Key Stats for Alphabet Stock

- Current Price: $368.03

- Target Price (Mid): ~$635

- Street Target: ~$433

- Potential Total Return: ~73% (over the next ~4.5 years)

- Annualized IRR: ~13% / year

- Earnings Reaction: +9.96% (April 29, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Alphabet (GOOGL) is in a strange spot for a company this good. Analysts keep marking their price targets higher, quarter after quarter, yet the stock has drifted down from its peak. At $368.03, GOOGL sits about 9% below the $408.61 high it set in the past year, while the average Wall Street target has climbed to roughly $433.

That is the disagreement worth understanding. The Street is getting more bullish on paper as buyers step back in practice. One side prices the AI build-out as a compounding asset. The other watches the free cash flow get squeezed and asks what it is paying for. The question neither side has answered: is the recent softness a warning, or a gift?

The targets keep climbing

TIKR’s Street data shows the mean analyst target rising every quarter, from around $331 at the end of 2025 to roughly $381 in March 2026, and up to around $433 as of June 18. Even the lowest target on the Street sits at $340, near today’s price, and the high reaches $515. Sentiment matches: 42 Buys, 14 Outperforms, 7 Holds, and zero Sells, per the breakdown TIKR tracks. Firms have kept lifting targets through June, citing Gemini traction and the AI capacity build-out, with at least one fair-value estimate revised toward the $490s.

So why has the stock not followed?

The spending is the catch

The answer is the cash. Alphabet has committed to capital expenditures of $180 billion to $190 billion in 2026, double last year’s, with management guiding 2027 higher still. That spend is hitting the income statement now. TIKR’s estimates show free cash flow margin compressing to around 5% in 2026, down from about 18% in 2025, before recovering as the infrastructure cycles through depreciation. For a business, investors bought because it gushed cash, watching that tighten is unsettling, even when growth is the cause.

The recent dilution did not help. To fund the buildout, Alphabet completed an $84.75 billion equity raise in early June, anchored by a $10 billion private placement from Berkshire Hathaway, and the stock slipped on the news.

Management frames the spending as offense. At a June 3 special call, CEO Sundar Pichai said Alphabet is seeing “strong demand for our AI solutions and services from enterprises and consumers at levels that are meaningfully exceeding our available supply.” In other words, it is building to serve demand already booked, not demand it hopes to find.

See historical and forward estimates for Alphabet stock (It’s free!) >>>

Why the demand argument has teeth

Analysts keep raising targets through the cash-flow dip because the demand evidence is concrete. Google Cloud, Alphabet’s enterprise computing and AI segment, exited Q1 2026 with a backlog of $462 billion, nearly double the prior quarter, with management expecting just over half to convert to revenue within 24 months. A backlog is signed customer commitments not yet booked as revenue, the strongest forward signal a cloud business can give. On the call, CFO Anat Ashkenazi said Cloud delivered “a record $20 billion in revenue in the first quarter while expanding margins to 33% and more than tripling operating income to $7 billion.”

The Q1 report set the tone. Alphabet posted $109.9 billion in revenue, up 22% year over year, and the stock rose 9.96% on April 29. That print gave analysts room to keep raising estimates, and earnings revisions have skewed higher since.

What you pay for the premium

None of this makes Alphabet cheap. At $368.03, GOOGL trades near 29x forward earnings and about 18x NTM EV/EBITDA, a clear premium to its peers. On TIKR’s Competitors page, Meta trades around 10x NTM EV/EBITDA and Reddit around 20x, against a peer-group mean near 7x. Alphabet earns the premium by running three category leaders at once: a dominant Search franchise, a Cloud business growing above 60% with a near-half-trillion-dollar backlog, and the world’s largest video platform, all inside one enterprise value. Whether that premium holds rests on one question: does the backlog convert on schedule, or does the capex prove an overshoot? Signed contracts plus a supply constraint are a clean setup for bulls. A forced adtech divestiture from the pending antitrust case, or a Cloud slowdown, would leave the spending stranded.

See how Alphabet performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

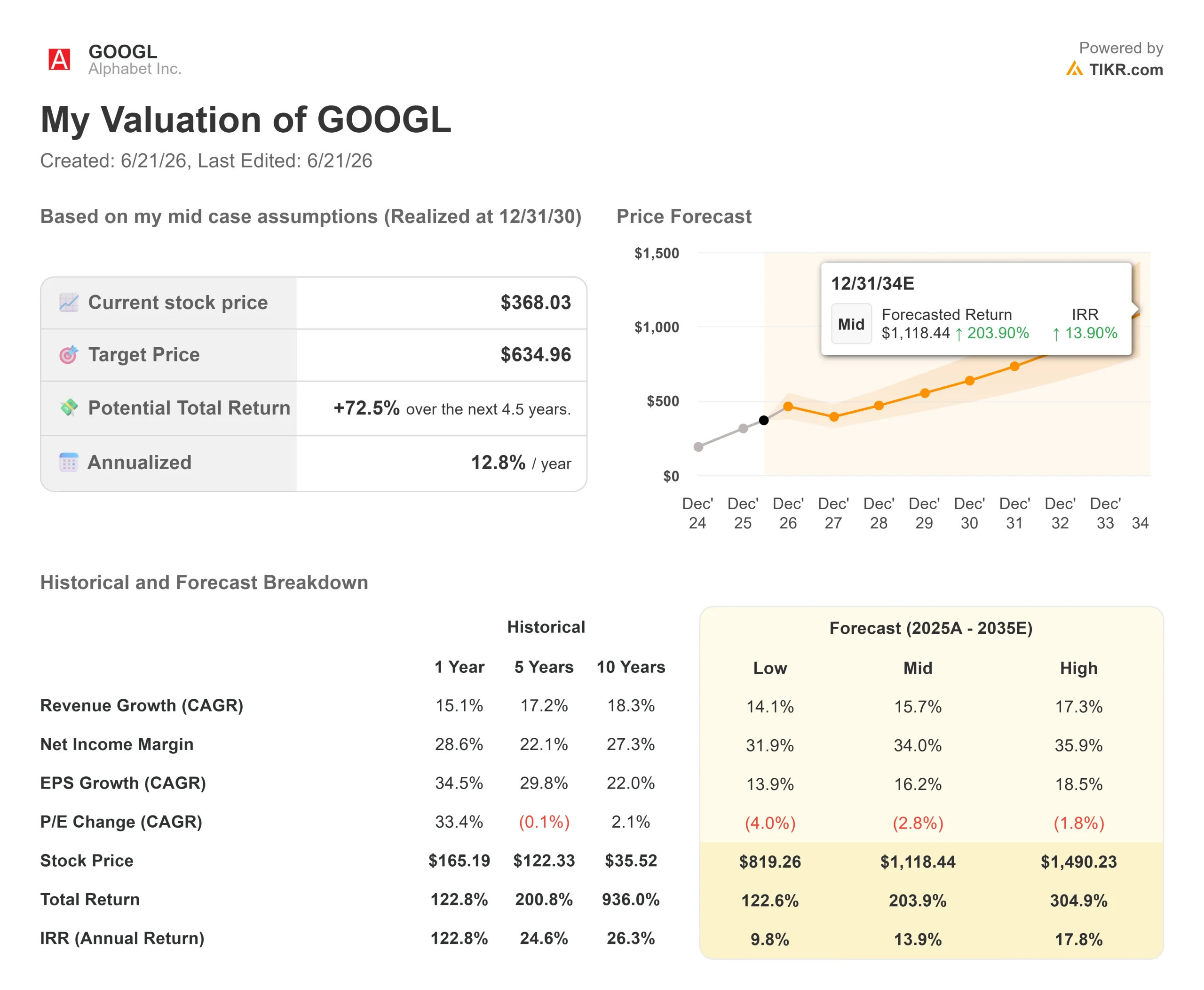

- Current Price: $368.03

- Target Price (Mid): ~$635

- Potential Total Return: ~73%

- Annualized IRR: ~13% / year

See analysts’ growth forecasts and price targets for Alphabet stock (It’s free!) >>>

On TIKR’s mid-case assumptions, realized at the end of 2030, the model targets around $635 per share. That is around 73% total return from today’s price, or about 13% annualized over the roughly 4.5-year horizon, above the current Street average of around $433.

The target rests on two revenue growth drivers: Google Cloud, where the backlog and enterprise AI demand provide a compounding base, and Search advertising, where AI Overviews and AI Mode lift revenue per query. The margin driver is Cloud operating leverage, as utilization rises across the new infrastructure. The primary risk is regulatory: a forced divestiture of Google’s Ad Exchange would remove material ad revenue from the model.

The model assumes a revenue CAGR of around 16% and a net income margin of around 34%.

Upside: the backlog converts faster than expected and margin leverage compounds, pushing toward the high case near $1,490.

Downside: Capex stays elevated while Cloud decelerates and free cash flow stays compressed, dragging toward the low case near $819.

Conclusion

The disconnect resolves at one number: Google Cloud’s growth rate. Watch it at Q2 2026 earnings, expected July 23. The threshold is clean. Cloud holding above 50% growth with steady or expanding margins means the backlog is converting and the dilution overhang fades. Cloud slipping toward the 30s while free cash flow stays compressed means the buyers stepping back had it right. The targets and the stock cannot stay apart forever, and the July print is the first real test of which one is closer.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Alphabet?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Alphabet, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Alphabet alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Alphabet on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!