breach risk management belongs to vendor-agnostic agentic AI-powered solutions that continuously predict, assess, confirm, quantify, prioritize and remediate risks across on-prem and multi-cloud environments,” directly positioning Qualys against single-vendor platforms and theoretical-score-only exposure management tools gaining attention through deals like ServiceNow’s Armis acquisition.

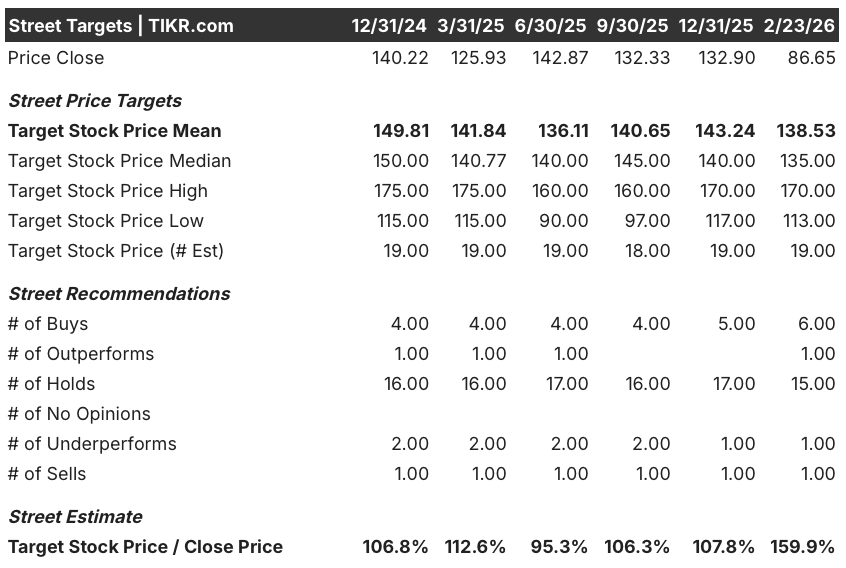

Adding institutional weight to the recovery thesis, Wall Street’s median 12-month price target stands at $140.6, roughly 59.3% above the current $88.25 price, with 6 analysts maintaining buy-equivalent ratings even as the stock trades within $3 of its 52-week floor, suggesting professional conviction that the selloff has overshot fundamentals.

Looking out three to five years, Qualys’ FedRAMP High authorization, its growing mROC partner ecosystem, and its first-mover position in agentic AI exploit validation position it to capture an expanding share of the $53B cybersecurity risk management market as enterprises consolidate fragmented security stacks into unified, autonomous remediation platforms.

Wall Street’s Take on QLYS Stock

That growth deceleration narrative, while real, now trades at a 43.3% discount to its 52-week high, creating a setup where Qualys’ agentic AI platform buildout and FedRAMP High authorization could drive a meaningful re-rating if ETM adoption accelerates through 2026.

Beneath the selloff, the fundamental engine remains intact, with consensus estimates projecting $720M in revenue for fiscal year ending December, a 7.8% increase, while normalized EPS grows to $7.4 and EBITDA margins hold at 44.5%, proving the business model’s durability through the transition.

Wall Street currently prices Qualys at a mean target of $138.5 across 19 analysts, representing 59.9% upside from the February 23 close of $86.7, with 6 buys and 1 outperform rating suggesting a growing minority of analysts see the selloff as a mispricing rather than a fair verdict.

Notably, the target range spans from a low of $113 to a high of $170, a $57 spread that reflects genuine disagreement over whether Qualys’ ETM upsell motion will inflect meaningfully in 2026 or remain a slow-burn story requiring another full year of execution to validate.

What Does the Valuation Model Say?

Even accounting for continued P/E multiple compression of 8.6% annually, TIKR’s mid-case valuation model prices Qualys at $114.6 by December 2030, delivering a 32.3% total return and a 5.9% annualized IRR from current levels, suggesting the market has already priced in substantial disappointment.

The primary risk remains pipeline conversion, as management explicitly guided for no material improvement in the 103% net dollar expansion rate, meaning the ETM upsell thesis depends entirely on unproven acceleration from a partner ecosystem and QFlex pricing model still operating in beta.

At $88.3 with a 5.9% annualized IRR in the base case and 59.9% upside to Wall Street’s mean target, Qualys looks undervalued for patient investors who believe the agentic AI risk operations story is early rather than broken.Qualys just beat Q4 estimates across every major metric, but the real story isn’t what happened in the quarter, it’s whether ETM adoption inflects in 2026 and forces a complete repricing of a stock sitting dangerously near its 52-week floor.

Should You Invest in Qualys, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Qualys stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Qualys, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze Qualys stock on TIKR for Free →