Key Stats for NVIDIA Stock

- Current Price: $210.69

- Target Price (Mid): ~$550

- Street Target: ~$300

- Potential Total Return: ~160%

- Annualized IRR: ~23% / year

- Earnings Reaction: -1.77% (May 20, 2026)

- Max Drawdown: 20.22% (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

A Company That Didn’t Need the Money Just Borrowed $25 Billion

NVIDIA (NVDA) generates more free cash flow than almost any company on earth, so the obvious question this week was simple: why borrow at all? The answer is the most revealing thing about the stock right now. On June 15, NVIDIA priced its largest bond offering ever at $25 billion, its first debt sale since 2021, and the deal closed on June 18. Shares ended that day at $210.69, up 2.95%, near a record high.

The size is not the story. The demand is. The offering drew roughly $85 billion in orders, more than three times the deal, letting NVIDIA upsize from $20 billion and cut its borrowing cost. The notes run across seven tranches out to 2056. A 30-year bond is a bet that AI infrastructure is a decades-long buildout, not a passing cycle.

This is not a funding rescue. NVIDIA holds more cash than debt, with net debt of negative $40 billion even after the raise. It is locking in cheap, long-dated capital to fund growth and shareholder returns at once, without diluting a share. That is the bull case in one transaction. The bear case is the mirror: if AI demand cools, 30-year debt raised at the top of a capex boom ages badly.

The Timing Lines Up With What Management Has Been Saying

Two weeks earlier, at the Bank of America Global Technology Conference, CFO Colette Kress explained why NVIDIA needs a bigger financial toolkit. She sized the forward supply obligations directly. “We’re essentially at about $124 billion of commitments,” said Colette Kress, Executive Vice President and CFO. Those cash demands are locked in years ahead, which is exactly what long-dated debt is built to fund.

Kress also confirmed the roadmap behind the demand. Vera Rubin, NVIDIA’s next data center platform, is “ready for Q3” and in full production, and she framed Blackwell and Rubin together as roughly $1 trillion in opportunity across 2025 through 2027.

Debt also frees cash for a fast-rising capital return. NVIDIA authorized an $80 billion buyback on May 18 and lifted its dividend sharply. Kress was blunt about the priority: “The amount that we can return to shareholders 50% or more absolutely is a key focus of ours,” confirming the new dividend at “$1 a share per year.” Asked why not 75%, she said only, “We’re working on it.”

See historical and forward estimates for NVIDIA stock (It’s free!) >>>

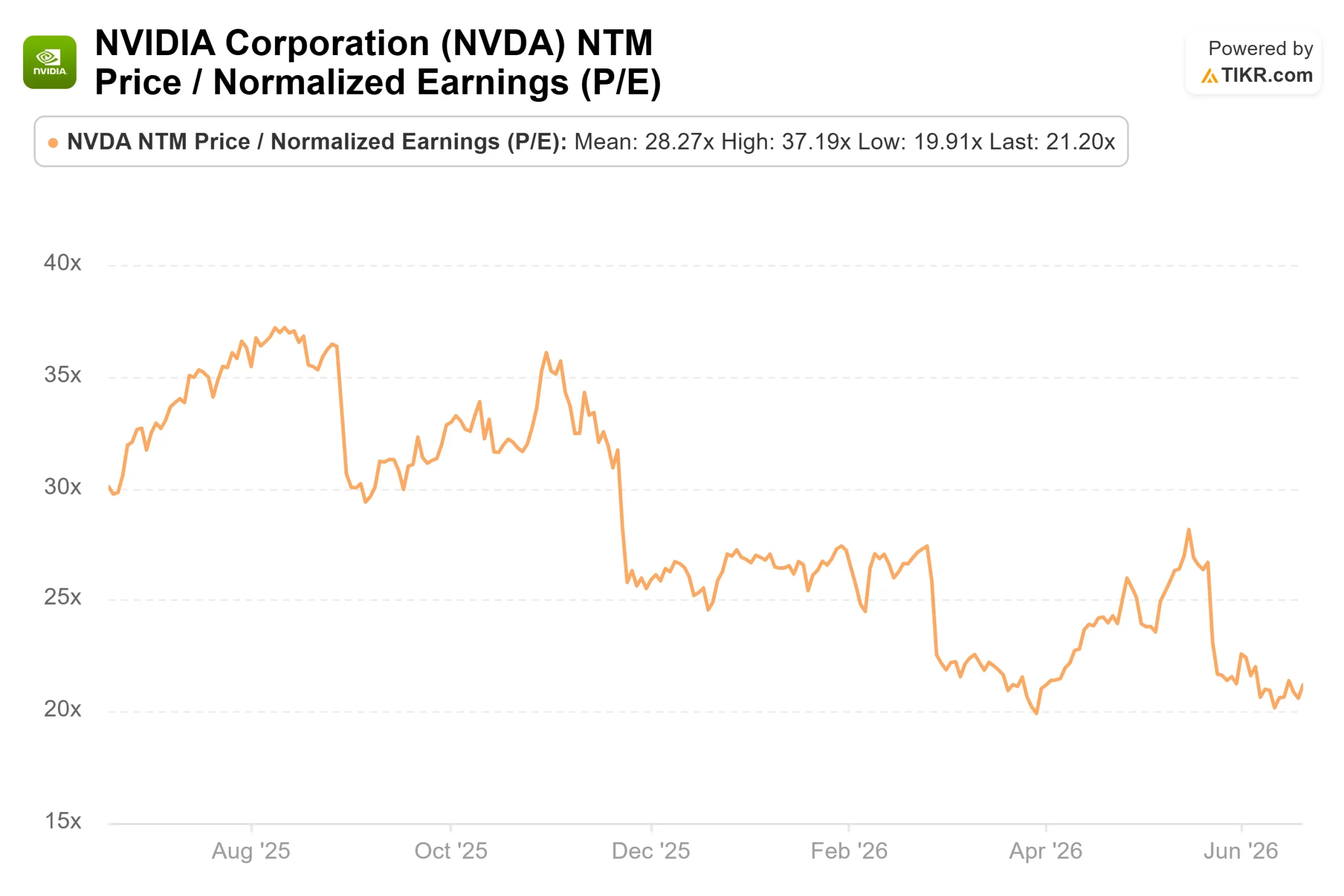

The Discount That Keeps Following NVIDIA Around

Here is the tension. NVIDIA is the world’s most valuable company at $5.1 trillion, yet it trades cheaper than its peers on the metric that matters most for a fast grower. Its next-twelve-months P/E is 21.20x. Among semiconductor peers on the TIKR Competitors page, Broadcom trades at 26.13x and AMD at 61.63x. The fastest grower in the group is one of the cheapest.

That gap is not random. Export controls remain unresolved, and NVIDIA’s guidance assumes zero Data Center compute revenue from China. Hyperscaler custom chips threaten the GPU. And after the May 20 earnings report, shares slipped 1.77% even as revenue rose 85% year over year to $81.6 billion. NVIDIA has a habit of posting great numbers and selling off anyway, because expectations outrun even strong results.

The fundamentals keep widening the gap between price and performance. That same quarter produced $48.6 billion in free cash flow, the base that makes $25 billion in new debt look conservative.

See how NVIDIA performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $210.69

- Target Price (Mid): ~$550

- Potential Total Return: ~160%

- Annualized IRR: ~23% / year

See analysts’ growth forecasts and price targets for NVIDIA stock (It’s free!) >>>

The model entry price matches the live close, and the target lands by early 2031. Two revenue drivers carry the case: the Blackwell and Vera Rubin ramp, and diversification into AI clouds, enterprises, and sovereigns beyond core hyperscalers. The margin driver is NVIDIA’s full-stack pricing power, with net income margins modeled around 55%. The primary risk is multiple compression, since the model already assumes a modest yearly P/E decline, and any sharper de-rating breaks the math.

The upside: if mid-case revenue growth of over 20% holds, NVIDIA roughly doubles from here. The downside: a demand air pocket or a China shock turns those long bonds into a cautionary tale, and the multiple keeps shrinking.

Conclusion

The next test is the Q2 FY2027 report due in late August. Watch Data Center revenue and the China outlook: a clean beat confirms the buildout is still accelerating, and the $25 billion was money well borrowed. A guide-down, or a China-driven shortfall, validates the bears and the discount holds. The bond market just signaled what long-term money believes. By September, NVIDIA’s income statement will say whether it was right.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in NVIDIA?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NVIDIA, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NVIDIA alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!