Key Stats for Deckers Outdoor Stock

- Past-Week Performance: 3%

- 52-week Range: $79 to $224

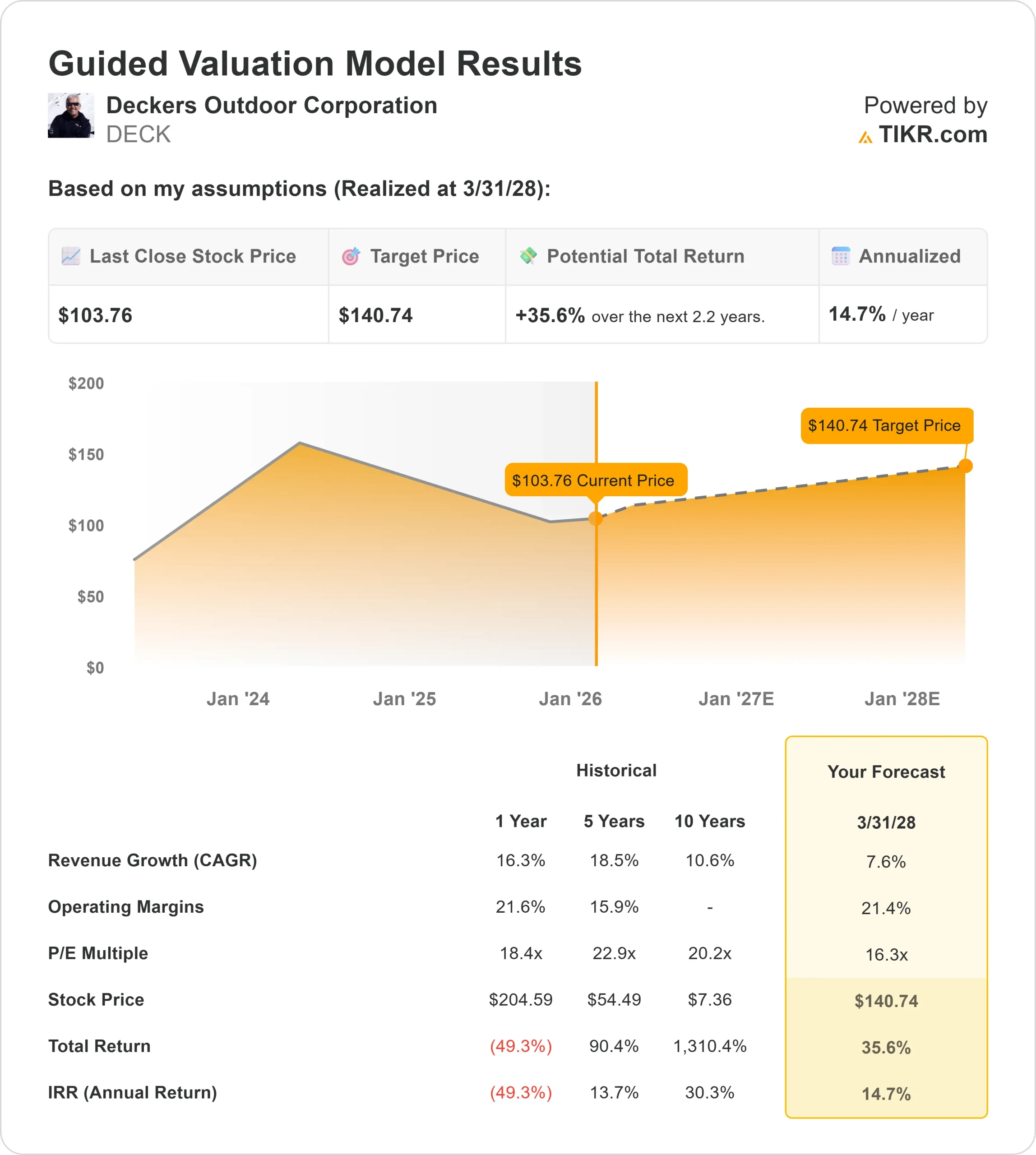

- Valuation Model Target Price: $141

- Implied Upside: 35.6% over 2.2 years

Value stocks like Deckers Outdoor with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Deckers Outdoor (DECK) fell about 3% over the past week, after trading higher earlier in the week before giving back gains and settling near $104 per share. The stock had been moving off recent lows but failed to sustain momentum as investors reassessed how much recovery to price in.

Earlier in the week, buying interest was supported by continued confidence in Deckers’ profitability and cost discipline. In recent commentary, Goldman Sachs highlighted the company’s strong margin structure and controlled inventory levels as key supports for earnings, even as top-line growth has moderated.

Despite that supportive backdrop, the rally proved difficult to extend. With DECK still down roughly 50% from highs near $224, investors appeared reluctant to push the stock materially higher without clearer evidence that demand trends are stabilizing, particularly across the company’s core brands.

As a result, some investors locked in gains late in the week, leading to a pullback despite the absence of negative earnings revisions or company-specific news. The move reflected valuation sensitivity and positioning rather than any deterioration in Deckers’ underlying business.

See analysts’ growth forecasts and price targets for Deckers Outdoor (It’s free) >>>

Is Deckers Outdoor Undervalued?

In the Guided Valuation Model above, we used these assumptions:

- Annual revenue growth: 7.6% CAGR

- Operating margins: 21.4%

- Exit P/E multiple: 16.3x

Based on these inputs, the model estimates a fair value of $141 per share, implying 35.6% total upside from the current share price over the next 2.2 years.

Business performance over the next year will be shaped largely by UGG’s ability to hold full price sell through during the fall and winter seasons, since even small changes in traffic, conversion, or discounting can materially impact revenue and gross margins.

Inventory discipline remains a key earnings lever, as lean inventory levels support pricing power, while excess product would likely force higher promotions and compress margins quickly.

HOKA’s growth trajectory also plays an important role, particularly if wholesale reorders and international expansion continue at recent rates, which would help offset slower growth in more mature categories.

Finally, operating leverage becomes increasingly meaningful if revenue stabilizes, because keeping marketing and SG&A growth below sales growth would allow earnings to recover faster than the top line.

Together, these factors explain why the market remains cautious today, while also highlighting how incremental improvements in execution could translate into outsized earnings and stock performance.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>