Key Takeaways:

- Digital Banking Surge: Q2 Holdings delivered record bookings in Q4 2025 with 26 enterprise and Tier 1 deals for the full year.

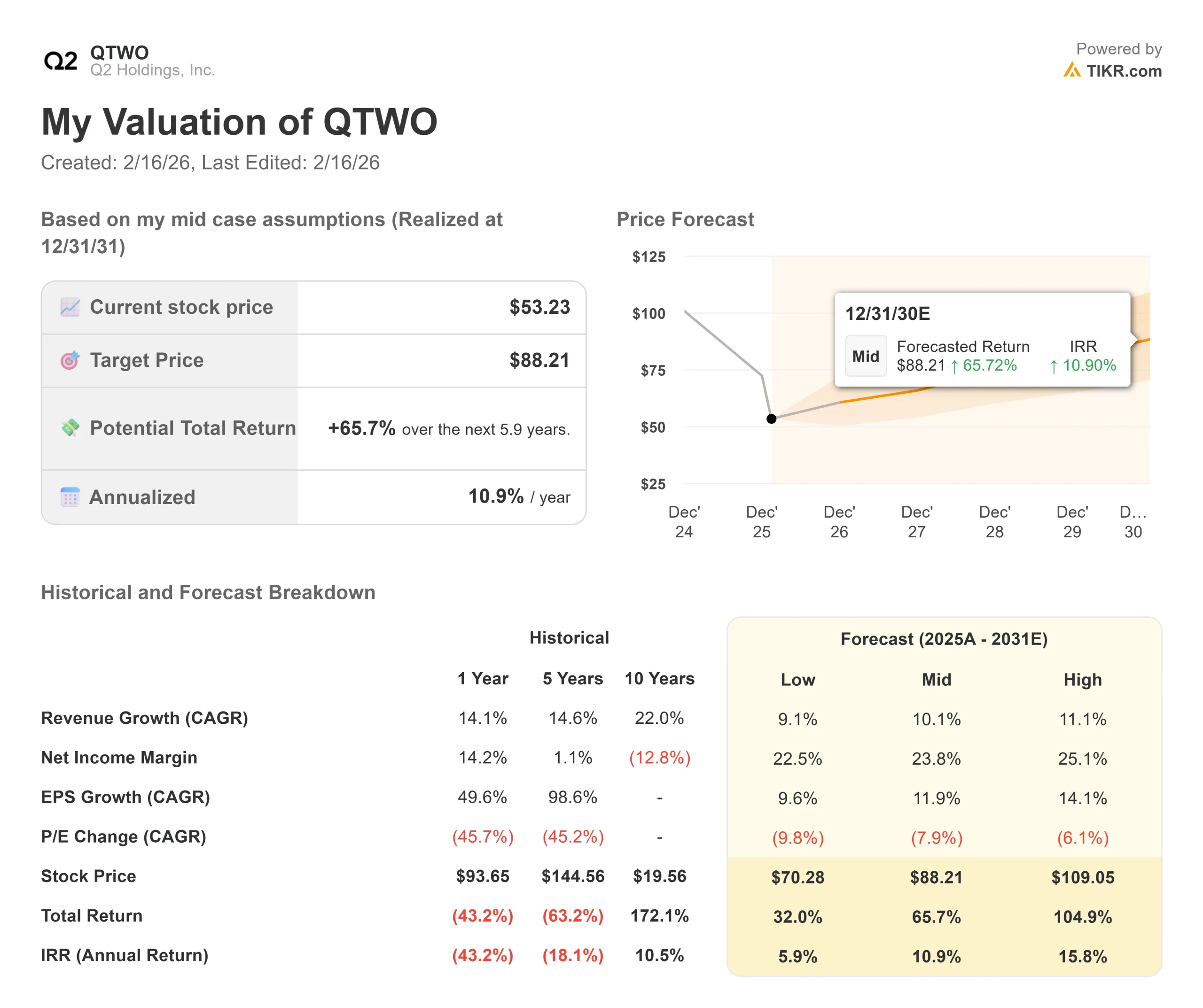

- Price Projection: Based on current execution, QTWO stock could reach $72 by December 2028.

- Potential Gains: This target implies a total return of 35% from the current price of $53.

- Annual Return: Investors could see roughly 11% growth over the next 2.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Q2 Holdings (QTWO) capped off 2025 with its strongest year as a company, delivering 16% subscription revenue growth and expanding adjusted EBITDA margins by over 400 basis points year-over-year.

The fourth quarter alone produced $56.6 million in free cash flow, marking the company’s second-largest bookings quarter ever.

CEO Matt Flake highlighted robust demand across the product portfolio, with particular strength in larger deals.

- The company closed eight Tier 1 and enterprise deals in Q4, including wins that combined relationship pricing with commercial digital banking.

- For the full year, Q2 executed 26 enterprise and Tier 1 deals, split evenly between new customers and expansions with existing clients.

- The digital banking platform continues to resonate as financial institutions prioritize deposit growth.

- With heightened competition for deposits, banks and credit unions are streamlining technology while delivering better customer experiences.

- Q2 Holdings’ commercial banking solutions processed over $4 trillion in transaction volume during 2025, representing 21% year-over-year growth.

- December 2025 was the first month ever to break $400 billion in transaction volume

- Innovation Studio has become a cornerstone of Q2 Holdings’ strategy. Nearly every new digital banking deal in 2025 included Innovation Studio, enabling faster product delivery and stronger customer engagement.

- Management believes this positions Q2 Holdings to adapt quickly as priorities like AI emerge across financial services.

- Risk and fraud solutions emerged as one of the fastest-growing product lines.

- The company signed its largest fraud deal ever with a $200 billion bank, and fraud solutions consistently performed as both stand-alone products and top cross-sell offerings.

- As fraud becomes continuous and cross-channel, financial institutions are moving away from fragmented point solutions toward more integrated approaches.

- Bank M&A activity picked up in 2025, creating another tailwind for Q2 Holdings. Of all M&A deals involving a Q2 Holdings customer, 93% chose Q2 Holdings as the go-forward solution.

- This track record in technology conversions has become a competitive advantage, helping customers derisk transactions and realize value faster.

Despite strong fundamentals and a growing product portfolio, Q2 Holdings trades at $53, offering upside for investors who recognize the company’s position in critical banking infrastructure.

See analysts’ full growth forecasts and estimates for QTWO stock (It’s free) >>>

What the Model Says for Q2 Holdings Stock

We analyzed Q2 Holdings as it transformed into a comprehensive digital banking platform with expanding fraud and relationship-pricing capabilities.

- The company benefits from structural trends that are forcing banks to modernize their technology stacks and compete more aggressively for deposits.

- Commercial banking represents a significant growth driver. As regional banks expand upmarket to capture larger operating accounts, Q2 Holdings’ mature commercial solutions and modern interface provide a durable competitive advantage.

- The company processed $4 trillion in commercial transactions during 2025, with strong momentum continuing into 2026.

- Innovation Studio creates additional leverage. The revenue-sharing model generates high-margin income while strengthening Q2 Holdings’ role as the gateway for AI and other innovations entering financial services.

- Banks are steering technology partners directly to Q2 Holdings for integration, reinforcing the company’s central position in digital banking.

Using a forecast of 10.7% annual revenue growth and 23.6% operating margins, our model projects the stock will rise to $72 within 2.9 years. This assumes a 17.9x price-to-earnings multiple.

That represents compression relative to Q2 Holdings’ historical P/E average of 33.2x (one-year). The lower multiple acknowledges the transition from hypergrowth to profitable expansion, though the company continues demonstrating strong execution across bookings and margins.

The real value lies in capturing deposit-driven digital banking demand while expanding into higher-margin products such as fraud solutions and relationship pricing across a growing customer base.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for QTWO stock:

1. Revenue Growth: 10.7%

Q2 Holdings’ growth centers on digital banking modernization and commercial expansion.

The company delivered strong bookings throughout 2025, with particular strength in larger deals weighted toward the back half.

Management expects subscription revenue growth of at least 14% in 2026, with continued momentum from relationship pricing and fraud solutions.

The pipeline remains healthy across both new customers and expansions, with Tier 1 and enterprise activity expected to follow a similar pattern to 2025.

2. Operating margins: 23.6%

Q2 Holdings has expanded adjusted EBITDA margins by approximately 550 basis points over the past year, driven by operational efficiency and a growing mix of subscription revenue.

The company completed its cloud migration in January 2026, which should drive further gross margin expansion.

Management sees continued leverage opportunities across sales, marketing, and G&A, while maintaining investments in AI R&D and product innovation.

3. Exit P/E Multiple: 17.9x

The market currently values Q2 Holdings at 18.2x earnings. We assume modest compression to 17.9x over our forecast period.

While the company has executed well and established clear profitability targets, the transition from growth-at-all-costs to balanced expansion typically commands a lower multiple.

As Q2 Holdings demonstrates consistent execution and approaches its 2030 targets of 65% gross margins and 35% EBITDA margins, the company should maintain a premium valuation among financial technology providers.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Financial technology companies face evolving customer priorities and competitive dynamics. Here’s how Q2 stock might perform under different scenarios through December 2028:

- Low Case: If revenue growth slows to 9.1% and net income margins compress to 22.5%, investors still see a 32.0% total return (5.9% annually).

- Mid Case: With 10.1% growth and 23.8% margins, we expect a total return of 65.7% (10.9% annually).

- High Case: If commercial banking and fraud solutions drive 11.1% revenue growth while Q2 Holdings maintains 25.1% margins, returns could hit 104.9% total (15.8% annually).

See what analysts think about QTWO stock right now (Free with TIKR) >>>

The range reflects execution on digital banking wins, successful cross-selling of fraud and relationship pricing products, and the company’s ability to deliver on its long-term margin targets.

In the low case, competitive pressure increases, or banks delay technology investments.

In the high case, deposit competition intensifies faster than expected, AI monetization accelerates, and bank M&A activity surges above current levels.

How Much Upside Does Q2 Holdings Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!