Key Stats for Martin Marietta Materials Stock

- Past-6-Month Performance: 14%

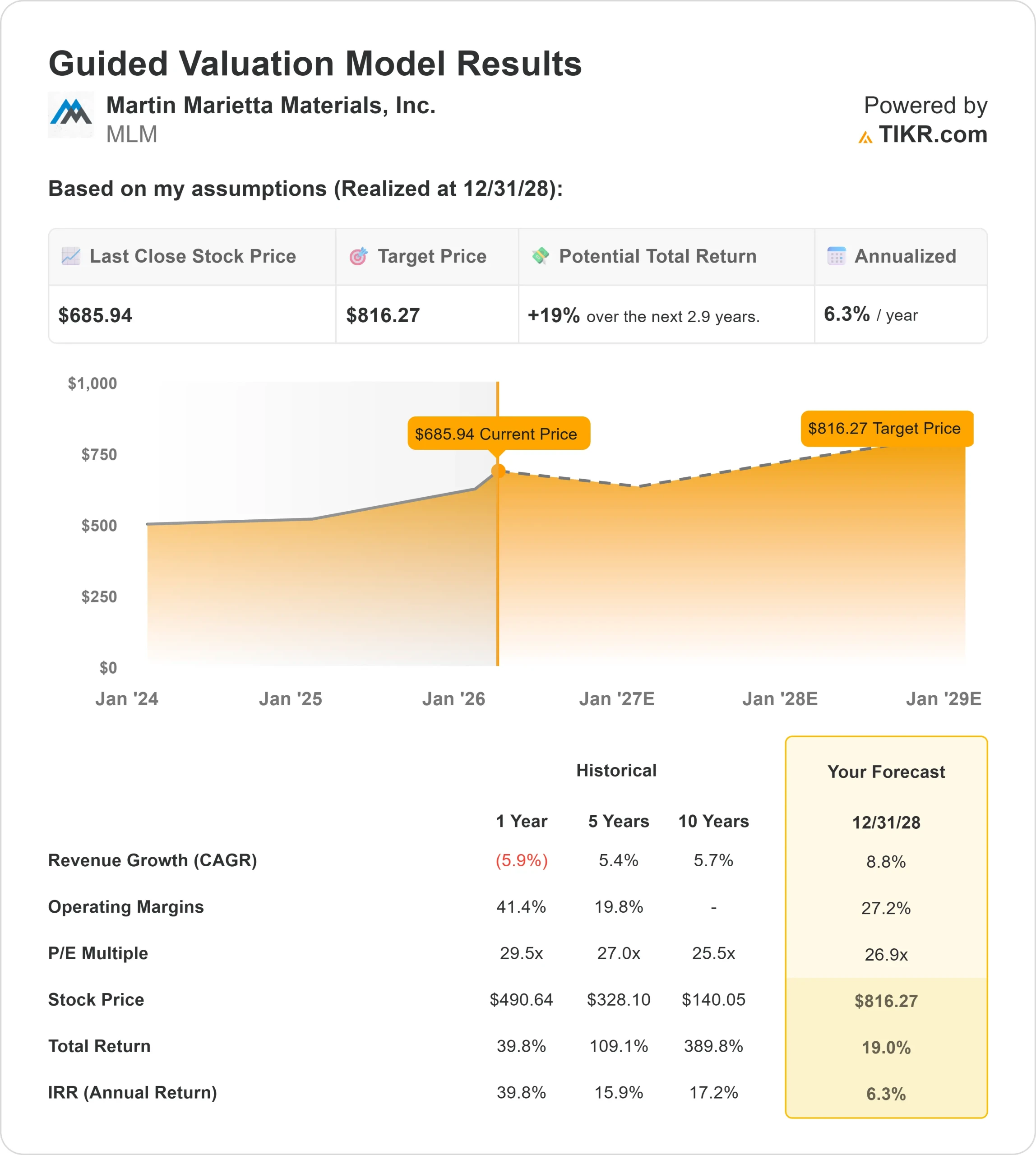

- 52-Week Range: $442 to $711

- Valuation Model Target Price: $816

- Implied Upside: 19%

Value your favorite stocks like Martin Marietta Materials with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Martin Marietta Materials stock has climbed about 14% over the last six months, recently trading near $686 per share as investors repositioned around improving infrastructure visibility, disciplined pricing, and strong cash generation.

The stock is up primarily because the company delivered record 2025 results and reaffirmed steady 2026 growth during its February 11 earnings call, reinforcing earnings durability despite a balanced macro environment.

Shares are holding near the upper end of their $442 to $711 52-week range, reflecting sustained confidence in the company’s aggregates-led business model.

While 2025 delivered record results, shipment growth guidance of about 2% at the midpoint for 2026 signals stable but not accelerating volumes, which likely explains why shares have recently consolidated after their strong run.

During the earnings call, management reported aggregates revenue rose 11% to $5 billion and aggregates gross profit increased 16% to $1.7 billion in 2025. Cash flow from operations climbed 22% to a record $1.8 billion.

CEO Ward Nye called 2025 “an outstanding year for Martin Marietta” and guided for consolidated adjusted EBITDA of approximately $2.49 billion in 2026.

Analyst activity also supported the move higher. Jefferies raised its price target to $761 and maintained a Buy rating following the results, reinforcing confidence in the company’s long-term margin expansion and infrastructure exposure.

Institutional positioning remains active. JPMorgan trimmed its stake slightly to 2,934,783 shares valued at about $1.85 billion, while Pelham Capital increased its position by 57% to 30,052 shares and now allocates 9.4% of its portfolio to Martin Marietta.

TimesSquare Capital reduced its position by 10.9% to 95,704 shares. Overall institutional ownership remains near 95%, underscoring strong long-term sponsorship.

Infrastructure remains the foundation of visibility into this year. About 37% of the business is tied to infrastructure, and top state DOT budgets are up roughly 7%.

Of IIJA highway funds, 71% have been obligated while only 48% disbursed, providing continued runway into 2026. Heavy nonresidential markets also remain supportive, with data center volumes growing around 60% and representing roughly 3% of shipments.

See analysts’ growth forecasts and price targets for Martin Marietta Materials (It’s free) >>>

Is Martin Marietta Materials Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 8.8

- Operating Margins: 27.2%

- Exit P/E Multiple: 26.9x

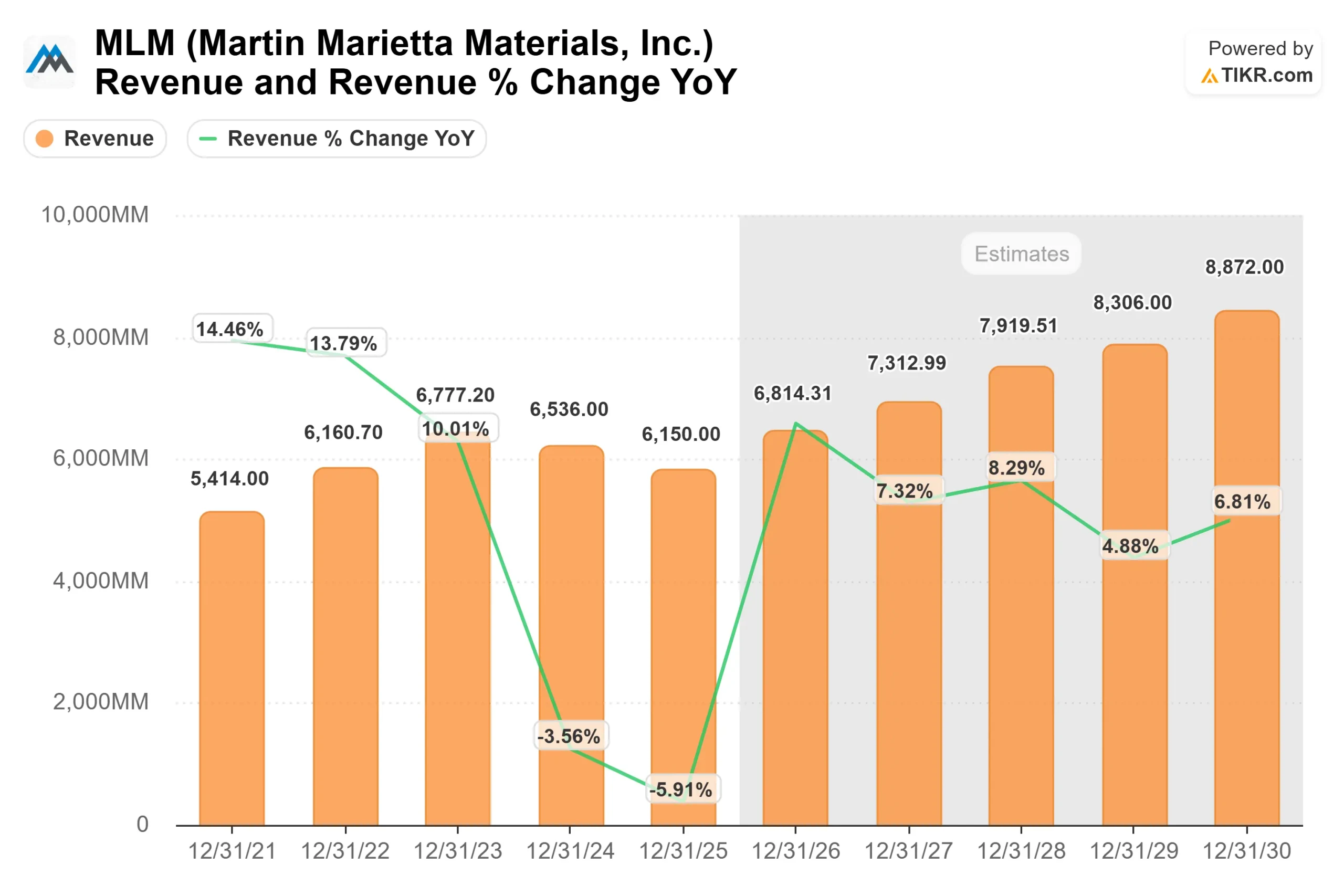

Revenue is projected to compound at nearly 9% annually through 2028, supported by federal infrastructure programs, strong state transportation budgets, and continued investment in data centers, LNG facilities, and power generation projects.

For 2026 specifically, management expects low single-digit shipment growth combined with mid-single-digit pricing increases, supporting low double-digit aggregates gross profit growth.

Pricing discipline remains a key driver, particularly in high-growth Sun Belt markets where supply remains constrained and permitting new capacity is difficult.

Data centers and energy projects remain incremental demand drivers this year. Although data centers represent only about 3% of shipments today, management noted volumes are growing at roughly 60%, which can contribute meaningful operating leverage as quarries run at higher utilization.

Operational execution also supports the margin outlook. The company is expanding network optimization efforts after successful pilot programs reduced cost per ton in late 2025.

Combined with disciplined capital allocation and portfolio reshaping toward higher-margin aggregates, this supports the 27% margin assumption used in the valuation model.

Cash flow remains a strategic advantage. With $1.8 billion in operating cash flow in 2025 and net debt to adjusted EBITDA around 2.3x, Martin Marietta retains flexibility for targeted acquisitions and shareholder returns while funding organic growth.

Based on these inputs, the valuation model estimates a target price of $816, implying about 19% total upside and 6.3% annualized returns.

At $686 per share, Martin Marietta appears modestly undervalued, with 2026 performance likely driven by infrastructure disbursements, pricing strength, cost discipline, and continued heavy nonresidential demand rather than multiple expansion alone.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>