Key Stats for Lululemon Stock

- Current Price: $111.77 (June 18, 2026 close)

- Target Price (Mid): around $143

- Street Target: around $134

- Potential Total Return: around 28%

- Annualized IRR: around 6% / year

- Earnings Reaction: -8.56% (June 4, 2026)

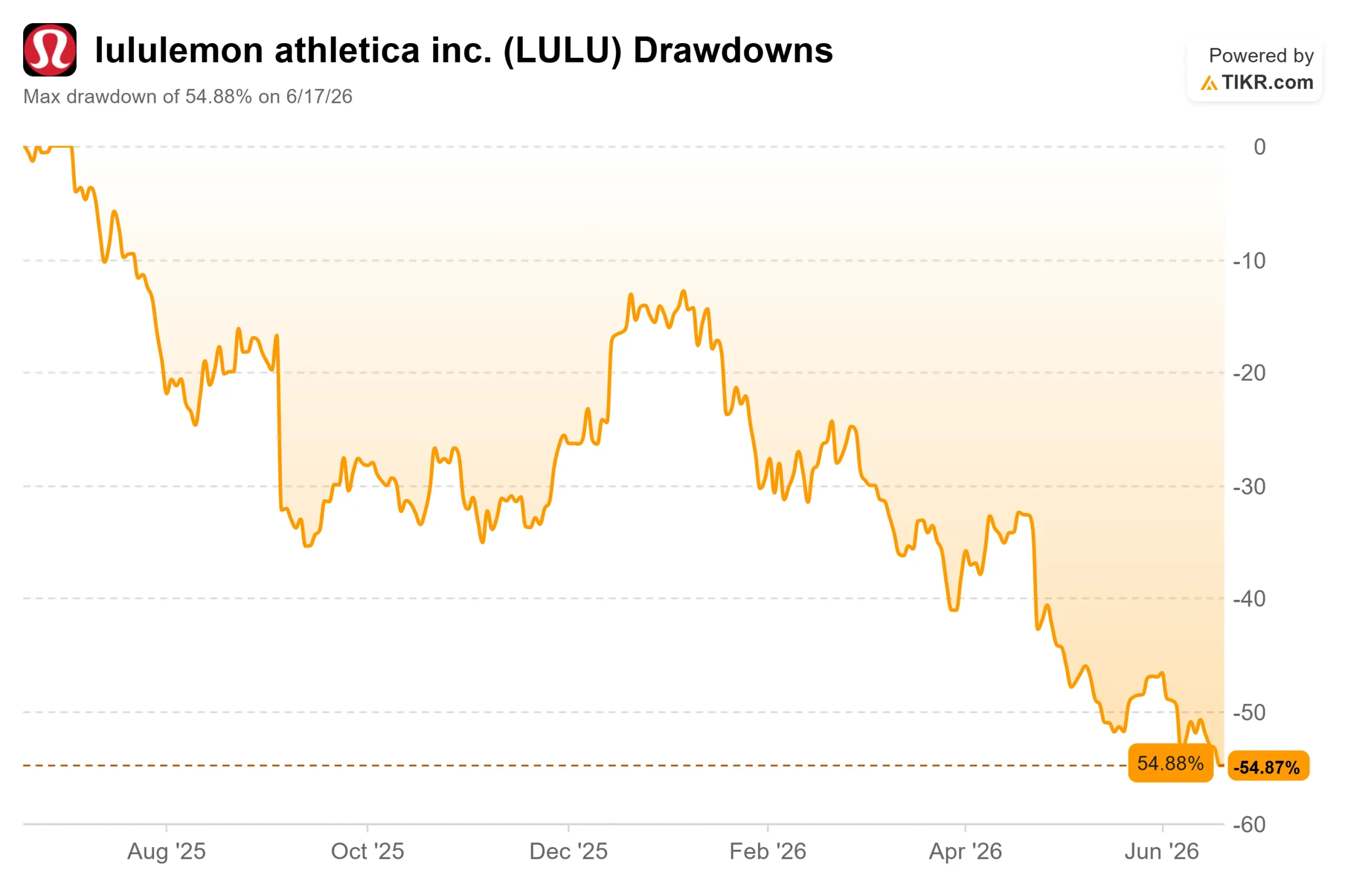

- Max Drawdown: -54.88% (June 17, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Lululemon athletica inc. (LULU) had one part of its story still working. While North America stalled, China was the growth engine, guided to grow about 20% a year. Then a yoga event on the Great Wall turned into a public apology, and the bright spot started to look fragile too.

The stock closed at $111.77 on June 18, near a 52-week low of $109.36 and down about 46% in 2026. Bulls see a single-digit earnings multiple on a brand that still prints high margins. Bears see a company guiding to flat-to-down revenue, with the recovery now resting on a market that just showed how fast sentiment can turn. The question the market cannot yet answer: if China wobbles, what carries the recovery?

The China backlash investors did not see coming

On May 30, Lululemon staged a yoga festival on the Great Wall of China, billed as a celebration of Chinese culture. The problem was a drum. A percussion instrument used in the performance was identified online as resembling a Japanese taiko drum rather than a Chinese one, and in a market where anti-Japanese sentiment runs deep, the backlash was swift. The company scrubbed its campaign and apologized on June 17, citing “limitations in our professional knowledge.”

The stock slid to fresh 52-week lows the same week. For a company whose growth narrative now leans on China, the timing could not have been worse.

What stings is that management had just told investors China was holding up. On the Q1 call on June 4, Interim Co-CEO and CFO Meghan Frank said earlier brand noise had subsided: “These stories have died down and subsided, but we have not yet seen a return to our pre-disruption trends.” In plain terms, the damage lingers in the numbers even after headlines fade.

A cheap stock for a reason

Lululemon trades at about 9x trailing earnings, still generates a 55.7% gross margin, and carries almost no net leverage, with net debt to EBITDA at 0.19x. On those facts, the stock screens as a bargain.

The discount is not a mistake, though. Americas comparable sales fell 5% in Q1, the fifth straight quarterly decline, and management guides full-year North America revenue down high single digits. The whole company is guided to revenue of $11 billion to $11.15 billion, flat to down about 1%, with full-year EPS cut to $10.95 to $11.15 from $13.26 last year. Gross margin fell 410 basis points in Q1 on tariffs and markdowns.

Frank was blunt on the causes: negative commentary plus product misses. “Not all of our product launches have met our expectations,” she said, pointing to a “new look of yoga” campaign that drew interest but failed to lift the rest of the assortment. That self-inflicted quality is the bear case. Tariffs are a recoverable, industry-wide headwind. Brand sentiment and product missteps are harder to fix on a schedule, with a permanent CEO not arriving until September.

The market agreed. The June 4 print sent shares down 8.56% the next session, and analysts slashed targets: Stifel to $134, JPMorgan to $149, Bernstein to $145, Piper Sandler to $110, and BNP Paribas downgraded to Underperform at $88, citing decelerating China sales. The consensus Street target has compressed to around $134, just above the current price.

See historical and forward estimates for Lululemon stock (It’s free!) >>>

What the Bulls still have to work with

The recovery case is not empty. China is still expected to grow about 20% for the year, and management held that line after the backlash. International overall grew 22% in Q1. The balance sheet helps: $1.5 billion in cash and roughly $1 billion left on the buyback give room to repurchase shares cheaply while funding a marketing push, now lifted to 6% to 6.5% of sales.

The peer discount is stark. Lululemon trades at 5.78x forward EV/EBITDA versus a peer mean of 10.64x, with Nike at 19.06x, Deckers at 10.04x, and adidas at 10.16x. The market prices Lululemon as a structurally challenged retailer, not a premium brand. Whether that gap is justified depends entirely on North America stabilizing and China holding. A brand growing 20% in its key international market should not trade at half its peers’ multiple, and the fact that it does tells you how much execution risk the Street assigns.

See how Lululemon performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $111.77

- Target Price (Mid): ~$143

- Potential Total Return: ~28%

- Annualized IRR: ~6% / year

See analysts’ growth forecasts and price targets for Lululemon stock (It’s free!) >>>

The entry price of $111.77 sits below most analyst targets and near the 52-week low, so the starting point already reflects a beaten-down stock.

The two revenue drivers are modest: forward growth around 3% to 4%, leaning on China and international expansion to offset North America, plus low-double-digit square footage growth as the store fleet expands abroad. The margin driver is net income margin holding near 12%, well below the 17% peak. The primary risk is North America: if comparable sales keep falling and full-price selling does not recover, the growth assumptions break.

The upside: if product newness lands and China sustains 20% growth, margin recovery pushes returns toward the high case.

The downside: if North America stays negative and China damage deepens, the low case points to roughly low-single-digit annual returns, barely paying for the risk.

Conclusion

Watch America’s comparable sales when Lululemon reports Q2 in early September, the same month new CEO Heidi O’Neill starts. Management guided the segment down into the low double digits, so “good” looks like a shallower decline with sequential improvement. “Bad” is another leg down that confirms the brand problem is structural. Watch China alongside it: any crack in the 20% growth guide after the Great Wall episode would remove the last pillar the recovery leans on. Until both stabilize, a 9x multiple is less a bargain than a measure of how much the market doubts the turnaround.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Lululemon?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Lululemon, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Lululemon alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Lululemon on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!