Key Stats for VST Stock

- Past week’s performance: 14.3%

- 52-week range: $133 to $220

- Valuation model target price: $231

- Implied upside: +47.9% over 2.6 years

Value your favorite stocks like VST with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

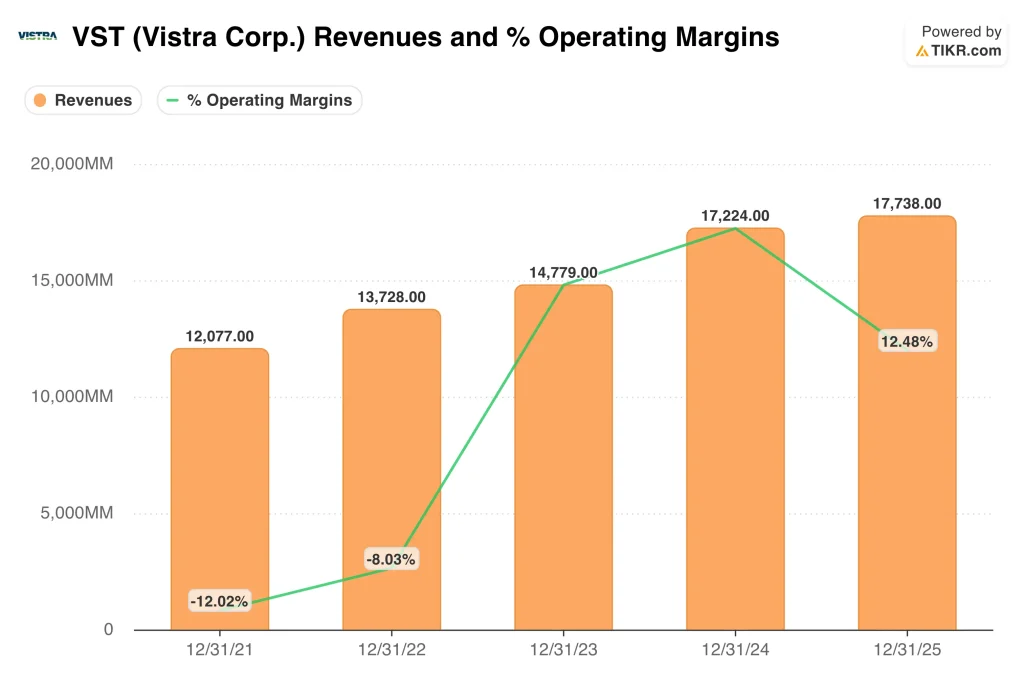

Vistra (VST) surged about 14% over the past week. The primary driver was a strong Q1 fiscal 2026 earnings report released on May 7. The company reported net income of $1.03 billion for Q1, swinging from a loss in the prior year. Revenue rose to $5.64 billion, slightly missing the $5.65 billion analyst estimate due to weather impacts. But the profit reversal dominated the investor narrative.

Vistra generates electricity from natural gas, nuclear, and coal plants and sells it to wholesale markets and retail customers. When electricity demand and prices rise, Vistra’s large generation fleet captures significant upside. The company’s nuclear fleet is especially valuable because it delivers low-cost electricity without fuel price risk. AI data center expansion is driving that demand surge, and Vistra sits at the center of it.

The broader power sector received additional positive news this week. Reuters reported that NextEra and Dominion are exploring a potential merger, extending the U.S. utility M&A wave into 2026. That deal activity raises perceived valuations across the power generation sector broadly.

Fitch Ratings also upgraded Vistra to BBB- investment grade in March 2026. That upgrade reduces borrowing costs and signals improved financial stability to investors. If VST stock continues to benefit from AI power demand growth, rising revenues, and investment-grade credit could sustain the momentum.

See analysts’ growth forecasts and price targets for VST (It’s free) >>>

Is VST Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 14.7%

- Operating Margins: 22.9%

- Exit P/E Multiple: 17x

Based on these inputs, the model estimates a target price of $231, implying 47.9% total upside from the current share price and a 16.2% annualized return over the next 2.6 years.

A 16.2% annualized return places Vistra firmly among stocks the model views as genuinely undervalued. The stock currently trades about 29% below its 52-week high of $220. That pullback from the peak creates the return opportunity the model is capturing. Importantly, the fundamental driver of AI-driven electricity demand has not diminished since the stock fell from its highs. The gap between business momentum and stock price is what makes the setup interesting.

Vistra’s trailing gross margin is 38.6%, which is strong for a power generation company. The forward EV/EBITDA sits around 9.8x. EV/EBITDA compares a company’s total enterprise value to its earnings before interest, taxes, depreciation, and amortization. Investors commonly use it as a standard valuation metric for capital-intensive businesses. A sub-10x EV/EBITDA looks modest relative to Vistra’s 14.7% revenue growth forecast.

Competitors like Constellation Energy also operate large nuclear fleets and have attracted premium valuations from AI-demand investors. Vistra’s diversified generation mix and retail electricity segment could close that valuation gap over time. The Fitch upgrade to investment grade broadens the potential investor base and reduces financing costs. Both of those improvements directly support the case for a higher earnings multiple over the next several years.

What’s Driving VST Stock Going Forward?

AI data center expansion is the most powerful external tailwind for Vistra. As hyperscalers build massive computing facilities, their electricity consumption is growing rapidly. Natural gas and nuclear generation are the primary solutions for meeting 24-hour baseload power demand. Vistra operates a large fleet of both types. So it is well-positioned to benefit from new power purchase agreements with technology companies.

The company completed a $4 billion senior notes offering in April 2026 to fund continued infrastructure investment. Management stated that full delivery of existing Meta power purchase agreements would significantly lift free cash flow before growth capital.

Free cash flow before growth capital is the cash a business generates from existing operations before new project spending. That metric is particularly important for capital-intensive power generators.

The Cogentrix acquisition, completed in January 2026, added natural gas and wind power capacity primarily in the eastern United States. That deal expanded Vistra’s geographic footprint beyond its traditional Texas and Midwest markets.

Management cited it as strategically aligned with its growing data center power business. Broader geographic reach also reduces weather-related revenue concentration risk. The Q2 2026 earnings call is expected around August 5. Investors will focus on summer power demand trends and any new commercial agreements with data center customers.

Regulatory developments around nuclear power credits and clean energy policy will also influence the longer-term earnings trajectory. A favorable policy on nuclear power would be an especially significant catalyst for Vistra’s nuclear fleet.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Vistra?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up VST, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track VST alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze VST stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!