Key Stats for Amgen Stock

- Past-Week Performance: -0.9%

- 52-Week Range: $261.4 to $391.3

- Current Price: $366.2

What Happened?

Amgen (AMGN), the Thousand Oaks-based biotechnology company behind drugs spanning cardiovascular disease, cancer, and rare autoimmune conditions, delivered a Q4 2025 revenue beat of roughly $400M over the Wall Street consensus, even as the stock sits 6.4% below its 52-week high of $391.29.

Amgen reported Q4 total revenue of $9.87B against the IBES estimate of $9.47B and adjusted EPS of $5.29 against the $4.73 estimate on February 3, , while issuing full-year 2026 revenue guidance of $37.0B to $38.4B that already bakes in known headwinds from biosimilar competition against its bone-density drug Prolia.

Repatha, Amgen’s cholesterol-lowering injection, surpassed $3B in 2025 after a landmark Phase III trial showed a 25% reduction in first major cardiovascular events, while UPLIZNA, its twice-yearly antibody for rare autoimmune conditions, grew 73% to $655M across three approved indications.

Additionally, Chief Executive Robert Bradway stated on the Q4 2025 earnings call that “Repatha, olpasiran and MariTide together would represent a very compelling set of cardiometabolic medicines to expand our leadership in the treatment of serious chronic diseases well into the next decade,” tying together the company’s approved blockbuster with two pipeline assets targeting cardiovascular risk and obesity.

With six Phase III studies running for MariTide, its monthly-dosing obesity and diabetes drug, $3B in 2025 biosimilar sales growing at 37%, and a 2026 capital expenditure plan of $2.6B partly dedicated to MariTide manufacturing readiness, Amgen is building toward a commercial identity that extends well beyond its current portfolio into the highest-volume drug category on earth.

Wall Street’s Take on AMGN Stock

The Q4 revenue beat of roughly $400M over consensus matters not because of its size but because Amgen delivered it while absorbing a record $7.2B non-GAAP R&D spend, signaling the portfolio’s commercial durability under maximum investment pressure.

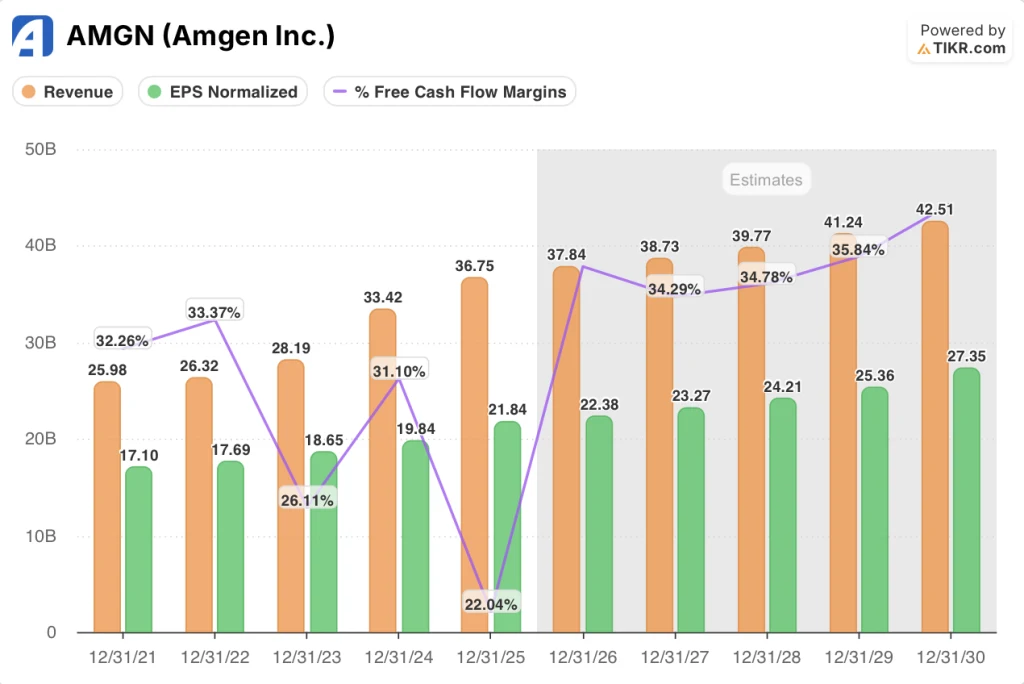

Consensus now models 2026 revenue at $37.84B, growing 3.0% from $36.75B in 2025, supported specifically by Repatha’s primary prevention expansion, UPLIZNA’s generalized myasthenia gravis launch, and the continued 37% growth trajectory in biosimilars.

Meanwhile, normalized EPS is forecast to reach $22.38 in 2026 and $23.27 in 2027, modest growth on its own, but paired with an expected free cash flow surge from $8.1B in 2025 to $13.41B in 2026, a 65.6% jump that reflects the end of one-time business development R&D charges absorbed in Q3 and Q4 2025.

That free cash flow recovery, which pushes FCF margin from 22.0% to an estimated 35.4% in a single year, is the number the market appears to be underweighting, treating a documented one-time drag as a structural margin problem.

The Street’s 29 analysts covering AMGN currently include 9 buys, 4 outperforms, 18 holds, 1 underperform, and 2 sells, with a mean price target of $350.03 implying 4.4% downside from $366.21, a lukewarm consensus that reflects caution around Prolia erosion and MariTide timeline uncertainty rather than fundamental deterioration.

The spread between the $200.00 low target and the $432.00 high target is the widest it has been in over a year, with bulls anchoring to MariTide’s six enrolled Phase III studies and bears anchoring to the TAVNEOS voluntary withdrawal and decelerating Prolia, which generated $4.4B in 2025 but faces accelerating biosimilar competition in 2026.

What Does the Valuation Model Say?

AMGN Stock Valuation Model Results (TIKR)

TIKR’s mid-case model prices AMGN at $462.66 by December 2030, implying a 26.3% total return over 4.8 years at a 5.0% annualized IRR, driven by a mid-case revenue CAGR of 3.0% and net income margin expansion from 32.1% to 34.6%.

The market is pricing Amgen as a low-single-digit grower, but the FCF margin is forecast to recover 13.4 percentage points in one year, from 22.0% to 35.4%, a reset the income statement alone does not show.

The operational evidence supporting that recovery is the $300M in one-time business development R&D charges absorbed in 2025, explicitly flagged by CFO Peter Griffith on the Q4 earnings call as non-recurring, which distorted 2025 FCF and inflated the year-over-year R&D growth rate to 22%.

Management’s signal that this is a misunderstood setup: the $2.6B 2026 capex plan, partly dedicated to MariTide manufacturing readiness, confirms Amgen is spending as if launch is coming, not as if the program is at risk.

The risk that breaks the TIKR model’s FCF recovery assumption is a MariTide Phase III failure or significant delay, which would strand $2.6B in manufacturing investment and remove the growth layer the model needs beyond 2027.

The specific number to watch is Q1 2026 revenue, where management guided low mid-single-digit YoY growth: a miss below that range, on top of the $250M Q4 inventory build, would signal commercial deceleration that the model’s 3.0% revenue CAGR cannot absorb.

Should You Invest in Amgen Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AMGN stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Amgen Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AMGN stock on TIKR for Free →