Key Takeaways for Elastic Stock

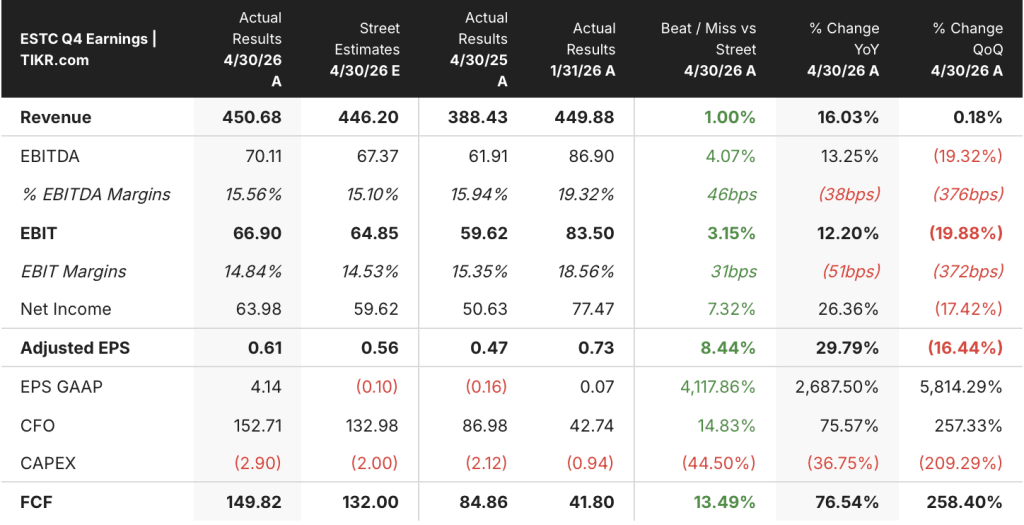

- Elastic stock posted Q4 FY2026 revenue of $450.68 million, growing 16% year over year and beating the $446.20 million Street estimate.

- Gross margins held at 76% in Q4 FY2026 while CRPO accelerated to 20% growth, signaling revenue recognition is lagging the commitment curve.

- The TIKR mid-case model targets Elastic stock at around $127, implying roughly 110% total return over the next 4.9 years at an annualized rate of around 16%.

- Operating margins turned positive at 0.2% in Q3 FY2026 before a seasonal Q4 reversal to -4%, framing FY2027’s guided 19% non-GAAP operating margin as a structural step-change, not a modest improvement.

Elastic stock is trading at $60 while the income statement shows a business where gross profit has compounded 24% year over year and the cost structure is about to be restructured with AI-driven efficiency gains. TIKR’s tools let you map this margin inflection before the market does. Analyze Elastic stock financial data on TIKR for free →

Elastic Stock Posts Record Multiyear Commitments as AI Drives Platform Consolidation

Elastic N.V. (ESTC) is a search AI company that provides a unified data platform for enterprise search, observability, and security, used by organizations to ingest, store, and analyze massive volumes of unstructured data at scale.

The company closed Q4 FY2026 on April 30, 2026, reporting total revenue of $450.68 million and delivering its seventh consecutive quarter of field execution above guidance.

The number that makes the AI demand story undeniable is CRPO growth accelerating 500 basis points to 20% year over year, reaching $1.2 billion in committed backlog, while RPO grew 28% to $1.98 billion, the highest year-over-year RPO growth in four years.

Sales-led subscription revenue, which excludes the smaller monthly self-serve cloud business and represents Elastic’s strategic core, grew 19% year over year to $375 million in Q4.

CEO Ash Kulkarni was direct on the Q4 earning call: “organizations are increasingly choosing Elastic for their long-term AI transformations and making larger multiyear commitments to standardize on our platform for the future.”

The mechanism behind this commitment surge runs across three converging forces. First, Elastic’s position as a context platform for AI pipelines, where enterprises use the company’s hybrid search, vector database, and newly acquired Jina AI embedding models to ground LLM outputs in real-time proprietary data rather than moving petabytes to external models.

Second, the agentic SOC and SRE capabilities in security and observability are winning displacement deals against legacy SIEM vendors, evidenced by an eight-figure Fortune 50 financial services win in Q4 and the CISA SIEM-as-a-Service contract, which has already exceeded its initial $26 million commitment as more civilian agencies onboard.

Third, the new metrics offering, built on a columnar architecture competitive with Prometheus, opens a segment of the observability market Elastic had not previously targeted, with the field team described at the Bank of America conference as eager to sell it without incentives.

Looking forward, management guided FY2027 total revenue of $1.985 billion to $2 billion, representing 14.6% year-over-year growth at the midpoint, with a quarterly growth trajectory that starts at 13% in Q1 and accelerates to its highest point in Q4.

Non-GAAP operating margin is guided at approximately 19% for FY2027, up roughly 2.5 percentage points from the FY2026 full-year print, driven by AI-led internal automation reducing operational complexity across every function.

Elastic stock’s commitment backlog tells a different story than the headline revenue growth rate. The CRPO-to-revenue gap is where the next 12 months of acceleration lives. See how Elastic stock’s backlog converts to revenue on TIKR for free →

Elastic Stock’s Gross Profit Grows 25% While the Cost Structure Prepares to Inflect

Elastic stock’s revenue has grown consistently across the eight quarters ending April 30, 2026, moving from $350 million in Q1 FY2025 to $451 million in Q4 FY2026, with year-over-year growth rates ranging from 16% to 20% across that period.

The more important story lives below the revenue line, where gross profit grew 16% year over year in Q4 FY2026 to $340 million on gross margins of 76%, and grew 24% year over year in Q1 FY2026 to $320 million when the highest margin quarter of the trailing eight-period set was established.

Elastic stock’s gross margin trajectory is the most stable figure on the income statement: 74% in Q1 FY2025, expanding to 77% by Q1 FY2026, then stabilizing in the 75% to 77% range across the four most recent quarters, a pattern that shows durable unit economics that are not deteriorating as the business scales.

Total operating expenses grew from $290 million in Q4 FY2025 to $360 million in Q4 FY2026, a 24% year-over-year increase, running ahead of revenue growth in that quarter, which partially explains the Q4 operating margin printing at -4%.

SG&A held at $230 million in Q4 FY2026, while R&D expanded from $90 million to $120 million over the same four-quarter trailing period, reflecting deliberate investment in embedding model development through the Jina AI acquisition and AI agent capabilities for the security and observability platforms.

The gap between Elastic stock’s 76% gross margin and its -4% operating margin in Q4 is not a structural problem; it is a 79-point spread that management has explicitly targeted for compression, guiding non-GAAP operating margin to approximately 19% in FY2027 and approximately 25% by FY2029.

The income statement mechanism is operating leverage: the cost structure is being reshaped by AI-driven automation across engineering, marketing, and finance functions, which means future revenue growth flows through to operating income at a higher rate than historical periods.

Operating income moved from -$30 million in Q4 FY2025 to $0 million in Q3 FY2026 before returning to -$20 million in Q4 FY2026, a seasonal pattern that should be read against the non-GAAP full-year delivery of 16.4% operating margin in FY2026 and the 19% guide for FY2027.

Elastic Stock Trails Datadog and Dynatrace on Gross Margin, but the Eight-Quarter Trend Tells a Different Story

Elastic stock posted gross margins of 74% in Q1 FY2025, expanded to 77% by Q1 FY2026, and settled at 75% in Q4 FY2026, a 2-percentage-point net improvement across the full eight-quarter period.

Datadog (DDOG) held gross margins between 79% and 81% across the same eight quarters, never dipping below 79%, with Q4 FY2026 printing at 79%.

Meanwhile, Dynatrace (DT) maintained the tightest range of the three, running from 81% to 82% across all eight quarters and landing at 81% in Q4 FY2026, a 6-percentage-point structural premium over Elastic stock at the same period end.

The gap is real, but the direction of travel favors Elastic stock: while Datadog compressed from 81% in Q1 FY2025 to 79% in Q4 FY2026, Elastic stock expanded across the same window, narrowing the Datadog gap from 7 percentage points to 4 percentage points in eight quarters.

Is Elastic Stock Undervalued in 2026? TIKR’s $127 Model Points to 110% Upside

TIKR’s mid-case model values Elastic stock at around $127 from a current price of $60, implying total return of approximately 110% over the next 4.9 years at an annualized rate of around 16%.

The mid-case assumes revenue CAGR of approximately 11% and net income margin expanding to approximately 19%, producing a stock price of around $158 at 4/30/31. That scenario requires the FY2027 non-GAAP operating margin guide of 19% to hold and the CRPO acceleration to continue converting into revenue through FY2029 as management has guided.

If CRPO growth sustains above 20% and the metrics product contributes meaningful bookings by FY2028 as management indicated, the high case produces a stock price of around $204 with a total return of approximately 239% and an annualized IRR of around 15%.

If revenue growth decelerates toward the low-case assumption of approximately 10% CAGR as macro headwinds compress enterprise software spending, the model produces a stock price of around $119 at a total return of approximately 97% and an annualized IRR of around 8%.

Is Elastic stock a buy in 2026?

Elastic stock trades at $60, more than 40% below its 52-week high of $96, while the business just reported 20% CRPO growth and a record quarter for multiyear commitments.

TIKR’s mid-case model puts the target at around $127, implying around 110% total return.

Whether the stock is a buy depends on confidence in the FY2027 operating margin guide of 19% and the revenue acceleration trajectory from Q1 to Q4 of that fiscal year.

Should You Invest in Elastic N.V.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Elastic N.V. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Elastic N.V. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ESTC stock on TIKR for Free →