Key Stats for PayPal Stock

- Past-Week Performance: -4.4%

- 52-Week Range: $38.5 to $79.5

- Current Price: $44.9

What Happened?

PayPal‘s board replaced CEO Alex Chriss on February 3 and simultaneously withdrew its 2027 financial targets, shares collapsed 20% in a single session to a 52-week range floor near $38.46, before recovering to $44.90.

The trigger was Q4 2025 earnings, where online branded checkout — PayPal’s core consumer payment button, representing over half of total profit — grew just 1% on a currency-neutral basis, decelerating 4 points from Q3’s 5%, while non-GAAP EPS of $1.23 landed $0.04 below the low end of guidance.

The engine behind the recovery thesis is diversification: Venmo, the peer-to-peer and commerce platform targeting young consumers, grew revenue 20% to $1.7 billion in 2025, Enterprise Payments returned to 12% volume growth in Q4, and Buy Now Pay Later — PayPal’s installment credit product — surpassed $40 billion in annual volume, up more than 20%, collectively driving 6% transaction margin dollar growth even as branded stalled.

Incoming CEO Enrique Lores, who joined March 1 after five years on PayPal’s board, had not yet spoken publicly, but CFO Jamie Miller stated at the Wolfe FinTech Forum on March 10 that Lores “is already hitting the ground running” and brings “faster decision-making, a greater focus on prioritization, and discipline around execution.”

PayPal is simultaneously defending its checkout franchise and opening new transaction channels that did not exist at its prior Investor Day, backed by $6 billion in planned 2026 buybacks, at least $6 billion in guided free cash flow, a PayPal Plus loyalty program launching in the US by mid-2026, and agentic commerce integrations already live on Microsoft Copilot and Perplexity.

Wall Street’s Take on PYPL Stock

The February 3 23%collapse — triggered by a single quarter of 1% branded checkout growth and a withdrawn 2027 outlook — has pushed PYPL to roughly 8.4x 2026 estimated non-GAAP earnings, a multi-year valuation trough for a business that still grew transaction margin dollars 6% and non-GAAP EPS 14% in 2025.

TIKR consensus projects revenue reaching $34.2 billion in 2026 and $35.7 billion in 2027, modest 3% and 4.4% growth rates that already price in the branded checkout drag and the $400 million in planned growth investments management described as a deliberate margin headwind.

At 8.4x forward earnings, PayPal trades at a steep discount to Visa (V), which commands roughly 24x on TIKR’s 2026 normalized EPS estimate of $12.85, despite Visa carrying 70% EBITDA margins versus PayPal’s guided 19.5% — a gap that reflects execution risk, not business extinction.

Wall Street sits cautiously constructive but deeply split: 8 buys, 2 outperforms, 29 holds, and 4 sells among 31 analysts, with a mean price target of $50.23 implying 11.9% upside from $44.90, suggesting the Street is waiting for branded checkout data before recommitting.

The analyst target range spans $32 to $100, and the distance between those poles maps directly to the two outcomes already seeded in the story: full branded checkout recovery under Enrique Lores, or continued deceleration that proves the 2027 target withdrawal was structural, not tactical.

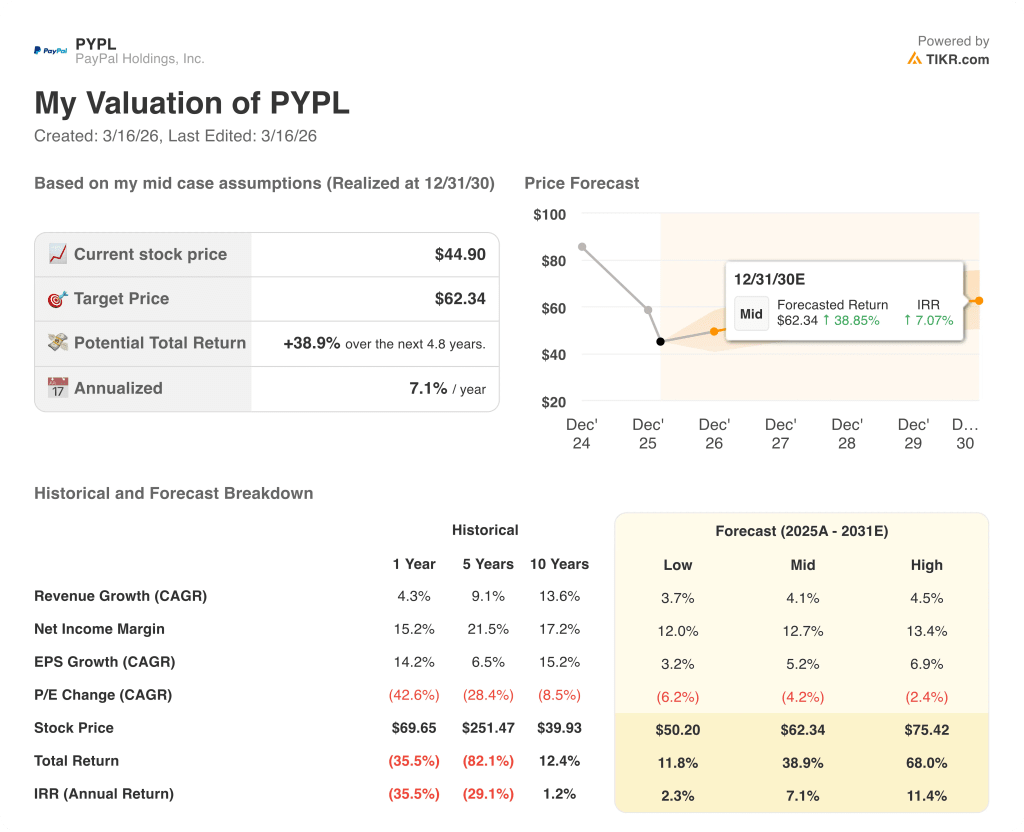

What Does the Valuation Model Say?

TIKR’s mid-case model prices PYPL at $62.34 by December 2030, a 38.9% total return at 7.1% annualized IRR, anchored to 4.1% revenue CAGR and net income margins expanding from 15.5% in 2025 toward 12.7% by the forecast period, supported by the $6 billion annual buyback compressing the share count.

The market is pricing PayPal as a melting branded business, but $6.4 billion in 2025 free cash flow and 14% non-GAAP EPS growth prove the diversification thesis is already working.

Venmo’s 20% revenue growth to $1.7 billion, Enterprise Payments’ return to 12% volume growth, and BNPL’s $40 billion-plus in annual volume are the three operational pillars TIKR’s $62.34 target requires to hold, even before branded checkout inflects.

CFO Jamie Miller confirmed at the March 10 Wolfe FinTech Forum that branded checkout was running “slightly better” than Q4’s 1% through mid-March, a data point too small to celebrate but directionally consistent with the model’s slightly positive to low-single-digit 2026 branded growth assumption.

If branded checkout exits 2026 below the guided slightly positive to low-single-digit range, the $400 million in growth investments produces no in-year return, EBITDA margins compress below the guided 19.5%, and TIKR’s $62.34 mid-case price target becomes indefensible.

Q1 2026 earnings, expected in late April or early May, deliver the first read on whether the March merchant integrations, upstream BNPL presentment, and biometric enrollment campaigns are translating into measurable branded checkout volume acceleration.

Should You Invest in PayPal Holdings, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PYPL stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track PayPal Holdings, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PYPL stock on TIKR for Free →