Key Takeaways:

- Eaton is executing a comprehensive growth transformation through strategic data center expansion, capacity investments, and the transformative Boyd liquid-cooling acquisition across electrical, aerospace, and industrial markets.

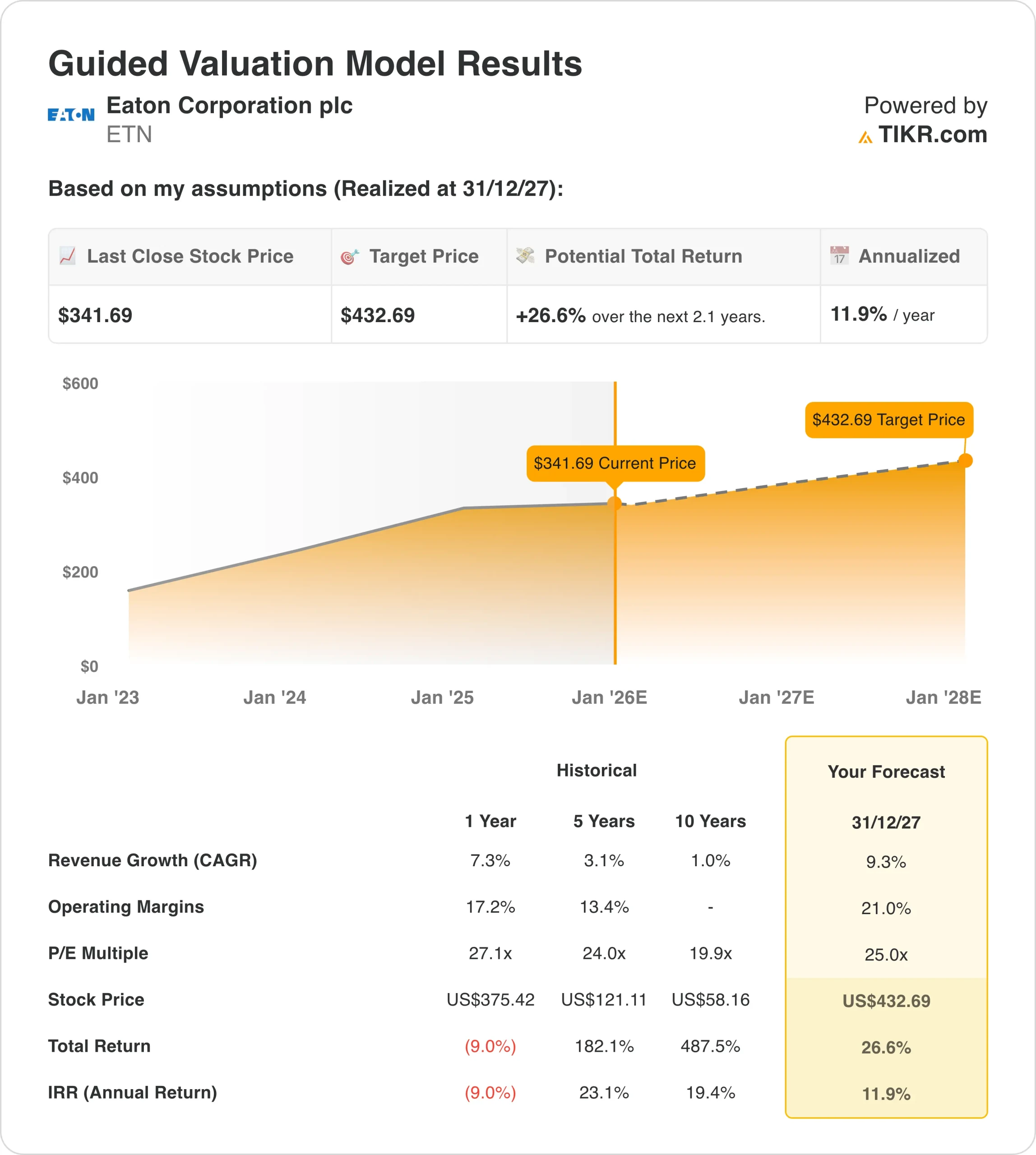

- ETN could reasonably reach $433/share by December 2027, based on our valuation assumptions.

- This implies a total return of 27% from today’s price of $342/share, with an annualized return of 12% over the next 2.1 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Eaton Corporation (ETN) is setting new benchmarks in the power management segment through strategic technology evolution, addressing data center infrastructure, liquid-cooling solutions, and electrical distribution systems across the cloud, utility, and aerospace markets.

Eaton serves electrical and industrial customers globally through its diversified portfolio philosophy, which spans electrical distribution, power quality, and energy management solutions.

Core offerings include data center power systems, utility infrastructure, aerospace hydraulics, and electrical equipment featuring solutions from the chip to the grid. This includes white-space power distribution, gray-space electrical infrastructure, and the recently acquired liquid-cooling technology.

The power management leader delivered Q3 2025 revenue of $7 billion, with Electrical Americas posting 9% organic growth. The company’s Electrical Americas backlog grew 20% year-over-year to a record $12 billion, while data center orders accelerated 70% and sales jumped 40% versus Q3 2024.

Eaton demonstrates strong execution across strategic initiatives under the leadership of CEO Paulo Ruiz and CFO Olivier Leonetti, who joined earlier in 2025.

- The company achieved segment margins of 25% in Q3, a quarterly record up 70 basis points year-over-year.

- Electrical Americas delivered 30.3% operating margins while investing $1.25 billion in capacity expansion across 12 facilities to serve unprecedented demand.

- ETN also announced the $1.8 billion acquisition of Boyd’s thermal business, a global leader in liquid cooling for data centers.

ETN stock went public decades ago and has delivered returns of over 500% to shareholders over the last 10 years.

Here’s why Eaton stock could provide strong returns through 2027 as it capitalizes on electrification megatrends while scaling its data center solutions across diverse global deployments.

See analysts’ full growth forecasts and estimates for Eaton stock (It’s free) >>>

What the Model Says for Eaton Stock

We analyzed the upside potential of Eaton stock using valuation assumptions based on its data center dominance and market expansion opportunities across electrical infrastructure and liquid-cooling growth strategies.

Analysts see an opportunity ahead for Eaton stock, given its proven execution track record, capacity-expansion strategy, and systematic approach to building competitive advantages while maintaining exceptional profitability in the expanding electrification market.

Eaton’s diversified growth strategy provides multiple vectors, while the Boyd acquisition validates that comprehensive power and cooling solutions can drive revenue growth and customer returns in the evolving data center landscape.

Based on estimates of 9% annual revenue growth, 21% operating margins, and a normalized P/E valuation multiple of 25x, the model projects Eaton stock could rise from $342/share to $433/share.

That would be a 27% total return, or a 12% annualized return over the next 2.1 years.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Eaton stock:

1. Revenue Growth: 9%

Eaton delivered a strong third quarter 2025 performance, with 7% organic growth driven by momentum across Electrical Americas (9% organic), Electrical Global (8% organic), and Aerospace (13% organic).

The company’s order momentum accelerated significantly, with Electrical Americas rolling 12-month orders up 7% (versus 2% in Q2) and quarterly orders up over 11% sequentially. Data center orders grew nearly 70% year over year.

This growth reflects the company’s strategic positioning in high-growth markets. The mega-project announcement backlog reached $239 billion in Q3, up 18% year-over-year, with data centers representing approximately half of total announcements. The two-year cumulative backlog now stands at $2.6 trillion.

Growth drivers include explosive data center demand, with the company targeting electrical content of $1.2 million to $2.9 million per megawatt. With the Boyd acquisition adding liquid cooling capabilities, this increases to nearly $3 million per megawatt at the high end.

Management expects data center market growth of approximately 17% annually through 2030, though the liquid cooling market is explicitly projected to grow at a 35% CAGR through 2028, reaching $6-9 billion by 2028 and $15-18 billion by 2030.

The company reaffirmed 2025 guidance of 8.5-9.5% organic growth (approximately $8.87 billion at the midpoint) and provided 2026 end-market assumptions implying approximately 7% market growth.

Eaton’s book-to-bill ratio stands at 1.2 for combined Electrical and Aerospace segments every quarter and 1.1 on a rolling 12-month basis.

We used a 9% forecast, reflecting Eaton’s ability to capture electrification demand through data center expansion, utility infrastructure growth, and aerospace strength while managing capacity constraints.

This balances the company’s strong near-term momentum with execution challenges posed by ramping 12 new facilities simultaneously.

2. Operating margins: 21%

In the third quarter of 2025, Eaton achieved segment operating margins of 25%, a quarterly record up 70 basis points year-over-year, demonstrating strong operational execution across the portfolio.

Electrical Americas delivered 30.3% operating margins, up 20 basis points despite approximately 100 basis points of inefficiencies from ramping six new facilities simultaneously and absorbing tariff costs.

Electrical Global posted 19.1% margins, up 40 basis points, while Aerospace expanded margins 150 basis points to 25.9%.

The company guided to full-year 2025 segment margins of 24.1-24.5%, reflecting ongoing investments in capacity expansion and integration of recent acquisitions (Resilient Power, Fibrebond, and soon Boyd).

The company is investing strategically in next-generation capabilities, including:

- $1.25 billion capacity expansion program ($700 million completing in 2025, remainder in 2026-2027)

- Boyd’s 16 global manufacturing facilities with 500+ engineers providing liquid cooling leadership

- Medium-voltage solid-state transformers through Resilient Power acquisition

- Modular data center solutions via Fibrebond acquisition expanding white space presence

We forecast 21% operating margins, in line with management’s guidance for 2026 and recognizing that capacity expansion inefficiencies will persist through 2026 before improving.

This accounts for the company’s near-term investment phase while recognizing significant margin expansion potential as facilities mature and operating leverage improves.

3. Exit P/E Multiple: 25x

Eaton stock currently trades at a next-twelve-months P/E multiple of approximately 25.5x, reflecting its premium positioning, electrification exposure, and proven ability to generate consistent growth through infrastructure investment cycles.

Historical P/E multiples show premium valuations: 27x over the past year, 24x over the last five years, and an average of 20x over the last decade, demonstrating expanding investor confidence in the company’s secular growth drivers.

We maintain a 25x exit multiple given Eaton’s execution capabilities, secular tailwinds from electrification and data center infrastructure spending, and systematic approach to building sustainable competitive advantages through capacity investments and strategic M&A.

The company’s 19 consecutive quarters of growth demonstrate operational consistency, while partnerships with major hyperscalers and collaboration with NVIDIA on data center design from “chip to grid” validate Eaton’s strategic positioning in the evolving infrastructure landscape.

Management’s disciplined capital allocation includes the $21 billion cash generation commitment through 2030, strategic M&A investments totaling approximately $3 billion across three deals in 2025 (Resilient Power, Fibrebond, Ultra PCS for Aerospace), and the transformational $1.8 billion Boyd acquisition announced in Q3.

Management increased its total addressable market significantly with data center content per megawatt expanding from $1.2-2.4 million to nearly $3 million, with Boyd’s liquid cooling capabilities included.

Build your own Valuation Model to value any stock (It’s free!) >>>

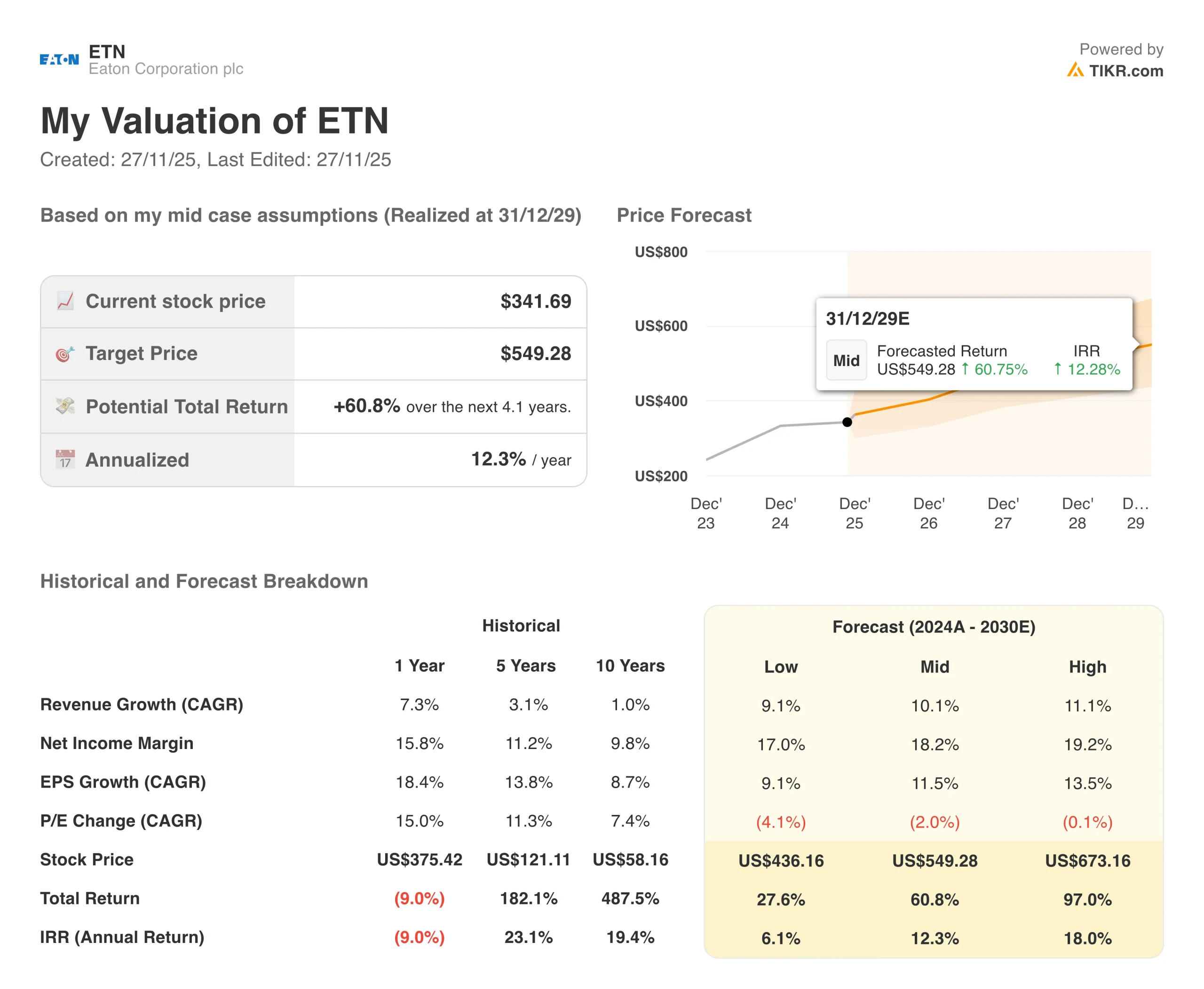

What Happens If Things Go Better or Worse?

Different scenarios for ETN stock through 2030 show varied outcomes based on data center deployment execution and capacity ramp dynamics (these are estimates, not guaranteed returns):

- Low Case: Capacity constraints persist and data center growth moderates → 6% annual returns

- Mid Case: Successful facility ramp and steady data center market share gains → 12% annual returns

- High Case: Strong Boyd integration and accelerated liquid cooling adoption → 18% annual returns

Even in the conservative case, Eaton stock offers positive returns, supported by its manufacturing footprint advantage and proven ability to maintain customer relationships and operational discipline, while competitors struggle with capacity limitations and integration challenges.

The upside scenario for ETN stock could deliver exceptional performance if the company successfully integrates Boyd’s liquid-cooling technology during the multi-year data center infrastructure build-out, while achieving operational excellence across 12 facility expansions and capturing the $2.6 trillion mega-project pipeline over the next several years.

See what analysts think about ETN stock right now (Free with TIKR) >>>

How Much Upside Does Eaton Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!