Key Stats for Carrier Stock

- Past-Week Performance: -4.6%

- 52-Week Range: $50.2 to $81.1

- Current Price: $55.7

What Happened?

Carrier (CARR) has quietly built a data center cooling business worth $1 billion in annual revenue, growing 50% in 2026, even as the stock sits 31% below its 52-week high of $81.09 on fears about the weakest residential HVAC market in nearly a decade.

Carrier’s Q4 2025 earnings on February 5 delivered adjusted EPS of $0.34, missing the $0.37 estimate, with adjusted operating income of $455 million falling 15% short of the $532.6 million consensus, as residential Americas sales collapsed nearly 40% in the quarter on distributor destocking and a housing market freeze.

The data center business, which supplies precision chillers and liquid cooling systems to hyperscale computing facilities, generated Q4 commercial HVAC orders up 4x year-over-year in the Americas, with applied orders more than tripling, positioning the company for $1.5 billion in data center revenue in 2026.

CEO David Gitlin stated on the Q4 2025 earnings call that “our data center investments are delivering results with fourth quarter CSA data center orders up more than 4x,” tying directly to the company’s expanded chiller portfolio that has grown water-cooled market share from roughly 10% to 40% since Carrier’s spin-off.

With $1.5 billion in planned share repurchases in 2026, a new 10-billion-rupee manufacturing facility signed in Andhra Pradesh on February 17, and 3-megawatt and 5-megawatt liquid cooling CDU units launching later this year, Carrier is building the supply and capacity infrastructure to convert a record data center backlog into durable margin recovery by 2027.

Wall Street’s Take on CARR Stock

The Q4 2025 earnings miss, driven entirely by a 40% collapse in residential Americas volumes, obscures that Carrier’s data center cooling business, which supplies precision chillers to hyperscale computing facilities, doubled to $1 billion in revenue last year and is guiding to $1.5 billion in 2026.

Revenue growth of 1.1% in FY 2026E is deliberately understated: consensus projects an acceleration to 5.2% in FY 2027E and 5.7% in FY 2028E, anchored by data center delivery conversions in H2 2026 and the absence of the destocking headwind that cut residential Americas sales in half.

Carrier’s EBIT margin troughed at 15.1% in FY 2025 and is projected to expand to 16.4% in FY 2027E and 17.3% in FY 2028E, supported by $100 million in overhead savings from the 3,000-person workforce reduction executed in H2 2025.

Meanwhile, CARR’s normalized EPS tells the compounding story directly: $2.59 in FY 2025 grows to $2.79 in FY 2026E, $3.18 in FY 2027E, and $3.66 in FY 2028E, a 41% cumulative increase over three years driven by margin expansion, share buybacks, and data center revenue acceleration.

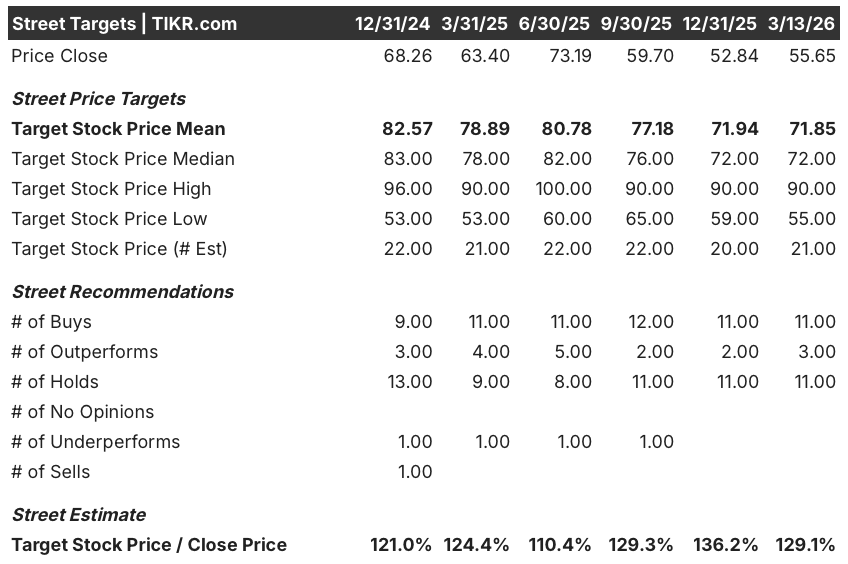

Fourteen analysts hold, but 11 buys and 3 outperforms among 25 covering analysts reflect a Street that sees the residential trough as temporary, with a mean price target of $71.85 implying 29.1% upside from the current price of $55.65.

The $35 spread between the analyst low target of $55.00 and the high of $90.00 maps directly to the residential recovery debate: the bear case prices in a housing market that stays frozen through 2027, while the bull case prices in the data center backlog converting and residential destocking ending in H2 2026 as management guided.

What Does the Valuation Model Say?

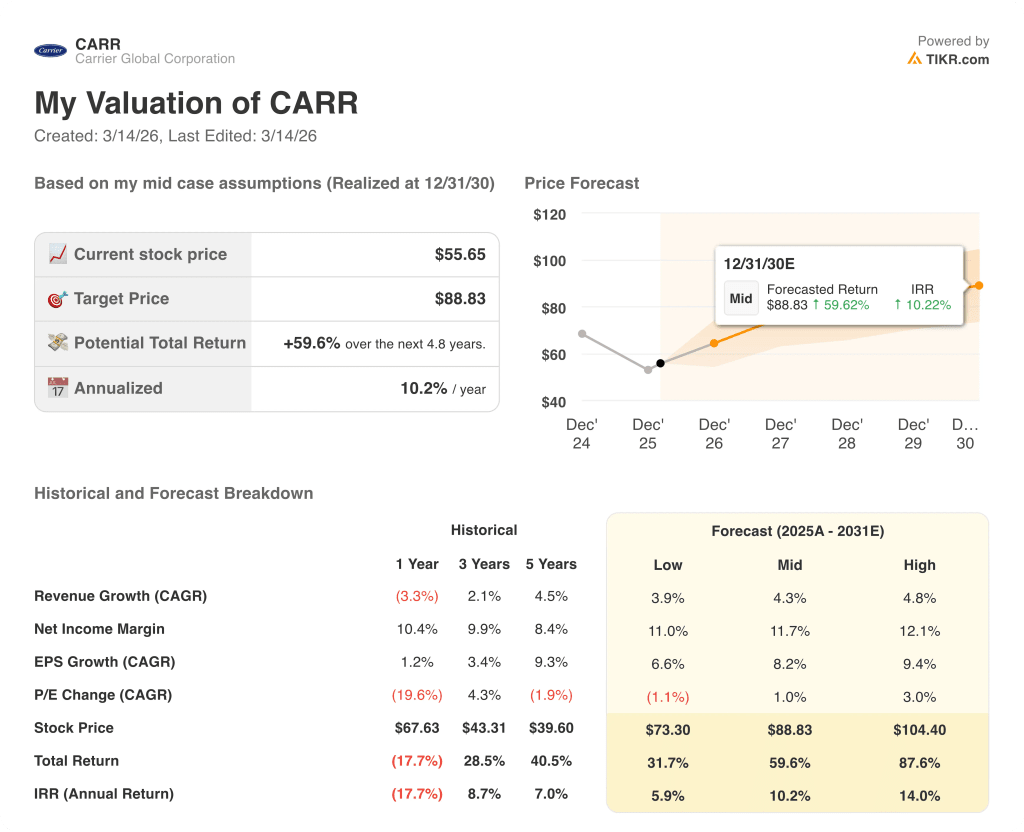

TIKR’s model targets $88.83 by December 2030, implying a 59.6% total return at a 10.2% annual IRR, built on a mid-case net income margin expanding from 10.3% in FY 2025 to 11.7% by the end of the forecast period.

The model’s 4.3% revenue CAGR assumption is conservative relative to the data center opportunity: $1.5 billion in 2026 data center revenue alone represents 6.8% of total company sales, growing at 50% annually.

The market is pricing Carrier as a residential HVAC stock in a down cycle, but data center cooling orders in Q4 2025 rose 4x year-over-year in the Americas.

CEO David Gitlin confirmed on February 19 at Barclays that guidance is “100% nothing new,” meaning Q1 is tracking exactly as modeled and the $1.5 billion data center target is intact.

If the U.S. residential HVAC market does not recover toward the 9-million-unit annual mean and data center order conversion slips into 2027, the FY 2027E EBIT margin expansion to 16.4% stalls and the model’s core assumption breaks.

Watch Q1 2026 earnings for CSA commercial HVAC margin and whether data center revenue is tracking toward the $1.5 billion full-year target, the single number that validates the margin expansion thesis.

Should You Invest in Carrier Global Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CARR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Carrier Global Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CARR stock on TIKR for Free →