Coterra Energy Inc. (NYSE: CTRA) trades near $26/share after a volatile period driven by shifting natural gas prices and uneven energy sentiment. Even with this backdrop, Coterra continues to stand out for its strong margins, low leverage, and consistent execution, which have helped it remain one of the most efficient producers in the sector.

Recently, Coterra has shown improved momentum as natural gas fundamentals have begun to stabilize. Production trends across its core assets have strengthened, and the company continues to operate with impressive cost discipline. These developments suggest that Coterra maintains solid earnings power even when commodity markets move cautiously.

This article outlines where analysts expect Coterra to trade by 2027 based on consensus targets and valuation model results. These figures reflect analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

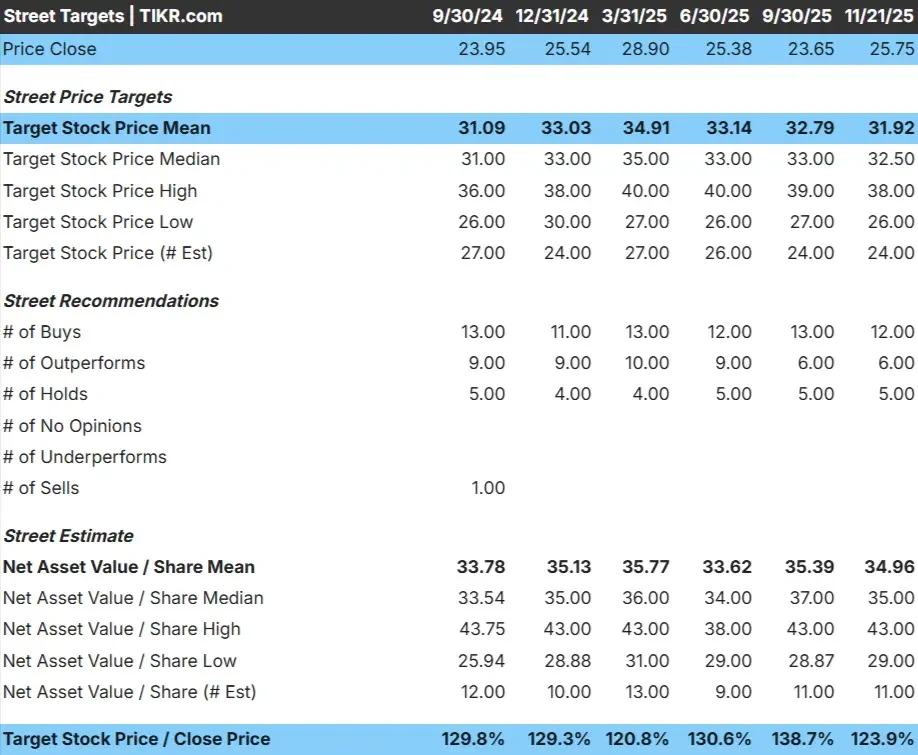

Analyst Price Targets Suggest Modest Upside

CTRA trades near $26/share, and the average analyst price target is $32/share, which implies about 24% upside. The spread between analyst estimates is relatively tight, suggesting a broadly shared view of where the stock could trend.

- High estimate: $38/share

- Low estimate: $26/share

- Median target: $33/share

- Ratings: 12 Buys, 6 Outperforms, 5 Holds

For investors, this points to modest upside. Analysts generally see Coterra as a steady operator with room to outperform if margins remain healthy and natural gas prices continue to recover. The consistency across forecasts signals confidence in Coterra’s operational stability.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

CTRA Growth Outlook and Valuation

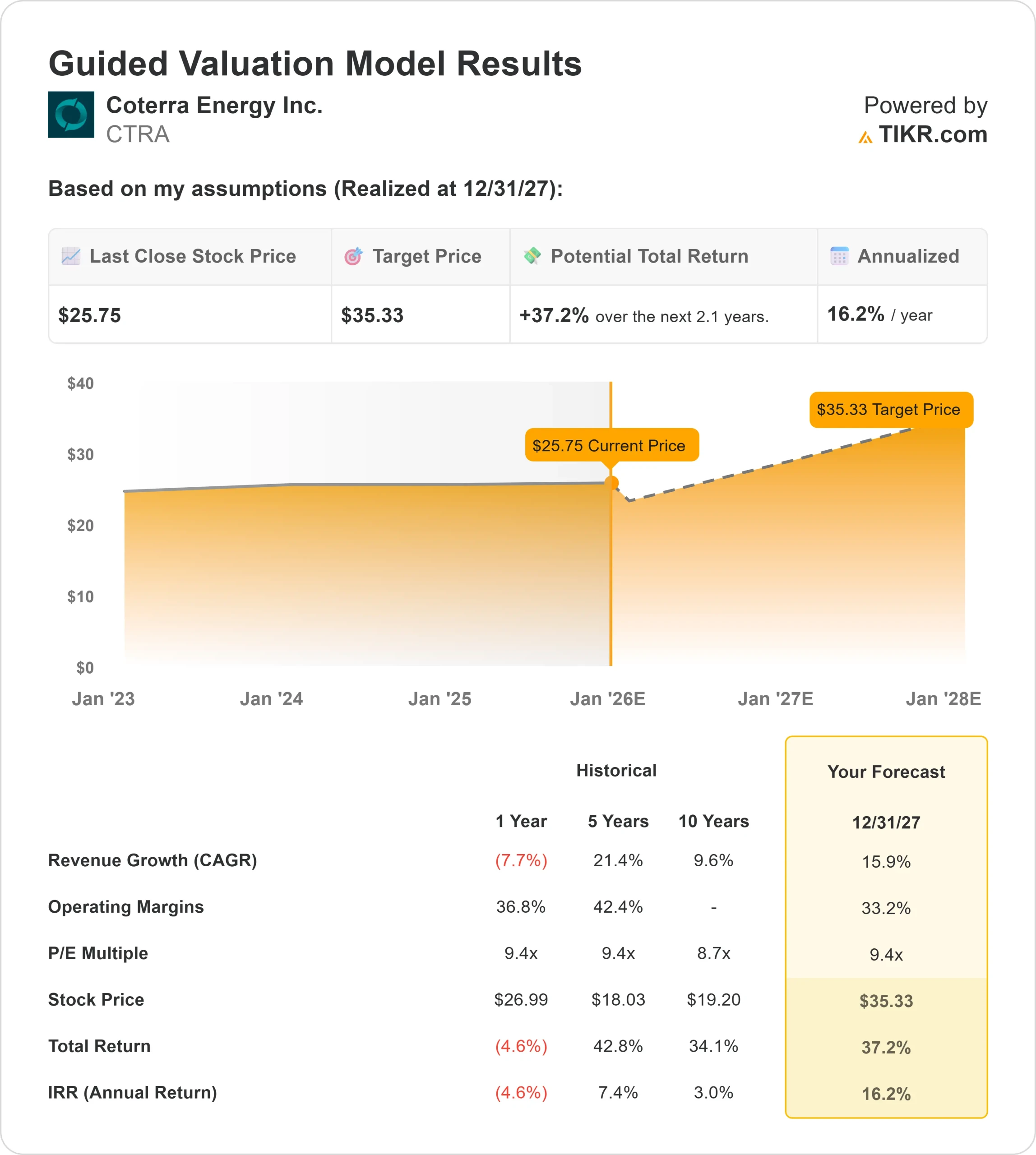

Coterra’s fundamentals appear solid and supported by steady operational performance. Analysts expect the company to deliver consistent growth through 2027 as production trends improve and margins remain healthy.

- Revenue growth forecast: 15.9%

- Operating margin forecast: 33.2%

- Forward P E used: 9.4x

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 9.4x forward P E suggests about $35/share by 12/31/27

- That implies around 37.2% upside, or roughly 16.2% annualized returns

These numbers indicate that Coterra can compound steadily without needing aggressive assumptions. The company’s strong margin profile and disciplined spending support a clear path to healthy earnings growth. For investors, Coterra looks like a high quality operator trading at a reasonable valuation, with potential upside driven by stable production and improving natural gas fundamentals.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Analysts are optimistic because Coterra continues to execute well, maintain strong cost control, and operate with financial flexibility. The company has demonstrated discipline across its operations, and stabilizing natural gas fundamentals help reinforce confidence in its earnings outlook. These strengths give investors reason to believe Coterra can compound value consistently.

Bear Case: Commodity Risk and Cyclical Pressure

Despite strong efficiency, Coterra remains exposed to natural gas price volatility. Shifts in supply and demand can quickly influence earnings, and weaker pricing environments have historically weighed on results. Broader macro risks, such as warmer weather patterns or elevated industry output, could also pressure margins.

For investors, the main concern is the cyclical nature of the business. Coterra is well managed, but not insulated from external drivers that can slow earnings momentum and limit valuation upside.

Outlook for 2027: What Coterra Could Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Coterra could trade near $35/share by 12/31/27, which represents about 37% total upside or approximately 16% annualized returns.

This outlook reflects a constructive path, though it already assumes steady margins and a stable commodity environment. To exceed these expectations, Coterra would need stronger pricing conditions or better than expected operational gains. Without those catalysts, investors can still expect a consistent, steady compounding path.

For investors, Coterra remains a high quality operator trading at a reasonable valuation. As long as operational discipline stays strong, the stock offers a clear case for long term value creation.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>