Key Takeaways for Toast Stock as of June 2026

- Analysts rate Toast stock 14 Buys, 5 Outperforms, and 10 Holds with a street mean target of $34, implying 37% upside from the current price of $25.

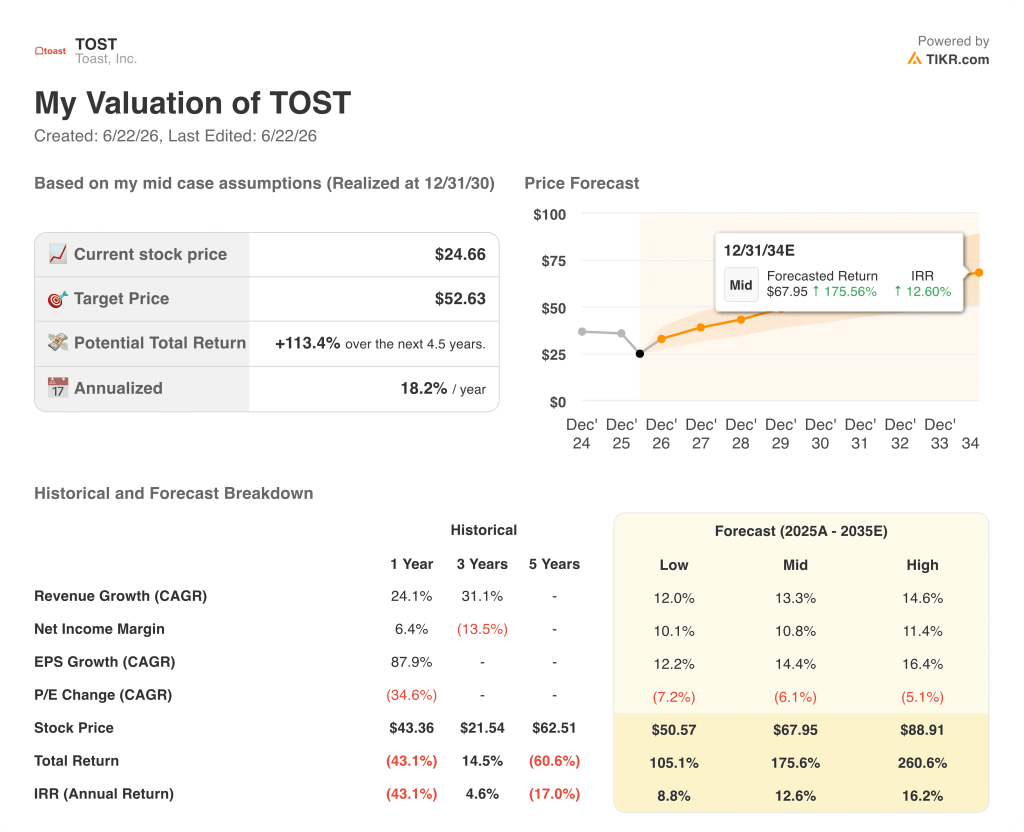

- TIKR’s mid-case model values Toast at $53 by December 2030, implying 113% total return from current levels, or 18% annualized.

- Toast stock’s normalized EPS beat the Q1 estimate by 7% while GAAP operating income margin crossed 20% for the first time, reaching 21%, a milestone the company had never previously achieved.

Toast Stock Crossed 20% GAAP Operating Margins While the Market Focused on Hardware Costs

Toast, Inc. (TOST) delivered Q1 2026 results on May 7, 2026 that showed normalized EPS of $0.29, beating the $0.27 consensus estimate by 7%, and GAAP EPS of $0.20, beating the $0.16 estimate by 28% and more than doubling the $0.09 result from one year ago.

The market punished Toast stock for a problem that does not touch its recurring revenue engine.

The operating milestone buried in the headline numbers matters more than any single quarter beat.

Toast stock’s GAAP operating income margin reached 21% in Q1 2026, crossing 20% for the first time in the company’s history, generating $110 million in operating income against revenue of $1.63 billion.

Recurring gross profit streams grew 27% year over year, and annualized recurring revenue reached $2.2 billion, up 26% from a year ago.

The company added approximately 7,000 net new restaurant locations during the quarter, ending March 31 with about 171,000 live locations, up 22% from one year prior.

Gross payment volume reached $51.3 billion in Q1, growing 22% year over year, and the total monetization take rate crossed 1% of GPV for the first time, reaching 103 basis points.

CEO Aman Narang told investors on the Q1 call: “2026 is off to a strong start. In Q1, we grew recurring gross profit streams 27% and expanded GAAP operating income margins to 21%.”

The share price reaction inverted the operating story, with TOST falling roughly 10% to 15% following earnings as Q2 EBITDA guidance landed below Wall Street expectations and management flagged that hardware memory chip costs would create a larger P&L headwind in 2027 than in 2026.

CFO Elena Gomez also confirmed on the call that the hardware pressure reflects a deliberate strategic decision rather than a deteriorating business, with Toast pulling memory chip inventory forward to protect customer shipments and accepting near-term P&L pressure in exchange for location growth continuity.

ValueAct Capital raised its stake in TOST to 12.9 million shares as of March 31, 2026, a meaningful signal from an institutional manager that focuses on long-duration business quality over short-term earnings optics.

For full-year 2026, management raised guidance, now expecting recurring gross profit of $2.29 billion to $2.32 billion, growth of 21% to 23%, with adjusted EBITDA of $790 million to $810 million.

Is Toast Stock Undervalued in 2026? What the Estimates Say

Toast stock’s earnings power is building faster than the current price reflects, and the Q1 data makes that case directly.

Normalized EPS came in at $0.29 for Q1 2026, against a $0.27 estimate, a 7% beat, and up 47% from the $0.20 normalized figure one year ago, the kind of annual acceleration that typically commands a re-rating upward rather than a 50% collapse from the 52-week high.

Consensus now projects TOST’s normalized EPS at $0.32 for Q2 2026, $0.36 for Q3, and $0.35 for Q4, a trajectory that implies the normalized earnings base is compounding through a year that management itself has characterized as one of deliberate reinvestment.

The EBITDA line reinforces the earnings beat, with Q1 EBITDA reaching $179 million against a $168 million estimate, a 6% beat, with the EBITDA margin expanding to 11% from 10% a year ago.

Toast stock’s SaaS gross margin exceeded 80% for the first time in company history during Q1 2026, reaching 81%, expanding nearly 300 basis points year over year as AI-assisted support automation begins to compress service delivery costs.

The Street’s 14 Buy ratings and 10 Hold ratings reflect a concrete divide, with bulls seeing the recurring revenue flywheel, the 27% gross profit stream growth, and the GAAP profitability milestone as a re-rating setup once hardware costs normalize, while the Hold camp treats the near-term EBITDA guidance shortfall as a reason to wait for a cleaner setup before committing.

The 19 Buy and Outperform ratings against 10 Holds, and a mean price target of $34 implying 37% upside from $25, suggest the majority of covering analysts view the current drawdown as a setup rather than a structural problem.

The open question for the Street is whether Toast IQ Grow, which showed an 8% sales lift in pilot restaurants and now counts 40,000 weekly active locations using the platform, converts into a measurable ARPU acceleration before the next earnings call, or remains a 2027 revenue contributor.

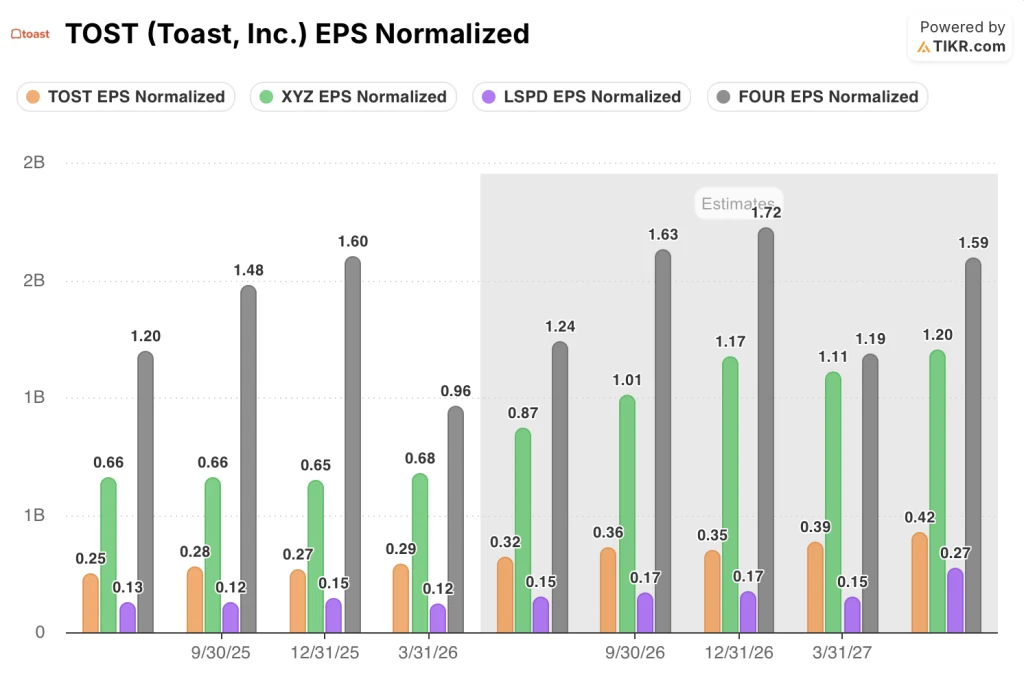

Toast Stock Trails Block and Shift4 on Normalized EPS but Leads Lightspeed Across Every Period

Toast posted normalized EPS of $0.29 in Q1 2026, ahead of Lightspeed Commerce’s (LSPD) $0.12 but trailing Block’s (XYZ) $0.68 and Shift4 Payments’ (FOUR) $0.96 in the same quarter.

The forward trajectory narrows that gap meaningfully: consensus projects Toast stock’s normalized EPS reaching $0.39 by Q1 2027, a 34% sequential climb from the $0.29 Q1 2026 actual, while Lightspeed’s estimate holds at $0.15 across the same window.

Shift4 carries the highest absolute EPS in the peer set at $1.72 estimated for Q4 2026, but Toast stock’s growth rate from $0.29 to $0.39 over four quarters outpaces Lightspeed’s flat trajectory and reflects the operating leverage that the GAAP margin milestone already confirmed.

TIKR’s $53 Target on Toast Stock: The Recurring Revenue Case

TIKR’s mid-case model values Toast stock at $53 by December 2030, implying 113% total return from the current price of $25, or 18% annualized over 4.5 years.

The path to that target depends on the recurring revenue engine maintaining the momentum already visible in Q1 2026, including 27% recurring gross profit growth, a total take rate that crossed 103 basis points for the first time, and SaaS gross margins that reached 81% and continue expanding as AI drives support automation.

Location growth is the compounding lever that makes the model credible, with 171,000 live locations at 22% annual growth and a TAM that now extends into enterprise chains, hotel food and beverage, and retail beyond the core independent restaurant market, giving each new cohort of locations a platform with higher ARPU potential than the one before it.

Toast stock is undervalued at current levels, with the market pricing in permanent hardware margin drag while the normalized earnings trajectory and recurring revenue base tell a compounding story that the $25 price does not reflect.

Should You Invest in Toast, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Toast, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Toast, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TOST stock on TIKR for Free →