Key Stats for Qualcomm Stock

- Current Price: $192.52

- Target Price (Mid): ~$238 (model entry price: $205.42)

- Street Mean Target: ~$180

- Potential Total Return (mid case): +15.8% over 4.3 years

- Annualized IRR (mid case): 3.5% / year

- Earnings Reaction: +15.12% (4/29/26)

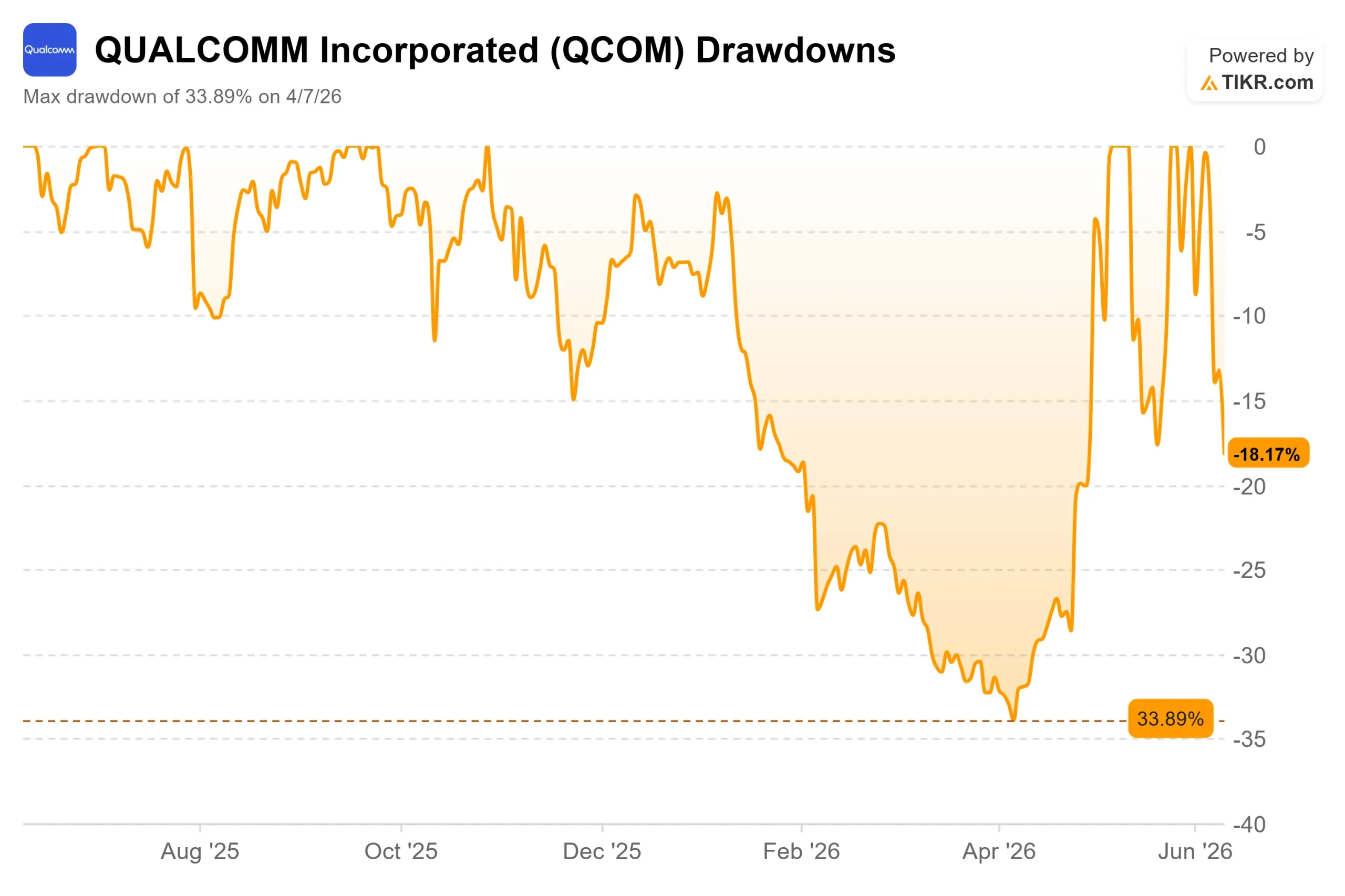

- Max Drawdown: -33.89% (4/7/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Qualcomm Incorporated (QCOM) closed at $192.52 on June 10, down 6.28% on the day and 26% below its 2026 intraday peak of $259.92, per TIKR. The decline caps a volatile stretch of AI-driven rallies and sell-the-news reversals. In 13 days, Qualcomm holds its Investor Day in San Jose. What CEO Cristiano Amon said at the Bernstein conference on May 27 tells investors exactly what to expect, and what the market needs to hear to justify the current price.

Why the Stock Has Sold Off

The selloff has three distinct triggers, none of which changed the underlying business. NVIDIA unveiled its RTX Spark chip at Computex, targeting the same Windows on Arm PC market where Qualcomm’s Snapdragon X competes, sending QCOM down around 11% on June 5. News that ByteDance was moving forward with a custom AI chip deal sparked export-control fears, triggering an additional 8% selloff on June 9. And the stock had already priced in a major Computex announcement that never fully materialized.

What has not changed: automotive crossing a $6 billion annual revenue run rate, a confirmed hyperscaler custom chip engagement with shipments scheduled for December 2026, and an Investor Day that Amon himself has framed as a major reveal.

See historical and forward estimates for Qualcomm stock (It’s free!) >>>

What Amon Said at Bernstein

The May 27 Bernstein conference contains commitments that have not been fully absorbed by the market. Amon confirmed that custom ASIC shipments, originally targeted for fiscal 2027, have been pulled into calendar year 2026. He laid out a three-pillar data center strategy: a custom CPU built for server workloads, an XPU (inference accelerator) that avoids HBM memory in favor of a different architecture, and a custom ASIC business built on IP from the Alphawave acquisition. Asked what “material” data center revenue in fiscal 2027 means for a company of Qualcomm’s size, Amon was direct: “Material has to be in the multiple billions of dollars.”

On the margin question, he gave the clearest commitment yet: “All of those things that we’re doing are going to be operating margin accretive for the company.”

JPMorgan raised its price target from $160 to $265 ahead of the Investor Day, while keeping a Neutral rating. Analyst Samik Chatterjee estimated Qualcomm could target more than $3 billion in data center revenue in fiscal 2027. That is his projection, not company guidance, and June 24 is when Qualcomm must deliver the numbers.

The Business Behind the Headlines

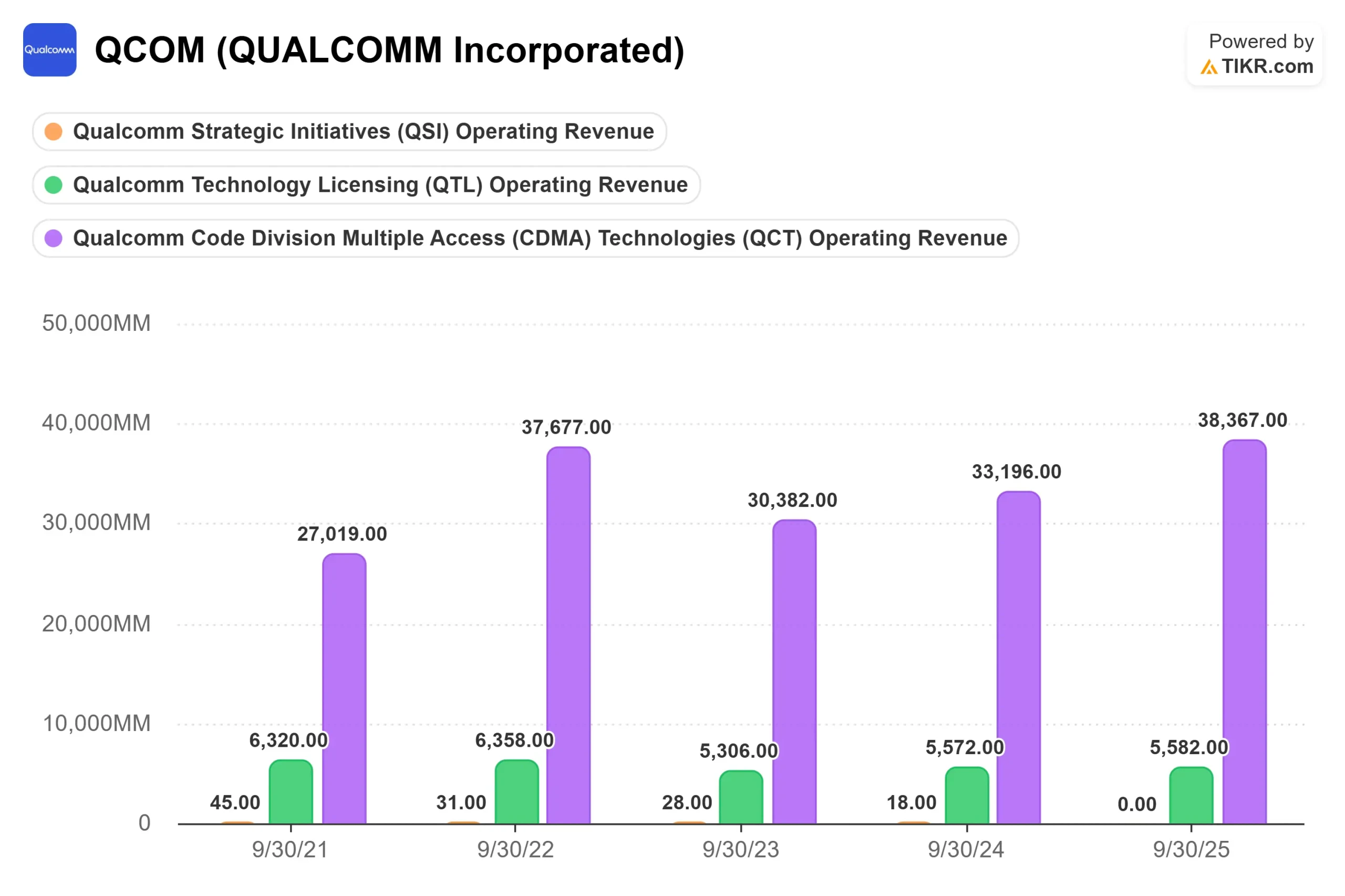

Automotive is the strongest engine in the existing revenue base. Qualcomm’s automotive segment grew 38% year over year to $1.326 billion in Q2 fiscal 2026, per the Q2 fiscal 2026 earnings call, crossing a $5 billion annualized run rate for the first time. Amon guided at Bernstein for a roughly $6 billion run rate by fiscal year-end, with the signed design-win pipeline already exceeding the previously disclosed $45 billion figure.

Handsets remain under pressure, but Amon’s read is supply-driven, not demand-driven. Memory chip inflation has suppressed smartphone production in China, and he said at Bernstein that Qualcomm is “significantly undershipping to consumer demand,” with Q3 fiscal 2026 expected to be the bottom. On Samsung, the Snapdragon baseline share has moved from around 50% historically to “north of 70%.”

IoT is recovering, with management guiding the segment to approximately $1.8 billion next quarter. The personal AI device category, which includes over 40 active designs in smart glasses and related form factors, is where Amon sees the next major volume ramp.

See how Qualcomm performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $192.52

- Target Price (Mid): ~$238

- Potential Total Return (mid case): +15.8% over 4.3 years (model entry: $205.42)

- Annualized IRR (mid case): 3.5% / year

See analysts’ growth forecasts and price targets for Qualcomm stock (It’s free!) >>>

At $192.52, QCOM trades at 21.02x NTM P/E and 15.61x NTM EV/EBITDA, per TIKR. For comparison, Broadcom trades at 24.91x NTM P/E and Nvidia at 20.95x, per TIKR’s Competitors page. Qualcomm’s discount exists because its data center revenue is currently zero. The Street’s mean target of $180.48 sits below the current price, with 22 Holds, 3 Underperforms, and 2 Sells among the 40 analyst recommendations tracked by TIKR, alongside 10 Buys and 2 Outperforms.

The TIKR mid-case model assumes a revenue CAGR of around 5% and a net income margin of around 24%, driven by automotive growth and QTL licensing, which runs at roughly 72% earnings before taxes margin. LTM free cash flow stands at $9.6 billion, per TIKR. These figures reflect the existing business with essentially no value assigned to the data center.

The high-case model projects around $337 with a total return of roughly 64% and an annualized IRR of around 6%, per TIKR. That scenario requires data center revenue scaling into the multi-billion range. The downside: if June 24 disappoints, the stock re-anchors to the handset earnings base and the current multiple contracts meaningfully.

Conclusion

June 24 is the single event that confirms or breaks this thesis. Good looks like named hyperscaler customers, a quantified data center revenue ramp from December 2026 into fiscal 2027, and updated non-handset revenue targets. Anything short of specific numbers is unlikely to hold the premium at $192. The handset’s bottom is priced in. Automotive is on track. What the market needs by the end of June 24 is proof that a data center is a business, not a slide.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Qualcomm?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Qualcomm, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Qualcomm alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Qualcomm on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!