Key Stats for CMG Stock

- 52-Week Range: $29.75 to $58.42

- Current Price: $32.89

- Street Mean Target: ~$43.38

- TIKR Target Price (Mid): ~$61.41

- TIKR Annualized IRR (Mid): 14.5% per year

- LTM Gross Margin: 39.6%

- LTM EBIT Margin: 15.9%

Value your favorite stocks like CMG with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

Why the Market is Penalizing America’s Favorite Burrito

Chipotle Mexican Grill (CMG) has taken a brutal 35.2% hit over the past year, tumbling toward its 52-week low of $29.75. The market’s current obsession isn’t a lack of burritos sold; it’s a structural reset in valuation multiples after years of euphoric growth.

Investors are grappling with broader restaurant industry normalization and leadership transitions. Inflationary ticks in labor, beef, and freight have forced a temporary squeeze on restaurant-level operating margins.

However, under the hood, the company’s operational throughput remains remarkably resilient. Recent results showed a surprise return to positive transaction growth, driven by key menu innovations and an overhaul of their digital rewards engagement program.

See historical and forward estimates for CMG stock (It’s free!) >>>

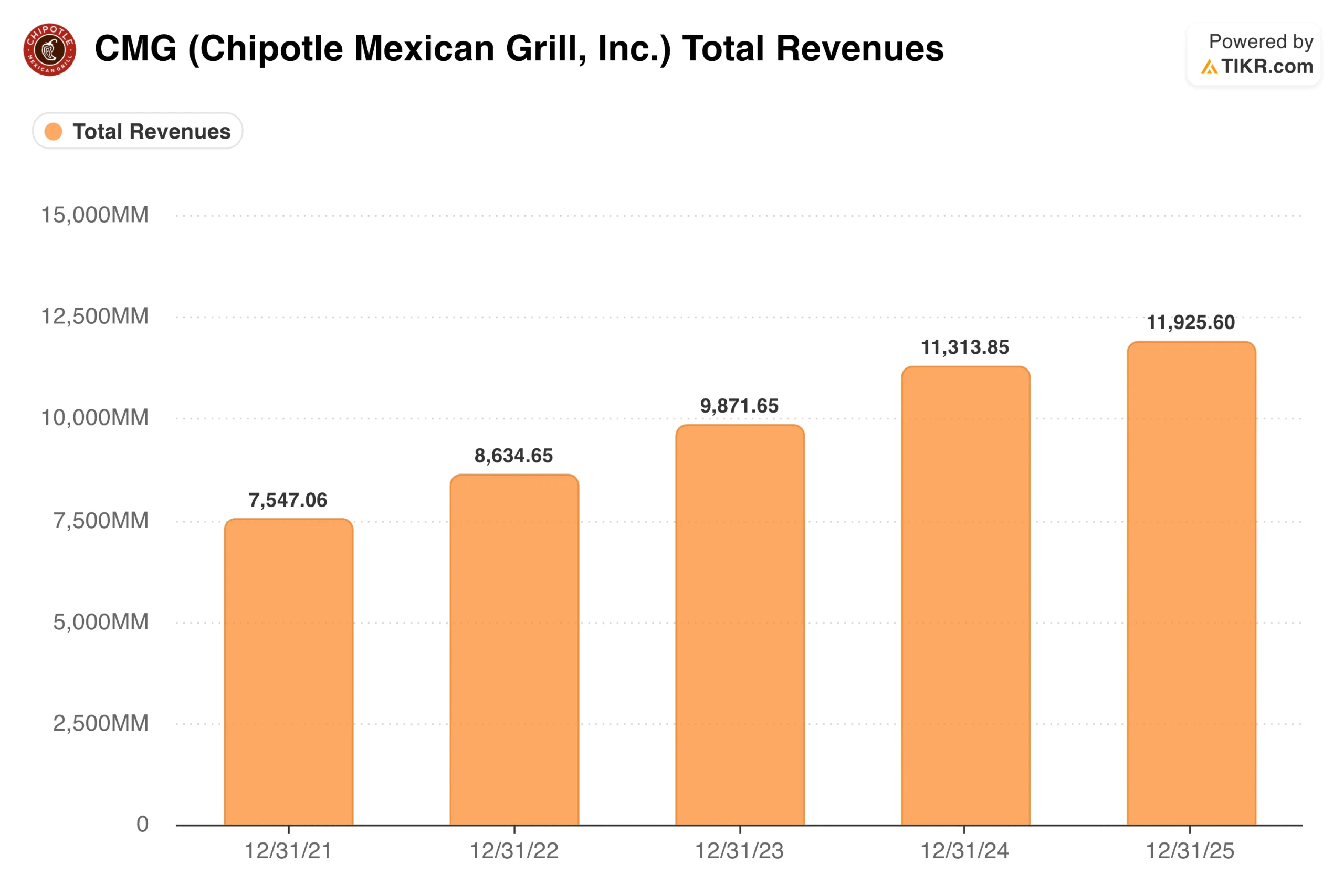

What the EPS Chart Shows About Chipotle’s Compounding Power

The market might be panicking about the stock price, but the normalized earnings per share (EPS) chart tells a completely different story. Chipotle’s underlying earnings power is expanding at a steady clip, unbothered by near-term stock volatility.

Adjusted EPS climbed from $0.51 in 2021 to $1.17 in 2025. This steady climb highlights excellent cost control, digital order efficiency, and massive pricing power that few peers can match.

Wall Street consensus estimates project that this compounding trajectory will shift into high gear. EPS is forecast to climb to $1.36 in 2027 and reach $2.17 by 2030.

This multi-year visibility is backed by Chipotle’s clear runway for new store openings and high-margin drive-thrus (“Chipotlanes”). To protect margins, management is deploying a high-efficiency equipment package, including automated dual-sided grills and high-capacity fryers, expected to reach 2,000 locations by the end of the year.

When incremental revenue flows through a highly optimized restaurant footprint, it translates directly into bottom-line earnings power.

See what analysts think about CMG stock right now (Free with TIKR) >>>

The Tailwinds: Pricing Power and Unit Compounding

Chipotle’s competitive moat is its phenomenal brand equity. The company boasts a high 24.8% Return on Invested Capital (ROIC), driven by stellar restaurant efficiency. Even during macro slowdowns, consumers treat Chipotle as an affordable luxury.

Traffic remains sticky, giving management a reliable lever to raise prices when labor or ingredient inflation ticks up. Furthermore, the ongoing system-wide rollout of automated kitchen equipment acts as a powerful margin lever, unlocking faster throughput per store, without adding structural overhead.

To maximize this efficiency, the company continues to aggressively expand its “Chipotlane” drive-thru formats, which historically yield structurally higher volumes and superior margins compared to traditional inline builds. This real estate strategy shifts the unit economic profile entirely, turning new store openings into highly predictable cash generation engines.

As these digital-first locations scale up, they reinforce a high-velocity capital-deployment cycle that allows Chipotle to self-fund its massive domestic expansion entirely from cash flow.

What the TIKR Model Implies at the Current Price

At $32.89, the TIKR valuation model suggests the market has severely over-discounted this high-quality business. The mid-case scenario targets a share price of $61.41 by the end of 2030, representing a potential total return of 86.7%, or a 14.5% annualized return.

The model assumes an organic revenue growth CAGR of 9.6% and a net income margin expanding slightly to 12.1% by 2030. Even the conservative low-case scenario implies a strong 10.0% annualized return, targeting $74.55.

Meanwhile, the high case reaches $129.90 at a stellar 17.3% annual return. This tight range proves that Chipotle doesn’t need to pull off a miracle to deliver market-beating returns from today’s compressed entry point.

The Risks: Execution Speed and Valuation Drag

No investment thesis is entirely risk-free. Chipotle lives and dies by its store execution; a slowdown in the rollout of new locations could push actual returns toward the lower end of the model. Furthermore, if a prolonged consumer spending crunch hits casual dining, multiple expansions could take longer to materialize.

Specifically, if cost inflation in key commodities like beef and avocados spikes while management holds off on menu hikes to protect market share, near-term restaurant-level operating margins will face immediate squeeze.

The stock’s trailing price-to-earnings (P/E) multiple of 30.14x also leaves very little room for operational missteps, as any perceived deceleration in growth will prompt instant institutional de-risking. If the broader market experiences a prolonged valuation compression, the stock could easily trade sideways regardless of stable financial metrics under the hood.

Is CMG Worth Buying at $33?

Chipotle is a premier consumer franchise trading at a temporary discount. While a 35% stock drop can feel alarming on paper, the fundamental data shows a compounding machine operating at peak health. The TIKR model reveals a highly favorable risk-reward asymmetric profile.

With management laser-focused on a long-term goal of hitting $4 million in average unit volumes and pushing restaurant-level margins toward 30%, this dip provides an exceptionally defensive entry point for investors looking to own an elite compounder.

Instead, you are buying a robust cash generator at a visible cyclical trough, with a margin of safety backed entirely by physical corporate expansion and compounding earnings power. For disciplined investors searching for institutional-quality market leaders trading at a rare discount, pulling the trigger at today’s compressed price is a highly compelling long-term allocation.

See analysts’ growth forecasts and price targets for CMG stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!