Key Stats for Dell Stock

- Past-Week Performance: +3.5%

- 52-Week Range: $66.3 to $168.1

- Current Price: $151.6

What Happened?

Dell Technologies (DELL), the hardware giant whose business spans personal computers, AI servers, and enterprise storage, booked $34.1 billion in AI server orders in a single quarter while trading at $151.62, well below its 52-week high of $168.08.

CFO David Kennedy reported Q4 revenue of $33.4 billion on February 26, , up 39%, with diluted non-GAAP EPS of $3.89, up 45%, both company records driven by unprecedented enterprise demand for AI-optimized servers equipped with Nvidia processors.

Dell’s Infrastructure Solutions Group, the division selling servers and storage to data centers, posted record revenue of $19.6 billion, up 73%, while exiting the quarter with a record $43 billion AI backlog, a figure that already exceeds rival HPE’s entire annual revenue guidance.

CEO Jeff Clarke stated on the Q4 FY26 earnings call that “we capped an already strong year with an exceptional quarter for AI, record orders and broad-based demand,” then guided FY27 AI server revenue to $50 billion, roughly doubling the $25.2 billion shipped in FY26.

Dell enters FY27 anchored by that $43 billion backlog, a Board-approved $10 billion buyback expansion, a 20% dividend increase to $2.52 per share annually, and a $140 billion revenue midpoint guidance that implies 23% growth, positioning the company for a fourth consecutive record year.

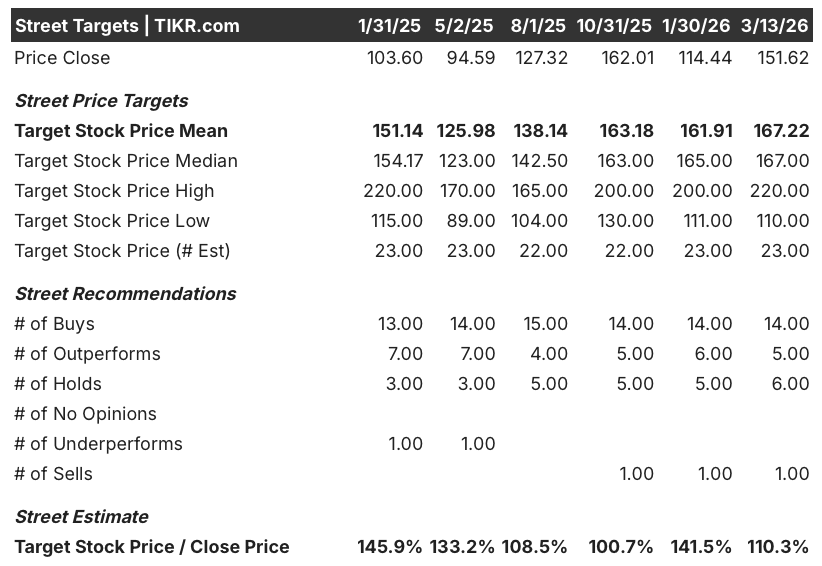

Wall Street’s Take on DELL Stock

The $43 billion AI server backlog Dell carried into FY27 — more than the entire AI revenue it shipped across all of FY26 — reframes this hardware company as a contracted infrastructure compounder, not a cyclical assembler.

Consensus expects revenue to accelerate from $113.5 billion in FY26 to $141.2 billion in FY27, a 24.3% jump anchored by the $50 billion AI server revenue target management guided explicitly, itself supported by $13 billion in Q1 shipments alone.

Analyst sentiment backs the growth case firmly: 14 buys, 5 outperforms, 6 holds, and 1 sell among 26 analysts produce a mean price target of $167.22, implying 10.3% upside from the current $151.62, with the Street pricing in continued AI server share gains and storage margin improvement.

The spread between the low target of $110 and the high of $220 reflects the genuine binary embedded in the story: bears anchor to memory cost inflation eroding CSG and traditional server margins, while bulls price the $43 billion backlog converting at mid-single-digit operating margins through FY27.

What Does the Valuation Model Say?

The TIKR mid-case model prices Dell at $225.33 by January 31, 2031, implying a 48.6% total return, at an 8.4% IRR, using a revenue CAGR of 7.5% and a net income margin of 6.2% — inputs the FY27 guide already partially validates given management’s explicit 23% revenue growth target at the $140 billion midpoint.

The market prices Dell at a discount to that mid-case because it still applies commodity-hardware multiples to a business where 30%-plus of FY27 revenue arrives pre-sold in backlog form.

The $43 billion backlog converting at mid-single-digit AI operating margins supports the TIKR target of $225.33, while the Board-authorized $10 billion buyback and 20% dividend increase signal management’s own confidence in that trajectory.

Additionally, CFO David Kennedy’s statement at the Morgan Stanley TMT Conference on March 4 that the five-quarter pipeline dollar value “has never been higher” confirms the demand signal extends well beyond the current contracted backlog.

The risk is straightforward: DRAM spot prices up 5.5x over the prior six months threaten CSG and traditional server margins if Dell’s pricing discipline lags cost inflation in the back half of FY27, compressing the EPS growth the TIKR model assumes.

Therefore, Q1 FY27 earnings will be the confirmation event: watch whether the $13 billion AI shipment target lands on schedule and whether CSG operating margin recovers sequentially from Q4’s 4.7%, the two numbers the TIKR model’s 6.2% net income margin assumption depends on most directly.

Should You Invest in Dell Technologies Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DELLl stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Dell Technologies Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DELL stock on TIKR for Free →