Key Stats for Amazon Stock

- Past-Week Performance: -2.6%

- 52-Week Range: $161.4 to $258.6

- Current Price: $207.7

What Happened?

Amazon (AMZN), the e-commerce and cloud computing giant, reported AWS growth accelerating to 24% on a $142 billion annualized run rate, the fastest pace in 13 quarters, while the stock sits at $207.67, nearly 20% below its 52-week high of $258.60.

The Q4 earnings call confirmed $213.4 billion in total revenue, $25 billion in operating income, and a $244 billion AWS backlog, up 40% year-over-year, as the company committed approximately $200 billion in 2026 capital expenditures predominantly in AWS infrastructure.

Trainium, Amazon’s custom AI chip that now underpins the majority of its Bedrock inference workloads, landed 1.4 million Trainium2 chips in its fastest-ever ramp, while Trainium3, which delivers 40% better price-performance than Trainium2, is expected to be nearly fully committed by mid-2026.

Moreover, CEO Andy Jassy stated on the Q4 2025 earnings call that “as fast as we install this AI capacity, we are monetizing it,” connecting directly to the March 13 AWS-Cerebras partnership that pairs Trainium with Cerebras CS-3 chips to deliver faster AI inference on Amazon Bedrock.

Amazon launched a Health AI agent on March 10 and rolled out Prime Video Ultra at $4.99 per month on March 13, while Amazon Leo’s commercial satellite internet service targets a 2026 launch and Trainium4 arrives in 2027, compounding addressable markets across healthcare, media, cloud, and connectivity simultaneously.

Wall Street’s Take on AMZN Stock

The $244 billion AWS backlog, up 40% year-over-year, directly supports the 2026 revenue estimate of $806.96 billion, a 12.6% increase, as enterprises convert signed commitments into active cloud workloads throughout the year.

EBITDA is projected to grow 24% to $210.6 billion in 2026 and another 22.5% to $258 billion in 2027, with margins expanding from 23.7% in 2025 to 28.7% in 2027 as Trainium-driven cost efficiencies compound across AWS infrastructure.

AMZN’s EPS normalized reaches $7.72 in 2026, a 7.7% step from $7.17, then accelerates to $9.34 in 2027 and $11.69 in 2028, a trajectory anchored by AWS operating leverage and advertising revenue that grew 22% to $21.3 billion in Q4 alone.

Accordingly, Forty-eight analysts rate AMZN a buy and 15 call it an outperform, with a mean price target of $280.55 implying 35.1% upside from $207.67, a near-unanimous consensus built around AWS acceleration and the Trainium chip cycle capturing AI inference share from Nvidia.

Also. the spread between the $175 low target and the $360 high reflects the real debate: bears anchor on the $200 billion capex cycle depressing near-term free cash flow; bulls price in the $244 billion backlog converting to revenue as Trainium3 reaches full deployment by mid-2026.

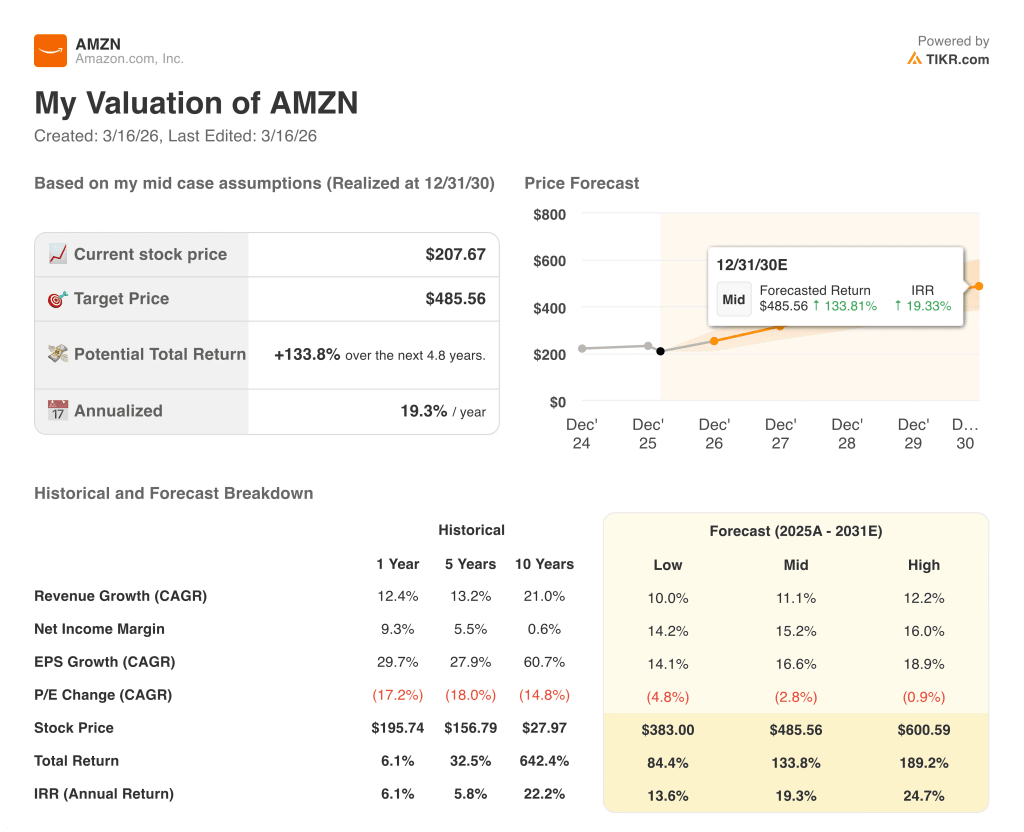

What Does the Valuation Model Say?

TIKR’s mid-case model prices AMZN at $485.56, a 133.8% total return over 4.8 years at a 19.3% annualized IRR, assuming 11.1% revenue CAGR and net income margins expanding from 10.8% in 2025 to 15.2%. The Trainium-underpinned Bedrock platform and the $244 billion backlog are the two operational inputs justifying both assumptions.

The market is pricing in capex risk while AWS operating margin already sits at 35% and the backlog hit $244 billion, up 40%.

Trainium3 reaching near-full commitment by mid-2026 and the AWS-Cerebras partnership going live in the second half of 2026 justify TIKR’s $485.56 target by expanding inference capacity without proportional cost increases.

Amazon monetizes capacity as fast as it installs it, per Jassy on the Q4 call, and the $244 billion backlog makes that claim contractually verifiable.

Meanwhile, free cash flow turns sharply negative in 2026 at an estimated -$18.78 billion as the $200 billion capex cycle peaks; if AWS revenue growth decelerates below 20%, the 2027 FCF recovery of $50.97 billion breaks entirely.

Watch the Q1 2026 earnings call for the AWS growth rate: if it holds at or above 24% as Trainium3 supply comes online, the TIKR mid-case margin expansion trajectory stays intact.

Should You Invest in Amazon.com, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AMZN stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Amazon.com, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AMZN stock on TIKR for Free →