Key Takeaways:

- Earnings Scale: UniCredit generated €25 billion in revenue and €11 billion in net income over the last twelve months, showing strong earnings conversion after peak-rate normalization.

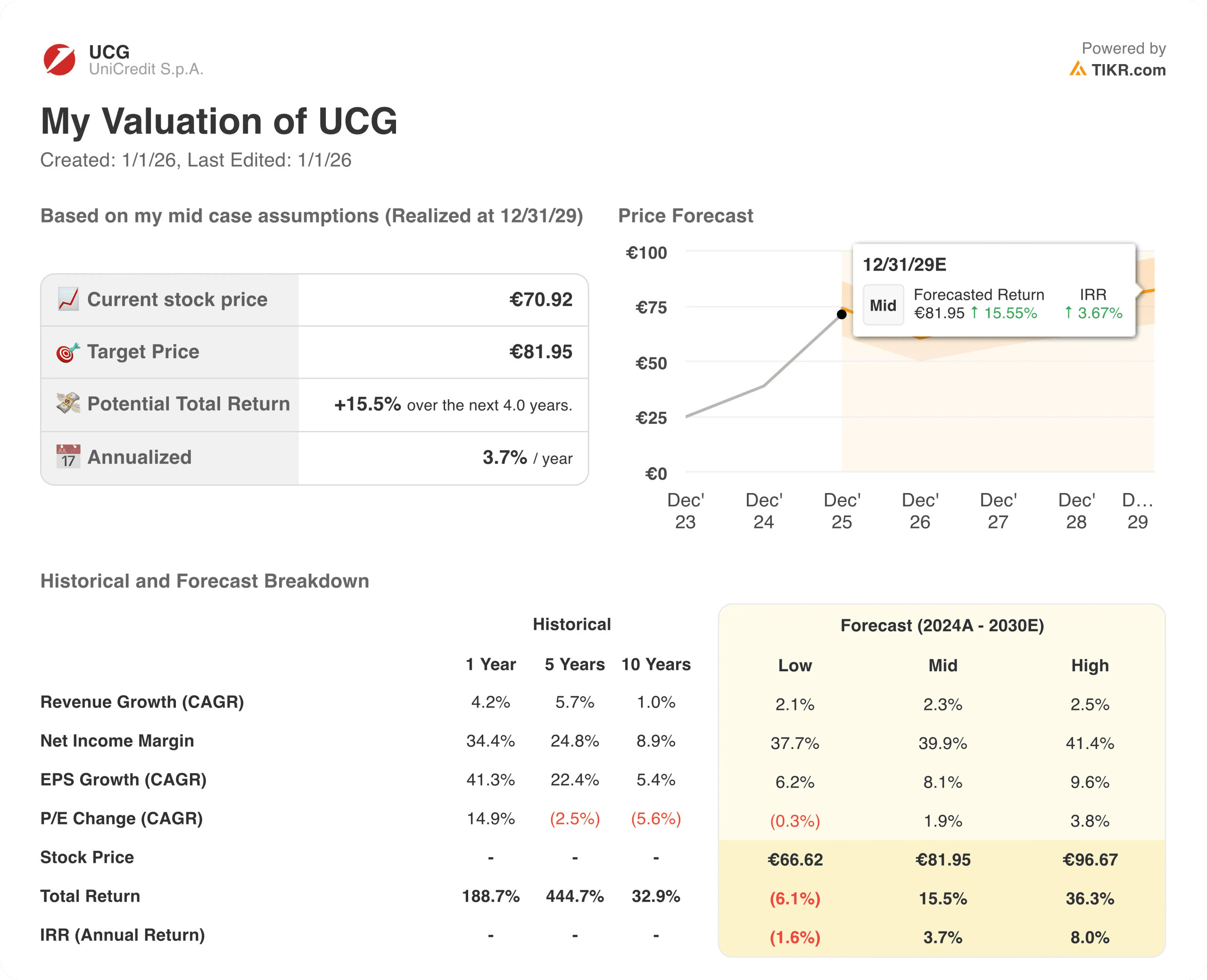

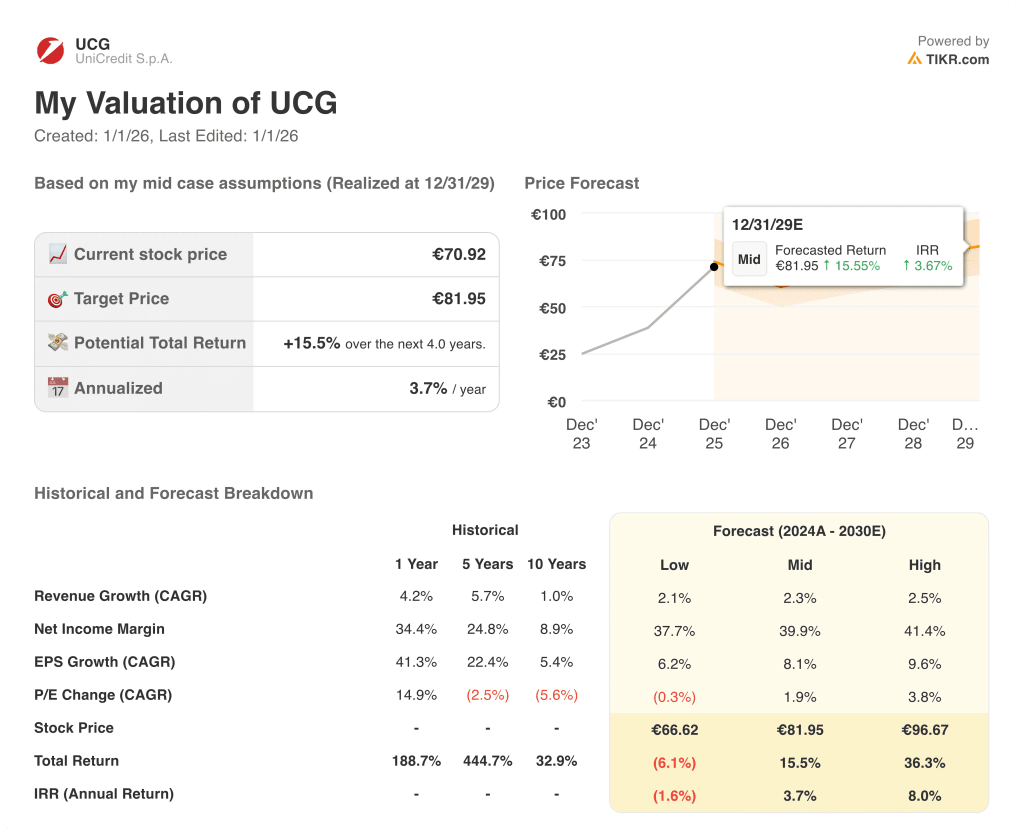

- Price Projection: Based on valuation assumptions, UniCredit stock could reach €77 by December 2027.

- Potential Gains: This target represents roughly 10% total upside from the current price near €70.

- Annual Return: The implied outcome equates to approximately 5% annualized returns over the next 2 years, anchored by capital returns and earnings stability.

UniCredit S.p.A. (UCG) is a pan-European bank with a strong presence in Italy, Germany, and Central and Eastern Europe, serving retail, corporate, and institutional clients across lending, payments, and capital markets.

Recent political clarity in Italy confirmed central bank independence and reduced systemic risk concerns, improving the operating backdrop for domestic banks with large sovereign and retail exposure.

Over the last twelve months, UniCredit generated €25 billion in revenue, reflecting stable loan volumes and net interest income resilience despite a slower rate-cut trajectory.

Net income reached €11 billion during the same period, showing how disciplined cost control and lower loan loss provisions allowed revenue to translate efficiently into profits.

Earnings efficiency remains strong with net income margins above 40%, supported by tight operating expenses and limited credit deterioration across core European markets.

Despite strong profitability and a dividend yield above 5%, the stock trades near 8 times forward earnings, raising the question of whether valuation fully reflects earnings durability as rate tailwinds fade.

What the Model Says for UniCredit Stock

We evaluated UniCredit’s valuation using stable net interest income, disciplined costs, and capital returns across core European banking markets.

Using 2% revenue growth, 63% operating margins, and an 8x exit multiple, the model reflects normalized post-cycle profitability and conservative valuation.

The model indicates UniCredit could reach €77 by 2027, implying a 10% total return or about 5% annualized returns over two years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for UCG stock:

1. Revenue Growth: 1.9%

UniCredit’s revenue expanded from €18 billion in 2022 to €25 billion LTM, largely reflecting the interest rate upcycle rather than structural balance sheet expansion.

Growth accelerated during 2022–2023, then slowed to about 5% in 2024 as lending volumes normalized across Italy and core European markets.

Net interest income growth moderated to about 3% LTM, indicating a shift from peak-rate tailwinds toward more stable banking conditions.

Forward estimates suggest revenues stabilize around €25–26 billion through 2027, pointing to low single-digit organic growth constrained by mature credit markets.

Loan growth remains limited by conservative underwriting standards, while fee income and digital services provide incremental support without fully offsetting rate normalization.

According to consensus analyst estimates, a 1.9% revenue growth assumption reflects stable core banking activity balanced against fading monetary tailwinds and limited structural expansion levers.

2. Operating Margins: 62.8%

UniCredit’s EBIT margin increased from 45% in 2021 to above 62% in 2024, showing strong operating leverage during the rate-driven earnings cycle.

Cost discipline improved materially as non-interest expenses declined while revenues rose, allowing profitability to scale faster than balance sheet growth.

Normalized net income margins exceeded 40% LTM, supported by lower loan loss provisions and controlled compensation growth across core markets.

Margins likely peaked during elevated interest rates and are expected to stabilize rather than expand meaningfully as rates normalize.

Forward projections place EBIT margins in the 61–63% range through 2027, consistent with recent execution and ongoing cost controls.

In line with analyst consensus projections, a 62.8% operating margin reflects disciplined expense management offset by normalization following exceptional rate-driven profitability.

3. Exit P/E Multiple: 8.4x

UniCredit currently trades near 8× forward normalized earnings, below long-term European banking averages despite strong profitability.

Trailing valuation multiples ranged between 8× and 10× across recent periods, reflecting macro sensitivity and earnings cyclicality.

Investor caution persists around European growth, regulation, and sovereign exposure, limiting appetite for aggressive valuation expansion.

Dividend yields above 5% anchor valuation but also cap expectations for meaningful multiple re-rating.

Regulatory uncertainty and rate normalization continue to constrain upside despite improved earnings durability.

Based on consensus market estimates, an 8.4× exit multiple balances strong cash generation and dividends against conservative European banking sentiment and limited re-rating visibility.

What Happens If Things Go Better or Worse?

European banking outcomes depend on rate normalization, credit quality, and capital discipline. Here is how UniCredit stock might look in different scenarios through 2027.

- Low Case: If rate cuts accelerate and loan growth weakens, revenue stays 2.1% and net income margin ease toward 38%→ roughly 2% annual returns.

- Mid Case: If revenue grows to 2.3% and cost control holds and net income margin remain at 40% → 4% annual returns.

- High Case: If credit quality remains strong and fee income improves, revenue grows 2.5%, and net income margins rise toward 41%→ 8% annual returns.

UniCredit has shifted into a steady earnings phase supported by capital returns, stable credit trends, and disciplined cost control.

A target price of €77 per share by 2027 is achievable if margins remain near current levels and valuation continues to reflect normalized earnings rather than renewed multiple expansion.

How Much Upside Does UCG Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!