Key Stats for Vistra Stock

- Current Price: $163.75

- Target Price (Mid): ~$173

- Street Target: ~$223

- Potential Total Return: ~6%

- Annualized IRR: ~1% / year

- Earnings Reaction: (4.05%) (May 7, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

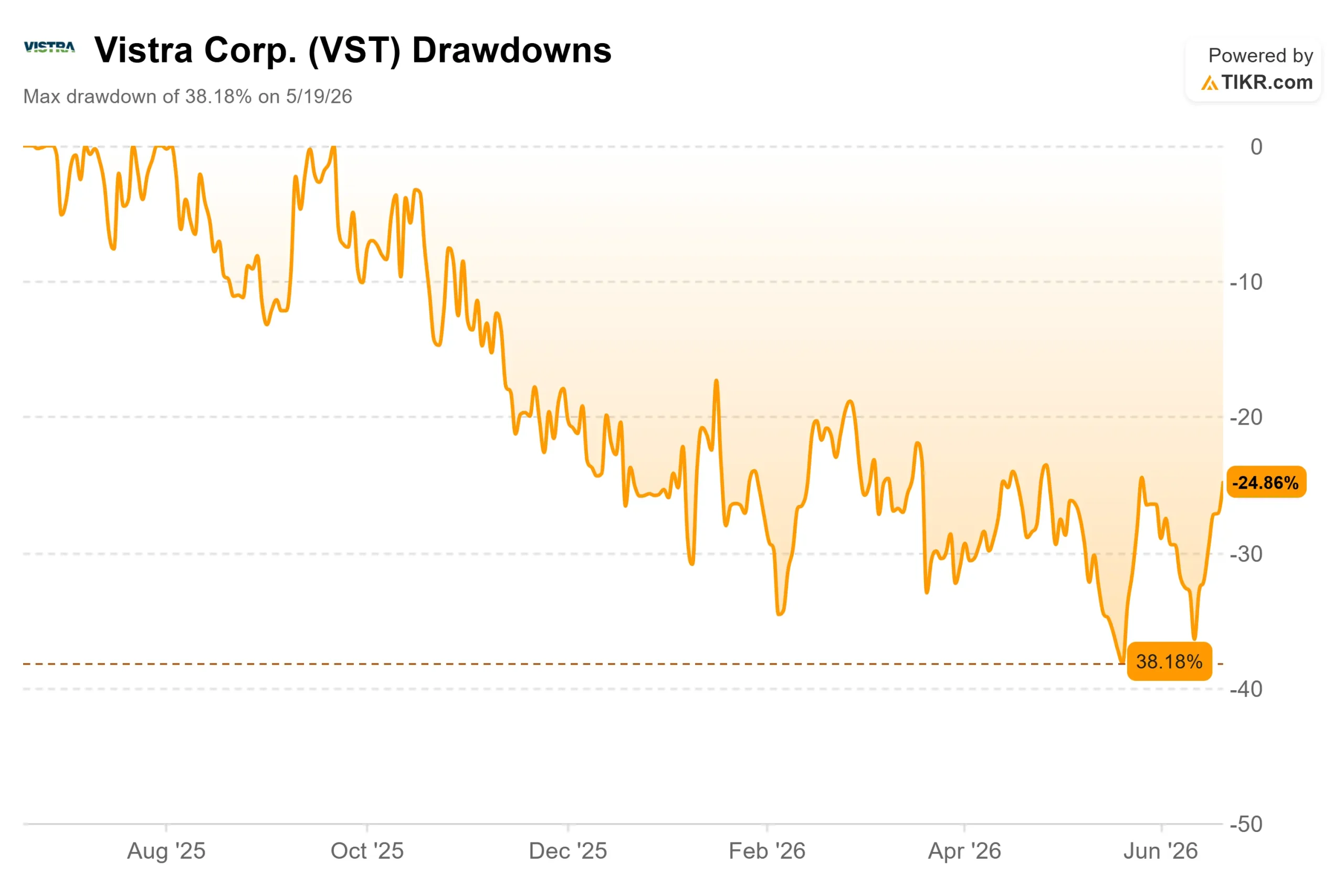

Vistra (VST) just got pulled into the center of the AI infrastructure story, and the market is still deciding what that is worth. The stock rose about 11% over the past month and closed at $163.75 on June 18, recovering off a year that saw it fall 38% from its high. The excitement is real, and so is the disagreement underneath it.

The catalyst was concrete. On June 11, KKR launched Helix Digital Infrastructure, a new company built to finance AI infrastructure at hyperscaler scale with more than $10 billion in committed capital. Vistra joined as a founding investor and Helix’s preferred power provider, alongside Nvidia as a technology partner and the Kuwait Investment Authority as a backer, a role detailed in the company’s investor relations materials. For a power generator, being the designated electricity supplier to a $10 billion AI buildout is the demand signal bulls have waited two years to see.

The question is whether that signal changes the cash flows or just the narrative. The bull case says the AI power era has barely started, and Vistra owns the fleet to serve it.

Why Helix Matters Beyond the Headline

Helix lands harder than a typical partnership because it fits what management has described all year. On the Q1 2026 earnings call, CEO Jim Burke put it plainly: “the load growth is real and is actualizing, and that creates meaningful opportunities for Vistra to support all its customers from residential to commercial and industrial, including data centers.” Helix is that load-taking contractual form.

Vistra is not a small player here. Its generation fleet is expected to reach nearly 50,000 megawatts by year-end 2026, and it has already signed more than 5,000 megawatts of hyperscaler power purchase agreements, which are long-term contracts to sell power to a specific customer at fixed terms. That includes 20-year deals with Meta for roughly 2,600 megawatts at its PJM nuclear sites. Being Helix’s preferred provider gives Vistra a channel to turn existing capacity into contracted, AI-linked cash flows instead of leaving it exposed to volatile merchant prices.

Analysts moved with the stock. On June 12, Morgan Stanley’s David Arcaro reiterated his bullish stance and $212 target, citing Vistra’s Helix role as a way to speed up contracting on its existing fleet. That is the bull thesis in one line: a faster path from idle capacity to signed offtake.

See historical and forward estimates for Vistra stock (It’s free!) >>>

The Numbers Behind the Recovery

The operational case is strong. Vistra delivered a record $1.494 billion in adjusted EBITDA in Q1 2026, up about 20% year over year, on revenue of $5.64 billion. CFO Kris Moldovan credited “strong realized revenue across the fleet, higher capacity revenues in PJM and the contribution from the assets we acquired in late 2025 from Lotus.” Generation carried the quarter while retail absorbed an unusually mild Texas winter.

The biggest catalysts are still outside guidance. The pending 5,500-megawatt Cogentrix gas acquisition, set to close in the second half of 2026, and the Meta nuclear PPAs are both excluded from current numbers. Vistra sees more than $10 billion of cash generation across 2026 and 2027 and has already returned about $600 million to shareholders this year through buybacks and dividends.

Valuation is where it gets complicated. Vistra trades at about 10x forward EV/EBITDA, which is not demanding for a generator with this growth. Its closest listed peer, AES Corporation, trades higher at roughly 17x, so Vistra screens cheaper there. But AES carries a much lower forward P/E of about 7x versus Vistra’s 16x, so the discount depends on which multiple you trust, and the two businesses differ enough that the comparison only goes so far.

The real risk is leverage. Vistra carries about $19.3 billion of net debt, or 2.84x net debt to EBITDA, meaningful for a capital-intensive business buying a $4.7 billion gas portfolio while funding new development. Investment-grade ratings from both Fitch and S&P lower that risk, but the balance sheet is why the AI optionality has not pushed the model target higher.

See how Vistra performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $163.75

- Target Price (Mid): ~$173

- Potential Total Return: ~6%

- Annualized IRR: ~1% / year

See analysts’ growth forecasts and price targets for Vistra stock (It’s free!) >>>

The mid-case rests on two drivers: ERCOT load growth that management pegs at 5% to 6% a year through 2030, and rising PJM capacity revenue as data center demand firms up. It assumes revenue growth of around 6% and a net income margin near 14%. The margin driver is contracted power replacing merchant exposure, exactly what Helix and the Meta PPAs are built to do. The primary risk is the same story in reverse: if ERCOT load grows slower than management projects, the earnings step-change never arrives.

The upside case reaches around $204 if margins expand and load growth runs hot. The downside case falls to around $126, a 23% loss, if mild weather and slower contracting pull the trajectory back toward steady-state utility economics. The thin mid-case return is not pessimistic about the business. It is that the stock has already climbed to $163.75, closing the gap to fair value that earlier pullbacks had opened.

Conclusion

The Helix deal is a genuine demand signal, but the stock has already priced in much of it. The next real test is the Cogentrix close in the second half of 2026, when management updates its 2026 guidance and 2027 EBITDA opportunity to finally include the acquisition and the Meta PPAs. A raise that lifts 2027 EBITDA well above the current midpoint would validate the run and reopen the high case. A muted update, or any sign that ERCOT load is tracking below 5% to 6%, would confirm the mid-case caution and leave the stock priced for a low single-digit return. Watch the close, and watch the load number that comes with it.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Vistra?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Vistra, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Vistra alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!