Key Stats for Seagate Stock

- Current Price: $968.53

- Target Price (Mid): ~$2,770

- Street Target: ~$930

- Potential Total Return: ~186%

- Annualized IRR: ~30% / year

- Earnings Reaction: +11.10% (April 28, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Seagate Technology Holdings (STX) spent the last week of June behaving like two different stocks. On June 26 it fell 12% in a single session as the AI storage trade unwound. Three days later, on June 29, it jumped 7.63% to close at $968.53, its best day in weeks. Nothing changed at the company in between. What changed was that Wall Street put a new number on the table.

That number was $1,600. The whipsaw is the story, and it leaves the Seagate stock 2026 debate sitting on a single uncomfortable question. After a 250%-plus run this year, is a stock at $969 still cheap, or is the market handing out top-tick targets right as the cycle peaks? Bulls see locked-in demand and margins that keep climbing. Bears see a hardware maker priced at nearly 40 times forward earnings, a level the market has never paid for this business before. Both can point to real evidence, and the next earnings print is still weeks away.

The $1,600 call that sparked the bounce

The catalyst was specific. On June 29, Melius Research analyst Ben Reitzes initiated coverage of Seagate with a Buy rating and a $1,600 price target, the highest on the Street. His logic leaned directly into the selloff that preceded it. Both Seagate and Western Digital had dropped more than 20% from recent highs, and for an AI infrastructure bull, Reitzes argued, that pullback was the entry point rather than a warning. He thinks hard disk drive (HDD) gross margins, currently in the 50% range, can climb past 65% as the storage shortage holds. Cantor Fitzgerald reinforced the move the same day, lifting its target to $1,300 from $1,000 while keeping an Overweight rating.

Why it matters: a 7.6% pop on an analyst note, with no earnings and no product news, tells you how tightly this stock now trades to the AI-infrastructure narrative rather than to its own quarterly results.

The bullish case does not rest on analyst enthusiasm alone. It rests on visibility that most hardware companies never get. Speaking at the Bank of America 2026 Global Technology Conference on June 2, EVP and CFO Gianluca Romano described a demand picture with unusual precision. “For the next 4 to 5 quarters, we have orders in place and an order has a precise mix, precise exabyte volume, precise price and time to deliver,” he said. That is a backlog, not a forecast, and it covers roughly the next year.

See historical and forward estimates for Seagate stock (It’s free!) >>>

Why the fundamentals keep validating the bulls

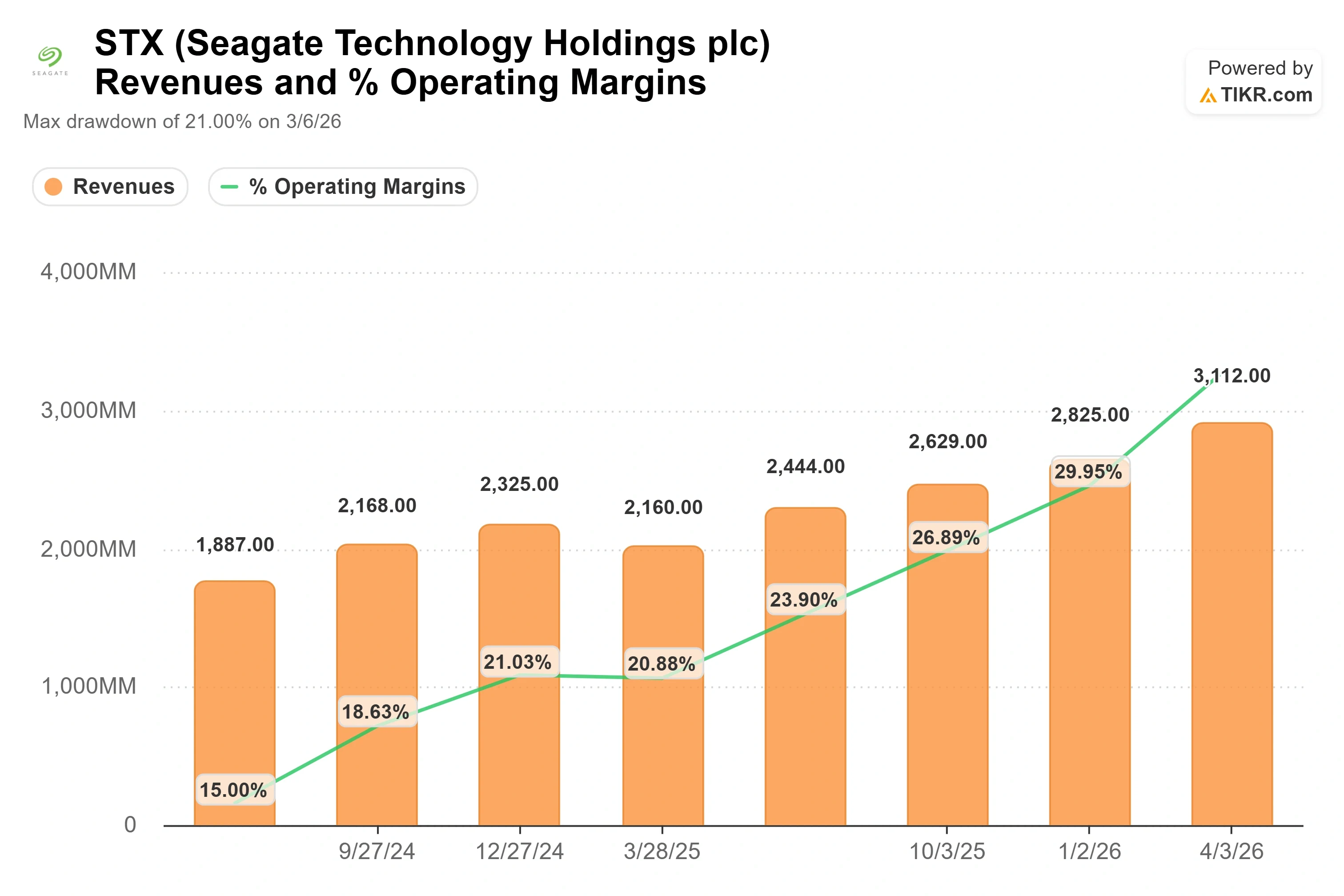

The April quarter is what analysts keep pointing back to. Seagate reported fiscal Q3 2026 revenue of $3.11 billion, up 44% year over year, and the stock jumped 11.10% on April 28. It was the fourth straight earnings beat. Net income came in at $934 million, beating the consensus estimate by 15.76%, and non-GAAP gross margin reached 47%, a level the company had never sustained before this cycle.

The driver behind those margins is the part that makes this cycle look structural rather than cyclical. Seagate is growing the data it can ship without building new factories. Its HAMR (heat-assisted magnetic recording) drives, which pack more terabytes onto each disk, let the same manufacturing footprint produce roughly 25% more exabytes every year. Romano was blunt about the discipline holding it together: the industry is “very disciplined in how we add exabyte capacity and not adding units.” That is the whole game. More capacity from the same cost base is how gross margin expands quarter after quarter.

Demand, by management’s account, is running ahead of supply rather than catching up to it. “Demand is probably higher than what we were expecting a year ago or 6 months ago,” Romano told the BofA audience. Roughly 80% of the business is now data center, and most of that volume is committed under contract. The uncommitted slice is where pricing can still surprise to the upside, because, as Romano put it, “demand is way above supply.”

The case for caution at $969

None of that makes the stock cheap, and that is the other half of the debate. Even after the recent pullback, STX trades at an NTM EV/EBITDA (next-twelve-months enterprise value to earnings before interest, taxes, depreciation, and amortization) of around 31x and a forward price-to-earnings ratio near 40x. For a business, the market has always been treated as cyclical, that is, a steep multiple. The premium only holds if the AI storage cycle proves durable.

Not everyone on the Street is convinced it will. On June 22, Fox Advisors downgraded Seagate to Equal-Weight, warning that expectations for HDD pricing “may be getting ahead” of likely increases. That is the bear case in one sentence: the stock has already priced in years of pricing power that have not been booked yet. The insider picture adds a smaller note of caution. Seagate insiders sold roughly $108 million to $113 million in stock over the three months through June, and bought none. The most recent executive sales, including the CFO’s June trades, were small sell-to-cover transactions executed under a pre-arranged 10b5-1 plan rather than discretionary calls on the stock, so those specific trades carry little signal. The absence of any insider buying during a historic run is the more notable part.

The competitor picture frames the valuation question cleanly. On NTM P/E, Seagate sits around 40x against Western Digital, its closest HDD peer, near 41x. The two storage leaders trade as a pair, which suggests the market is pricing a shared thesis rather than singling Seagate out for excess optimism. The rest of the hardware group sits far below: NetApp near 17x, Dell near 22x, and Samsung near 6x. The premium to that broader group is real and entirely deliberate. It is a bet that storage is no longer just hardware but AI infrastructure. If that bet is right, the multiple is defensible. If hyperscale capital spending plateaus, it unwinds fast.

See how Seagate performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $968.53

- Target Price (Mid): ~$2,770

- Potential Total Return: ~186%

- Annualized IRR: ~30% / year

See analysts’ growth forecasts and price targets for Seagate stock (It’s free!) >>>

This analysis uses the TIKR model’s mid case, realized at June 30, 2030, a four-year horizon. On those assumptions, fair value lands near $2,770, well above any current Street target, for roughly 186% total return and about a 30% annualized IRR.

Two drivers carry the revenue line. The first is exabyte growth from the HAMR roadmap, as Mozaic-based drives move from 40 terabytes toward 50, supporting a mid-case revenue CAGR of around 22%. The second is pricing on uncommitted volume, where demand runs above supply, letting Seagate take measured price increases on top of the contracted base. The margin driver is operating leverage on a structurally flat unit-cost base, which carries the mid-case net income margin to around 43%. The primary risk is a macro cycle that cuts hyperscale capital spending, the one external factor Romano named as able to break the trend.

The upside is that order-backed demand and density gains compound for years, and the stock grows into its premium. The downside is that AI spending plateaus, pricing discipline cracks, and a 30x EBITDA multiple unwinds quickly. The model’s wide range, from a low case well under the mid to a high case far above it, reflects exactly how much rides on that single variable.

Conclusion

The number to watch is gross margin, and the date is the fiscal Q4 2026 earnings report, expected around July 16, 2026. Seagate printed a 47% non-GAAP gross margin in the April quarter. Reitzes is betting that the figure marches toward 65% over time, and the entire $1,600 thesis depends on that path being real rather than aspirational. A Q4 gross margin holding at or above 47%, with management reaffirming order visibility into fiscal 2028, would confirm the structural-growth story and make the premium multiple look earned. A sequential margin dip, or any softening in the order book commentary, would hand the Fox Advisors bears their evidence that pricing got ahead of itself. At $969, the stock is priced for the first outcome. Late July is when investors find out which one they are getting.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Seagate?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Seagate, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Seagate alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Seagate on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!