Key Stats for Pepsi Stock

- Past-Week Performance: -0.6%

- 52-Week Range: $128 to $171

- Current Price: $165

What Happened to Pepsi Stock?

PepsiCo (PEP) traded at $165 on February 20, a price weighed down by below-consensus 2026 EPS guidance of $7.50 to $8.00 against analyst expectations of $8.44, a California court ruling blocking but not dismissing a Frito-Lay price discrimination class action, and an FDA announcement to review the GRAS safety status of processed ingredients, all landing within the same week.

At the CAGNY conference on February 18, CEO Ramon Laguarta detailed a sweeping portfolio transformation targeting Lay’s, Tostitos, Gatorade, and Quaker simultaneously in 2026, alongside new protein, fiber, and mini-meal launches including Doritos Protein in spring and a full Quaker relaunch in the second half of the year.

The transformation responds directly to two simultaneous structural headwinds: GLP-1 drug adoption reaching roughly 20% of U.S. households and driving an estimated $12 billion in long-term snack industry sales losses, and lower-income consumer spending pressure that forced price cuts of up to 15% on Lay’s and Doritos.

Investors are beginning to reconsider Pepsi stock less as a stable consumer staple and more as a company in active turnaround, with Elliott Investment Management’s September 2025 intervention having already triggered a North America supply chain review, two new board directors, and a record productivity push now entering its second consecutive year.

Rachel Ferdinando, Pepsi Foods U.S. CEO, stated that “we’ve spent the past year listening closely to consumers, and they’ve told us they’re feeling the strain,” as the company simultaneously cut prices, accelerated reformulation across its largest brands, and committed to eliminating all artificial colors and flavors by end of 2027.

On the legal front, while U.S. District Judge Monica Ramirez Almadani blocked class-action status in the Frito-Lay price discrimination lawsuit on February 19, she allowed plaintiffs to amend and refile claims, keeping alive a case that accused PepsiCo of favoring large retailers over independent convenience stores across thousands of transactions.

PepsiCo’s simultaneous battles on four fronts, consumer affordability, GLP-1 dietary disruption, regulatory scrutiny of processed ingredients, and activist-driven restructuring, make its long-term 100 basis point margin expansion target and return to mid-single-digit organic growth the central test of whether this transformation delivers or merely delays a more serious reckoning.

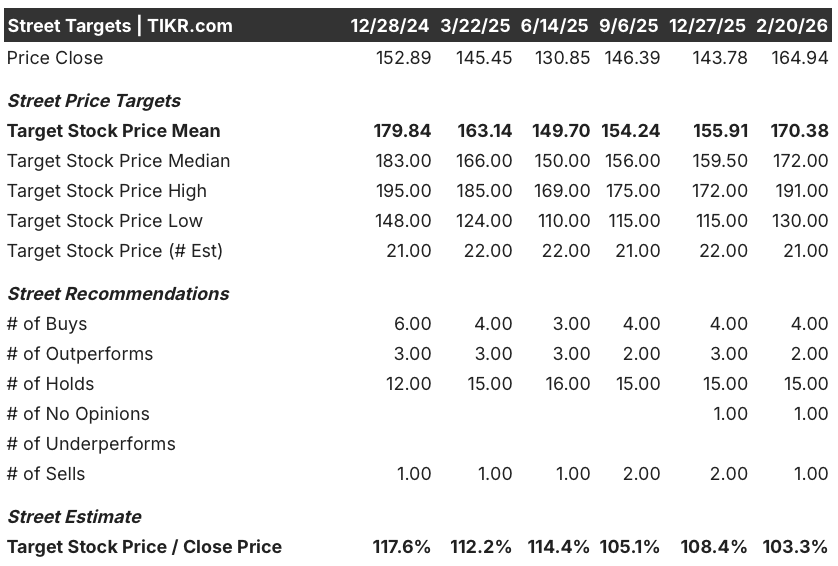

Wall Street’s Take on PEP Stock

Despite the post-CAGNY selloff and below-consensus 2026 EPS guidance, Pepsi stock’s sweeping portfolio transformation across Lay’s, Tostitos, Gatorade, and Quaker, combined with record productivity tailwinds carrying into 2026, positions the stock’s recovery as a volume-driven execution story rather than a valuation re-rating.

The fundamental case rests on Street estimates projecting 2026 revenue of $98.2 billion, up 4.6% year-over-year, normalized EPS of $8.62, up 5.9%, and EBITDA margins expanding to 19.9% from 19.6% in 2025, suggesting the business still compounds even in a difficult consumer environment.

Wall Street currently prices 21 analyst targets at a mean of $170.38, with 4 buys and 2 outperforms against 15 holds and 1 sell, implying only 3.3% upside from the current $164.94 price and signaling that conviction remains limited until volume trends confirm the turnaround.

The target range runs from a low of $130 to a high of $191, a gap wide enough to reflect genuine disagreement over whether PepsiCo’s affordability investments and brand restaging can restore volume growth before GLP-1 headwinds and FDA regulatory scrutiny on processed ingredients accelerate structural demand erosion.

What Does the Valuation Model Say?

Even accounting for the transformation underway, a mid-case valuation model prices PEP at $220.80 by December 31, 2030, projecting a 33.9% total return and a 6.2% annualized IRR, a modest proposition for a company juggling activist pressure, pricing rollbacks, and a $12 billion long-term snack industry demand threat simultaneously.

The primary risk is a compounding margin squeeze, where surgical price cuts on Lay’s and Doritos, increased advertising spend, GLP-1-driven volume pressure, and potential GRAS regulatory costs all hit the income statement simultaneously before productivity savings and volume recovery can offset them.

At $164.94, PEP stock looks like a wait-and-see, with the bull case requiring successful execution across too many simultaneous bets for the current 3.3% upside to analyst consensus to justify meaningful position-building ahead of concrete volume recovery data.

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.