Key Stats for Ralph Lauren Stock

- Current Price: $378 (May 22, 2026)

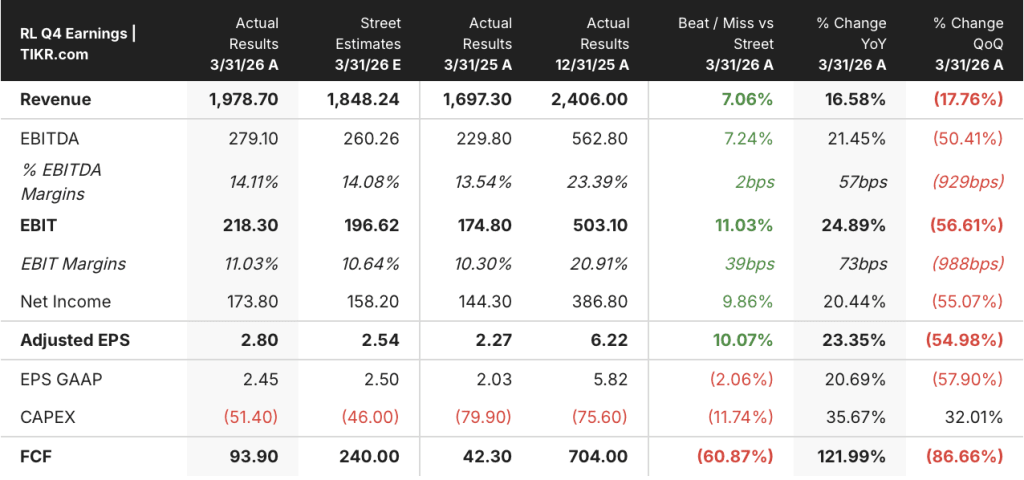

- Q4 FY2026 Revenue: $1.98B, +16.6% YoY

- Q4 FY2026 Adjusted EPS: $2.80, +23.4% YoY

- Full Year FY2026 Revenue: Surpassed $8B for the first time

- Full Year FY2026 Operating Margin: 15.4% (constant currency), +140 bps YoY

- FY2027 Revenue Guidance: Mid-single digits, centered around 4% to 5%

- FY2027 Operating Margin Guidance: +40 to +60 bps expansion (constant currency)

- TIKR Model Price Target: $500

- Implied Upside: ~33%

Ralph Lauren Crosses $8B in Revenue With China Up 51% and Every Region Beating Plan

Ralph Lauren Corporation (RL) posted Q4 FY2026 revenue of $1.98B, up 16.6% year-over-year and ahead of Street estimates of $1.85B, with adjusted EPS of $2.80 beating the prior year’s $2.27 by 23%, following its May 21 earnings release.

The result closed out a full year in which Ralph Lauren stock surpassed $8B in reported revenue for the first time, with operating margin expanding 140 basis points in constant currency to 15.4%, ahead of the company’s own plan.

Asia led Q4 with revenue up 28%, and China alone accelerated to more than 50% growth in the quarter, supported by a strong Lunar New Year activation, continued expansion across the top 6 city clusters, and scaling on Douyin.

North America grew 8% in Q4, ahead of both the company’s outlook and its three-year Next Great Chapter: Drive targets, driven by 14% direct-to-consumer growth and digital comps up 21%.

Global retail comps increased 17% in Q4, accelerating from the prior quarter, with AUR up 16% — roughly half from stronger full-price selling and reduced discounting, and half from favorable product, channel, and geographic mix.

Patrice Louvet, President and CEO, stated on the Q4 earnings call that “both our top and bottom line results exceeded expectations, supported by our diversified drivers of growth and our strongest quality of sales to date.”

High-potential categories including women’s apparel, outerwear, and handbags grew more than 20% for both Q4 and the full year, outpacing total company growth, with women’s apparel representing roughly $2B in revenue at approximately 1% market share.

Marketing spend reached 7.9% of full-year sales, up from around 3.5% at the start of the elevation journey, with management guiding to 8% in FY2027 and explicitly stating there is no ceiling on marketing investment as a percentage of revenue as long as ROI holds.

The company generated approximately $750M in free cash flow in FY2026 and returned more than $700M to shareholders through dividends and repurchases, while its board approved a 10% dividend increase.

For FY2027, management guided full-year constant currency revenue growth centered around 4% to 5%, with operating margin expansion of 40 to 60 basis points, and China specifically guided to mid-teens growth as it laps 40% growth from FY2026.

TIKR’s $500 Target on Ralph Lauren Stock Requires Execution, Not a Re-Rating

TIKR’s mid-case valuation model prices Ralph Lauren stock at $500, implying approximately 33% total return from the current price of $378over 5years at an annualized rate of 6% per year.

The mid-case assumes a revenue CAGR of 4.0%, a net income margin of 13.5%, and EPS CAGR of 5.3%, with modest P/E multiple compression of 0.9% annually — a notably benign assumption given that Ralph Lauren stock already trades at a historically elevated multiple following two years of outsized earnings growth.

That compression assumption is the pressure point inside the TIKR target: the model prices in continued margin expansion and steady earnings compounding, but gives back almost nothing on the multiple, which means any macro-driven derating would close the gap to $500 faster than the earnings growth can reopen it.

The FY2026 results sharpen the debate on Ralph Lauren stock to one question: whether the company can sustain mid-single-digit revenue growth in FY2027 while lapping 14.6% revenue growth and 34.5% EPS growth from the prior year.

The TIKR mid-case prices Ralph Lauren stock at $525 at full realization, delivering a 39% total return and 3.8% IRR, a scenario consistent with management’s on-algo guidance of 4% to 5% revenue growth, continued AUR expansion, and operating margin progression toward the mid-teens.

The high case at $629 and 5.9% IRR requires a net income margin of 14.1% and revenue CAGR of 4.4%, conditions that would likely require China to sustain growth above its guided mid-teens rate and high-potential categories to continue outpacing the company average as they did in FY2026.

The low case at $426 and 1.4% IRR captures the scenario where Europe softens beyond current guidance, tariff headwinds in the second half of FY2027 prove more disruptive than the 10% prevailing rate assumed for the first half, and AUR growth normalizes faster than management’s mid-single-digit outlook.

Should You Invest in Ralph Lauren Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Ralph Lauren Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Ralph Lauren Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze RL stock on TIKR for Free →