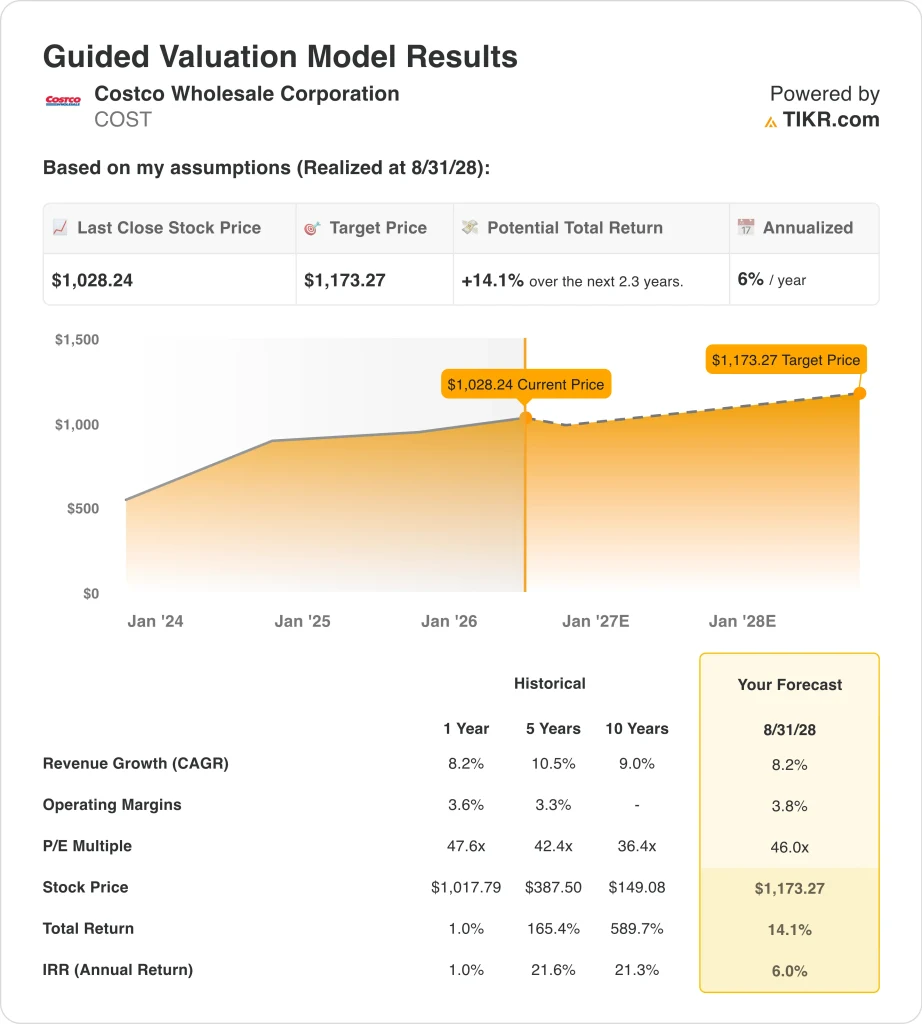

Key Stats for COST Stock

- Past week’s performance: -4.5%

- 52-week range: $844 to $1,097

- Valuation model target price: $1,173

- Implied upside: +14.1% over 2.3 years

Value your favorite stocks like COST with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Costco (COST) fell about 4.5% over the past week. No single negative catalyst drove the decline. Instead, investors appear to be de-risking ahead of Q3 fiscal 2026 earnings, scheduled for May 28. Premium-valued stocks often see profit-taking before major reporting dates, and Costco fits that profile precisely.

April sales data were actually encouraging. Costco reported April net sales of $23.92 billion, a 13% increase from the prior year. That result reinforced confidence in the membership model and the resilience of Costco’s value-focused retail approach.

Costco operates warehouse clubs where members pay annual fees for access to bulk merchandise at low prices. Those membership fees are high-margin and recurring, forming the financial engine behind the company’s premium valuation.

Separately, Costco raised its quarterly cash dividend from $1.30 to $1.47 per share in April 2026, a 13% increase. That increase signals management confidence in the company’s free cash flow generation.

Costco also faced a legal challenge this week. The company urged a U.S. judge to reject a consumer class action related to tariff refunds. The outcome carries modest financial risk and is not expected to materially affect the business.

Going forward, the Q3 fiscal 2026 earnings call on May 28 is the single most important near-term catalyst for COST stock.

See analysts’ growth forecasts and price targets for COST (It’s free) >>>

Is COST Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

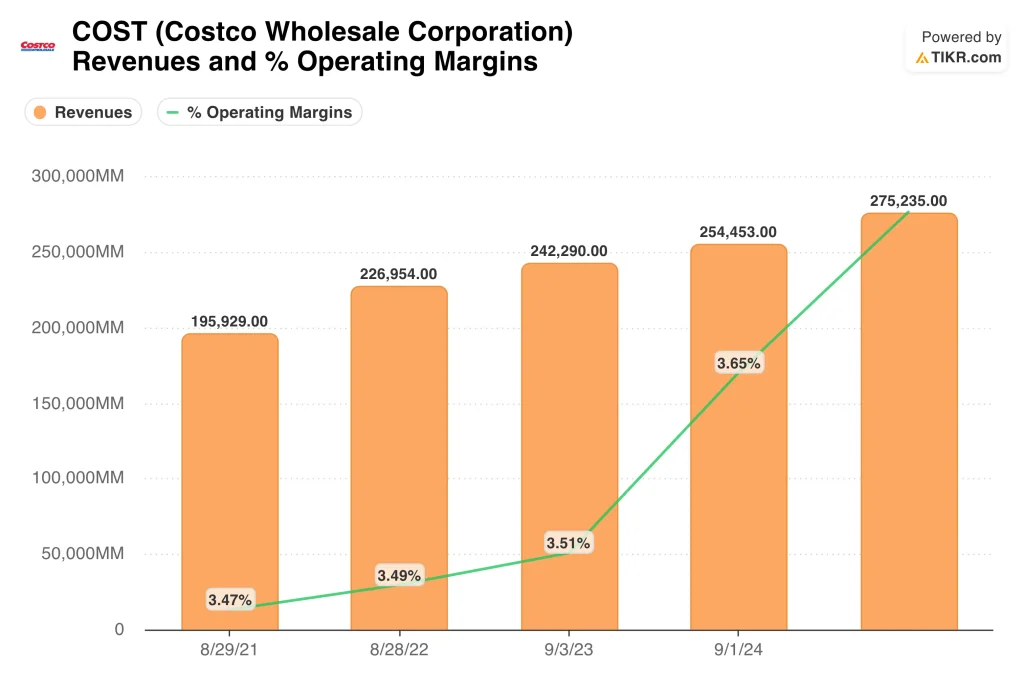

- Revenue growth (CAGR): 8.2%

- Operating Margins: 3.8%

- Exit P/E Multiple: 46x

Based on these inputs, the model estimates a target price of $1,173, implying 14.1% total upside from the current share price and a 6% annualized return over the next 2.3 years.

A 6% annualized return falls below what most investors consider a genuinely attractive opportunity. Costco trades at roughly 48x next-twelve-months earnings, one of the highest multiples among large-cap retailers. That premium reflects exceptional business quality. But it leaves limited room for error if growth disappoints or the macro environment softens. The model’s target requires near-perfect execution on the existing growth and margin trajectory.

Operating margins near 3.8% look thin, but they are intentional. Costco keeps merchandise margins deliberately low to attract and retain members. The real profit engine is annual membership fee income. With over 77 million paid memberships globally, that recurring fee stream is extremely predictable and high margin. That structural quality is what justifies a premium multiple relative to traditional retailers like Walmart.

The model’s exit P/E of 46x is only modestly below the current forward multiple. That limits the valuation expansion story. Costco’s five-year average P/E has been closer to 42x. The stock currently trades at a premium even to its own history. Walmart, a close competitor, trades at a lower multiple and has been posting comparable revenue growth. At current levels, the risk-reward is not especially compelling for new investors.

What’s Driving COST Stock Going Forward?

The Q3 fiscal 2026 earnings call on May 28 is the most immediate catalyst. Analysts will focus on membership renewal rates, same-warehouse sales growth, and any update on international expansion. Costco’s renewal rate has historically exceeded 90%, and any softening there would be a significant negative signal. E-commerce growth will also draw attention, as Costco continues to build digital channels alongside its warehouse footprint.

Tariff policy remains a background risk for Costco. The company sources a meaningful share of merchandise globally, and higher import tariffs could pressure merchandise margins. Management has navigated supply chain disruptions effectively in the past, but the current tariff environment introduces more uncertainty than typical. The ongoing legal action around tariff refunds adds a small layer of headline risk ahead of earnings.

The dividend increase to $1.47 per share quarterly reflects strong and consistent free cash flow. Costco has a history of issuing special dividends to return excess capital to shareholders. If May 28 results show continued strength in membership income and tight cost control, management could signal additional capital returns.

Long-term, international expansion into Asia and Europe provides a meaningful growth runway. New warehouse openings in underpenetrated markets generate membership fee revenue for decades and carry high returns on invested capital.

The core membership model is one of the most durable business structures in retail. That durability supports the long-term investment case even at a premium valuation. Costco’s ability to replicate the model internationally is the key variable to watch over the next several years.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Costco Wholesale Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up COST, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track COST alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze COST stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!