Key Stats for CRM Stock

- Past week’s performance: Consolidating

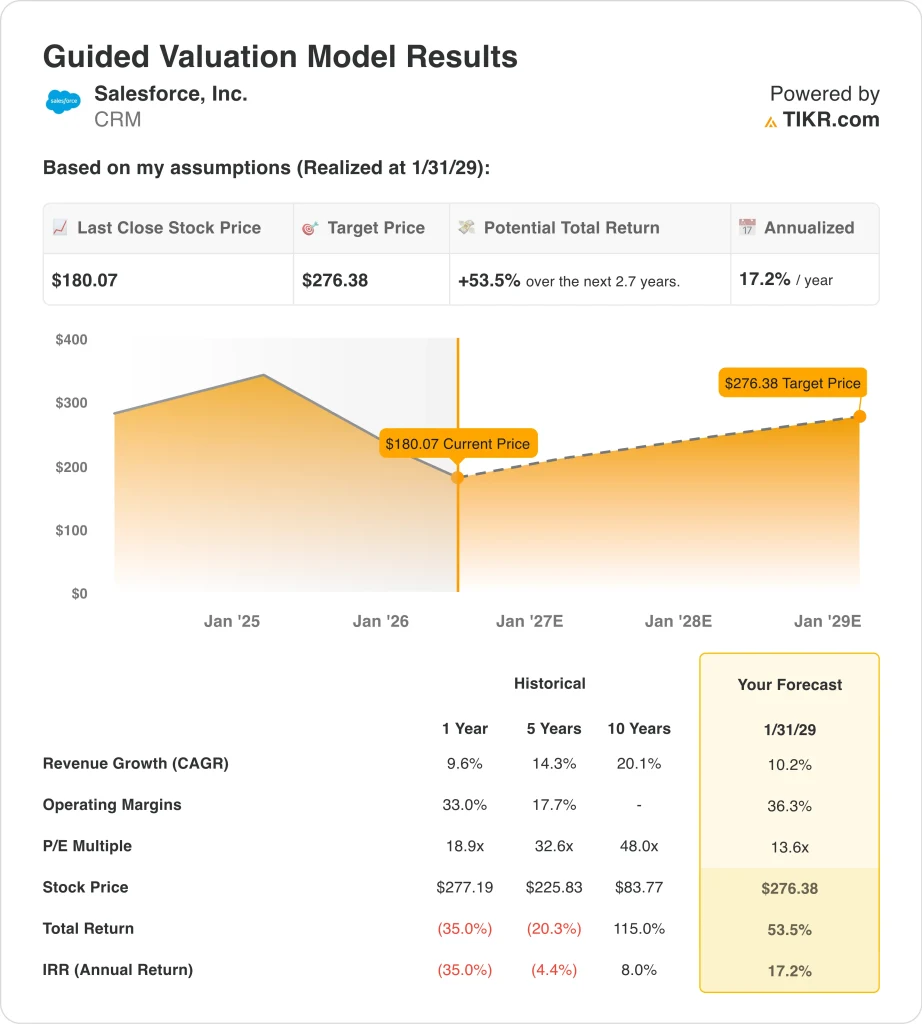

- 52-week range: $164 to $279

- Valuation model target price: $276

- Implied upside: +53.5% over 2.7 years

Value your favorite stocks like CRM with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Salesforce (CRM) gained less than 1% over the past week. But the broader context matters more here. The stock has fallen roughly 35% from its 52-week high of $279. That places it near the lower end of its annual trading range.

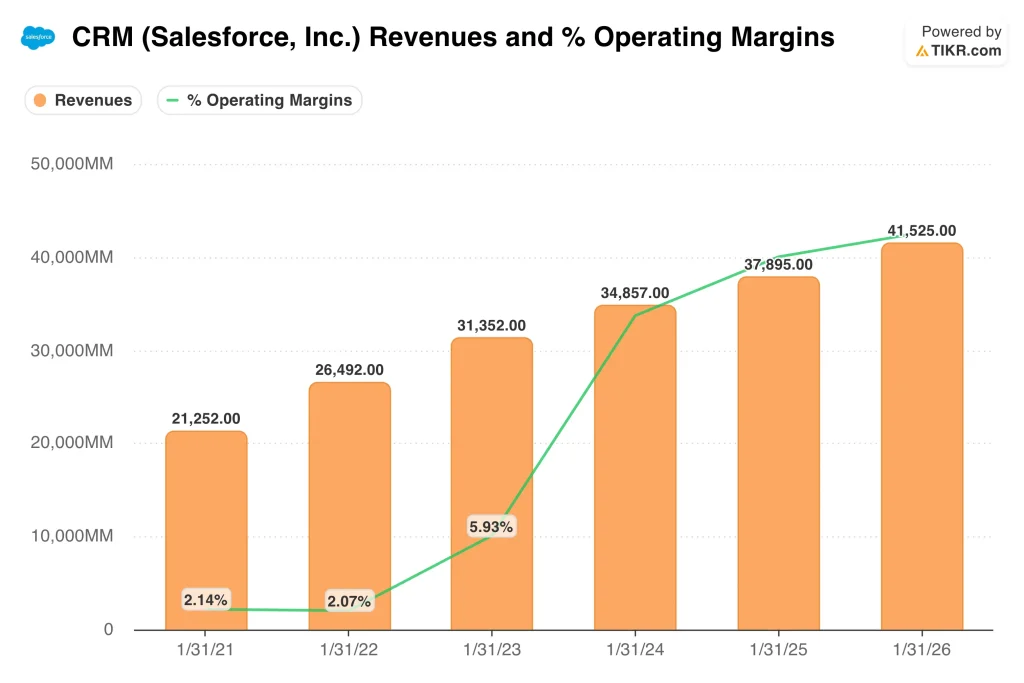

The decline reflects investor frustration with slowing revenue growth. Investors are also questioning whether Agentforce, Salesforce’s AI agent platform, can reaccelerate the business. Q1 fiscal 2027 earnings on May 27 represent the next major inflection point.

Recent news offered a mix of strategic progress and headwinds. Salesforce’s Informatica platform deepened its collaboration with Microsoft to deliver trusted data for agentic AI applications in May 2026. Agentic AI refers to software systems that can autonomously plan and execute multi-step business tasks.

Pierre Fabre, a global pharmaceutical company, also selected Salesforce Agentforce Life Sciences for its customer engagement platform. A new Salesforce report showed that AI agent adoption in customer service rose to 66% in 2026. That result suggests broad enterprise interest in the technology.

However, Starboard Value LP dissolved its entire stake in Salesforce in May 2026. Starboard is a well-known activist investor that has been pushing for improved operational performance. The exit removes a shareholder that was holding management publicly accountable for execution.

Salesforce also conducted another round of workforce reductions in February 2026, reflecting ongoing cost management efforts. Both developments weighed on sentiment during a period when investors were already cautious about the stock.

Going forward, the May 27 earnings report will be critical. Agentforce paid deal counts and remaining performance obligation growth are the two metrics investors will watch most closely.

See analysts’ growth forecasts and price targets for CRM (It’s free) >>>

Is CRM Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 10.2%

- Operating Margins: 36.3%

- Exit P/E Multiple: 13.6x

Based on these inputs, the model estimates a target price of $276, implying 53.5% total upside from the current share price and a 17.2% annualized return over the next 2.7 years.

A 17.2% annualized return places Salesforce among stocks the model views as genuinely undervalued. The stock trades at roughly 23x trailing earnings and approximately 14x forward earnings. Salesforce has historically traded above 30x forward earnings during periods of strong revenue growth. So the current compression represents a meaningful discount to the stock’s own history.

The model’s exit P/E of 13.6x is actually below the current forward P/E. That is a conservative assumption for a business with 77.7% LTM gross margins. Margins at that level are among the highest in enterprise software. They confirm the underlying business quality despite the stock’s recent decline. Any rerating toward historical multiples would add significant upside beyond the model’s base case.

Competitors like ServiceNow and Microsoft Dynamics are also competing for AI-powered enterprise software budgets. But Salesforce’s CRM market leadership and customer base of over 150,000 organizations create significant switching costs.

The $25 billion share repurchase launched in March 2026 could meaningfully reduce the share count over time. Fewer shares outstanding mechanically raise earnings per share, making the stock appear cheaper even without an improvement in absolute earnings.

What’s Driving CRM Stock Going Forward?

The Q1 fiscal 2027 earnings report on May 27 is the most immediate catalyst. Investors will focus on Agentforce paid deal counts, remaining performance obligation growth, and full-year revenue guidance.

The remaining performance obligation (RPO) is the total value of contracted future revenue not yet recognized. RPO growth serves as a leading indicator of business momentum. A strong RPO result would be a significant positive signal for the stock.

Salesforce is also in active acquisition mode. The company signed a definitive agreement to acquire Momentum in February 2026. That followed the earlier acquisition of Doti in November 2025.

These acquisitions add capabilities to the Salesforce platform and could accelerate Agentforce adoption across industries. Management commentary on integration progress will offer clues about how quickly acquired capabilities can contribute to revenue.

The $25 billion accelerated share repurchase announced in March 2026 is a significant capital allocation signal. At a share price near $180, Salesforce can retire a large number of its approximately 818 million shares outstanding. Fewer shares outstanding mechanically raise earnings per share.

That improvement can attract value-focused institutional investors even if absolute earnings do not change. Over time, the buyback becomes a compounding benefit for long-term shareholders. Long-term, the Informatica partnership with Microsoft positions Salesforce as a critical data layer for enterprise AI deployments.

If businesses broadly adopt AI agents for customer service, sales automation, and operations, Salesforce’s platform becomes increasingly essential. That secular trend underpins the bull case. It also justifies the model’s optimism about a stock trading far below its historical peak.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Salesforce, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CRM, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CRM alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze CRM stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!