Key Stats for Micron Stock

- Current Price: $1,213.56

- Target Price (Mid): ~$1,180

- Street Target: ~$1,230

- Potential Total Return: ~(3)%

- Annualized IRR: ~(1)% / year

- Earnings Reaction: +15.74% (June 24, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Micron Technology (MU) just did something memory companies almost never do: it made AI demand look predictable. On June 24, the chipmaker reported the most profitable quarter in its 48-year history, then told investors it had signed contracts that customers are not allowed to cancel. The stock jumped 15.74% the next session. For a business, the market spent decades pricing as a commodity, cyclical; that reaction was the point.

The tension now is sharp. Bulls see a company that has escaped the memory cycle, with multiyear deals that lock in pricing and a shortage management says runs past 2027. Bears see a stock up more than 800% in a year that now trades above where almost every model, including Wall Street’s own average target, says it should. The question the market cannot yet answer: if this quarter is the new normal, what is it worth?

A Record That Beat Even the Raised Bar

Micron entered earnings with expectations already stretched. At least six banks had doubled their price targets in a single June week, and the stock had run past most of them. Then the company beat anyway.

Revenue came in at $41.46 billion, up from $9.30 billion a year earlier and well above the roughly $35.8 billion analysts modeled. Non-GAAP earnings of $25.11 per share topped the consensus of nearly $20. Gross margin reached a record 84.9%, up from 39% a year ago. The core data center business was the engine, with revenue there climbing more than sevenfold to $11.5 billion.

Guidance went further than the quarter. Management projected fiscal Q4 revenue of around $50 billion, plus or minus $1 billion, with gross margin near 86% and earnings of around $31 per share. That outlook sits sharply above the roughly $43.6 billion the Street had penciled in. This was not a small upside surprise. It was a re-rating of what Micron earns.

See historical and forward estimates for Micron stock (It’s free!) >>>

The Contracts Are the Real Story

The number that changed the debate was not revenue. It was $22 billion: the total cash and financial commitments tied to 16 Strategic Customer Agreements (SCAs), which are long-term supply deals with data center operators, automakers, and other buyers. Almost $18 billion of that is upfront cash deposits already in hand.

Chief Business Officer Sumit Sadana was blunt about how binding these are. “These Strategic Customer Agreements or SCAs cannot be canceled,” he told analysts, describing take-or-pay deals that obligate customers to pay price times volume “whether they want to purchase the bits or not.” That attacks the exact fear that has capped Micron’s multiple for years: that demand evaporates, and pricing collapses. A take-or-pay book does not remove cyclicality, but it puts a contractual floor under revenue that commodity memory never had.

Sadana also laid out the ambition. The deals cover roughly 20% of DRAM bits and a third of NAND bits today, and management intends to grow that “all the way to roughly accounting for half of the company’s revenue.” CFO Mark Murphy put the appeal plainly: “We get visibility on our demand, it’s committed volume that we can be confident about making our investments.”

Supply Stays Short, and That Is the Point

These deals carry weight because supply cannot catch up. Micron expects market tightness beyond 2027, and Murphy said the high-bandwidth memory (HBM) market, the premium DRAM that sits beside AI processors, will cross $100 billion in 2027, a year earlier than the company’s prior view. The constraint is physical: HBM uses far more silicon per bit than standard DRAM, and new greenfield fabs do not produce meaningful output until calendar 2028.

That is also the bear case. Micron is raising fiscal 2026 capital spending to around $27 billion and signaled fiscal 2027 will run above the mid-$40 billion range. The spending funds the shortage’s profits, but it lands before anyone can confirm demand holds.

On valuation, Micron looks cheap against its memory peer. Per TIKR’s Competitors data, it trades at a next-twelve-months EV/EBITDA of 6.45x, against a semiconductor peer mean near 22.6x. Closest rival SK Hynix sits at 5.40x, so Micron holds a slight premium to Hynix and a steep discount to the broader group. That gap reflects the market’s long refusal to pay up for memory cyclicality. Whether the SCAs justify closing it is an open question.

See how Micron performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

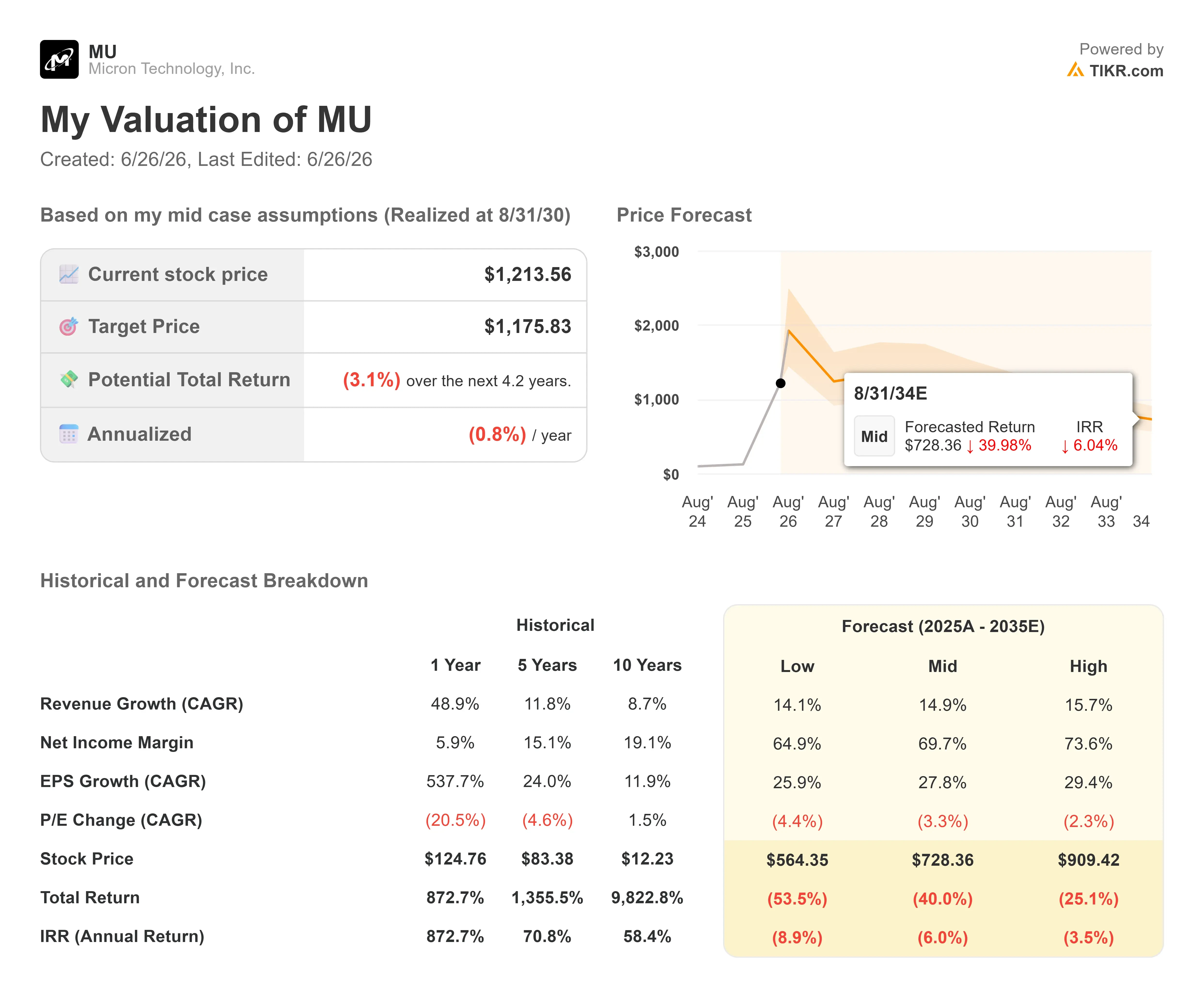

- Current Price: $1,213.56

- Target Price (Mid): ~$1,180

- Potential Total Return: ~(3)%

- Annualized IRR: ~(1)% / year

See analysts’ growth forecasts and price targets for Micron stock (It’s free!) >>>

Here is where the euphoria meets the math. On TIKR’s mid-case assumptions, the model lands on a target of around $1,180, just below the current $1,213.56. That implies a total return near negative 3% and an annualized return of around negative 1% over the next 4.2 years. After one of the great runs in large-cap tech history, the base case says the stock is roughly fairly valued to modestly expensive.

The Street agrees: its mean target sits around $1,230, barely above the price, even after post-earnings hikes. Of 45 analysts, 29 rate MU Buy, 9 Outperform, 5 Hold, 1 Underperform, and 1 Sell.

The mid case is not timid. It assumes revenue growth of around 15% per year, a net income margin near 70%, and EPS growth of about 28% annually. The two revenue drivers are HBM volume scaling into the $100 billion-plus 2027 market and the SCA book converting committed bits into recurring sales. The margin driver is sustained DRAM and HBM pricing from structural undersupply. The main risk is the fiscal 2027 capex step-up colliding with a demand air pocket as greenfield supply arrives in 2028.

The upside in one line: if Micron holds these margins through the next trough, the cycle has truly broken, and the model is too harsh.

The downside in one line: if pricing normalizes as capacity lands, earnings and the multiple compress together, the pattern memory investors know well.

Conclusion

The whole debate hinges on one thing the SCAs cannot yet prove: durability through a downturn. Watch the fiscal Q4 print, due in late September 2026, against the $50 billion revenue and roughly 86% gross margin guidance. Hit both, and the case that Micron has structurally re-rated gets much stronger, a fourth straight record built on pricing the company calls contractually locked. Come in below $48 billion in revenue or under 84% gross margin, and the market will start asking whether peak earnings arrived this quarter. The deeper test comes later, when the first SCA pricing bands reset, and investors see what the floor under “uncancelable” looks like in a softer market. Until then, the stock is priced for the bull case to keep being right.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Micron?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Micron, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Micron alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!