Key Stats for OKTA Stock

- Today’s Performance: 30%

- 52-Week Range: $63 to $125

- Valuation Model Target Price: around $140

- Implied Upside: about 14%

Analyze your favorite stocks like Okta with TIKR (It’s free) >>>

What Happened?

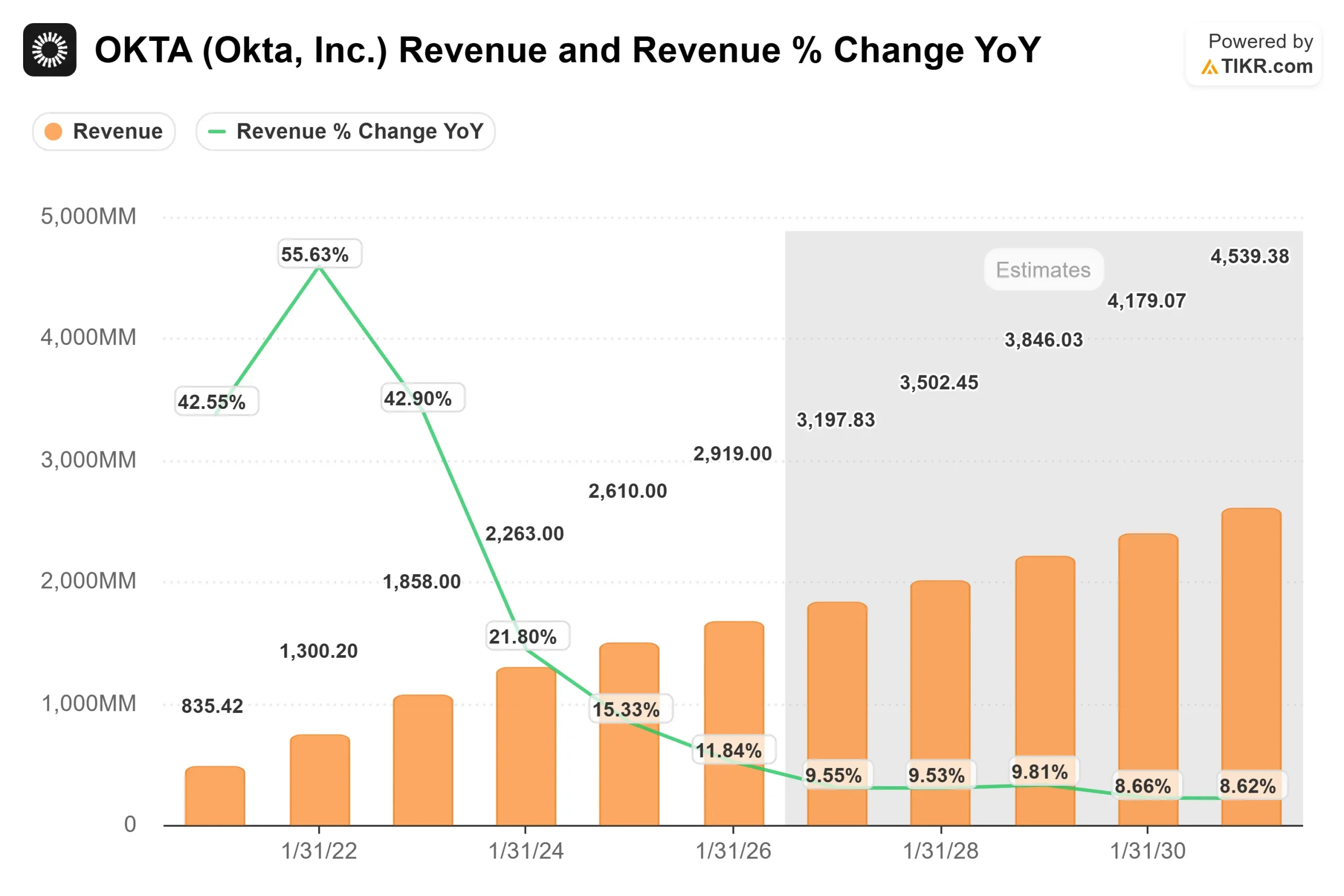

Okta Inc. stock rose about 30% today, recently trading near $123 per share, as investors rushed back into one of the more debated identity-security names in software. The move followed a stronger-than-expected Q1 fiscal 2027 report, raised full-year guidance, and a broad wave of analyst price target increases, pushing shares close to the top of their 52-week range after Okta reported adjusted EPS of $0.91 on revenue of $765 million, with sales up 11% year over year.

The stock moved higher because Okta gave investors several clear reasons to reprice the business at once: earnings beat expectations, FY 2027 guidance improved, AI-agent identity demand strengthened, and more than 20 Wall Street firms raised their price targets after the report. The rally also showed that investors are starting to look at Okta as more than a login and access-management company. The bigger question now is whether Okta can become a broader identity-security platform for employees, customers, and AI agents while competing with Microsoft Entra, CyberArk, SailPoint, Ping Identity, and ForgeRock.

Okta’s Q1 fiscal 2027 earnings call gave the rally more support. Management pointed to large enterprises, partner engagement, and newer products as key drivers, while new products reached about 25% of Q1 bookings and delivered a 40% ACV uplift when included in deals. CEO Todd McKinnon said, “Every agent inside an enterprise is a new identity,” framing AI agents as a major new security challenge because companies need to control what AI agents can access, what data they can touch, and when they should be shut down. CFO Brett Tighe also guided for Q2 revenue growth of 9%, current RPO growth of 11%, non-GAAP operating margin of 26%, and full-year FY 2027 revenue growth of 9% to 10%, with full-year free cash flow margin expected at 27% to 28%.

Analyst actions reinforced the move. Barclays raised its price target to $120 from $93, Canaccord lifted its target to $115 from $95, Citigroup raised its target to $105 from $87, Piper Sandler lifted its target to $105 from $82, Morgan Stanley raised its target to $115 from $101, Wells Fargo increased its target to $100 from $85, Susquehanna lifted its target to $110 from $80, Berenberg raised its target to $135 from $120, Truist lifted its target to $120 from $100, and Royal Bank of Canada raised its target to $122 from $108. Those updates helped validate the post-earnings rally, but many targets still sat near or below Okta’s current share price, suggesting Wall Street became more confident in Okta’s 2026 execution while also recognizing that the 30% move already priced in a lot of the good news.

Value Okta instantly (Free with TIKR) >>>

Is Okta Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): around 10%

- Operating Margins: around 27%

- Exit P/E Multiple: 28x

Okta’s revenue growth is no longer exploding like an early-stage software company, but the setup looks healthier because subscription revenue is still growing, cRPO is rising, and net retention has improved to 107%.

The around 10% revenue growth assumption depends on Okta turning large-enterprise demand, Identity Governance, and AI-agent security into stronger bookings. Identity Governance helps companies decide who can access which systems, while AI-agent security gives businesses a way to control software agents that can act on behalf of employees or customers.

See analysts’ growth forecasts and price targets for Okta (It’s free) >>>

The around 27% margin assumption depends on Okta growing subscription revenue while keeping sales execution disciplined. That matters because identity software can become highly profitable when customers expand over time, especially if Okta’s partner channel handles more services work and the company avoids heavy discounting to win large deals.

Based on these inputs, the model estimates a target price of around $140, implying about 14% total upside, which means Okta appears modestly undervalued after today’s sharp rally.

At current levels, Okta’s next move likely depends on execution, with future upside driven by stronger enterprise expansion, AI-agent security adoption, and continued operating leverage rather than another quick valuation reset.

How Much Upside Does Okta Stock Have From Here?

Investors can estimate Okta’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.