Key Stats for CVNA Stock

- 52-Week Range: $54.46 to $97.38

- Current Price: $68.28

- Street Mean Target: ~$92.92

- TIKR Target Price (Mid): ~$128.88

- TIKR Annualized IRR (Mid): 14.8% per year

- LTM Gross Margin: 20.1%

- LTM EBIT Margin: 9.2%

Value your favorite stocks like CVNA with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

Why the Market is Questioning the Used Car Vending Machine

Carvana (CVNA) has undergone one of the most volatile financial lifecycles in recent market history. After hovering near bankruptcy during the subprime car market unwind, the company executed a dramatic operational pivot away from unbacked volume chase and toward core unit profitability.

Despite a significant compression from its 52-week high, the business’s underlying economics are no longer fundamentally broken. The market’s current fixation has shifted from existential insolvency fears to whether Carvana can sustain its newfound efficiency gains in a normalizing auto inventory environment.

See the exact moment Wall Street upgrades a stock before the rest of the market piles in — track analyst rating changes in real time with TIKR for free →

How Carvana’s Unit Economics Flipped the Income Statement

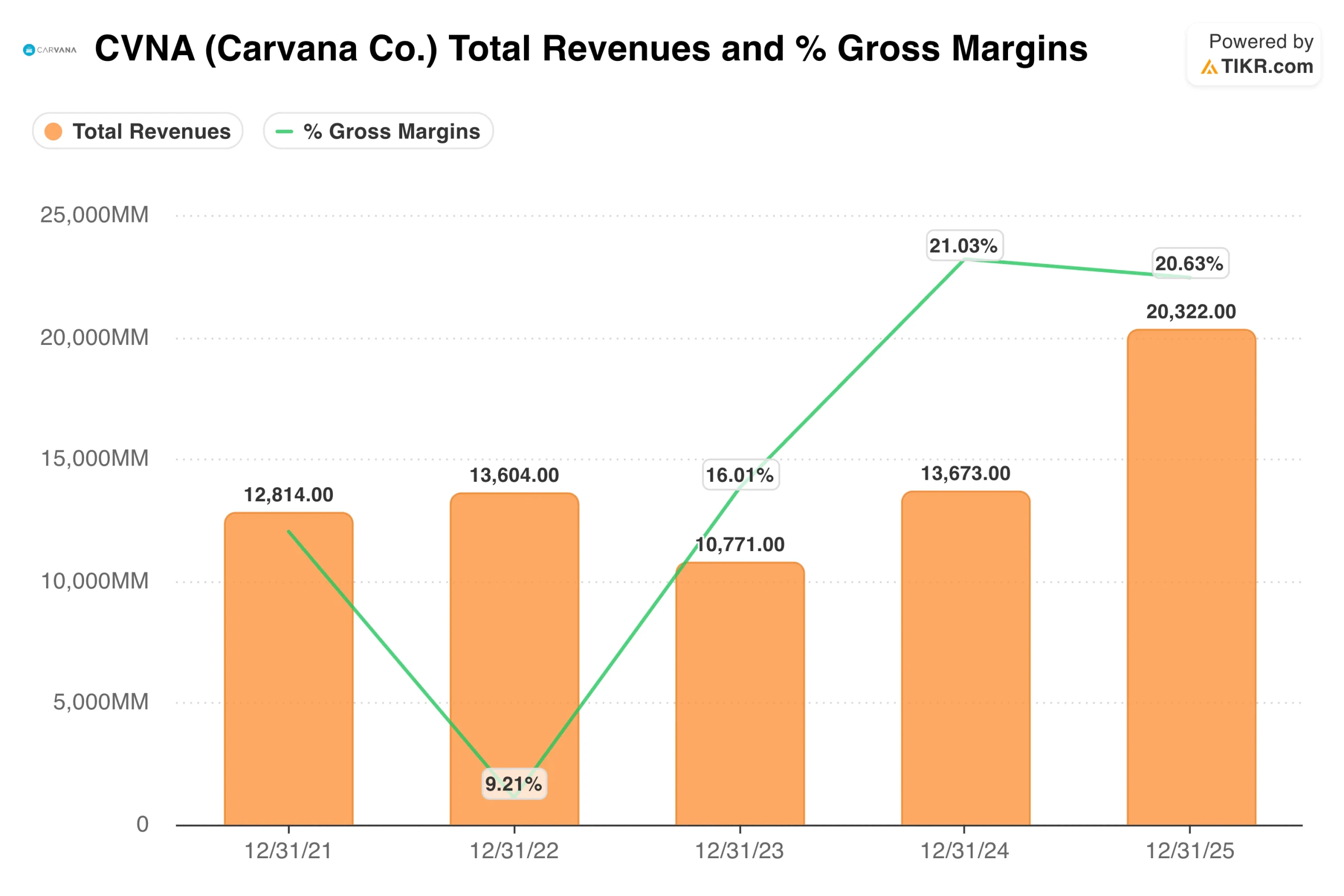

The gross margin expansion chart reveals a business that has radically rewritten its cost structure under the hood. In 2022, gross margins plummeted to a dangerous 9.21% as inventory write-downs and overhead crippled the operation.

However, by leveraging its proprietary vehicle reconditioning infrastructure and automating consumer logistics, management aggressively drove gross margins up to 21.03% in 2024 and maintained a stellar 20.63% into late 2025.

This systemic recovery directly unlocked massive fixed-cost operating leverage farther down the financial model. The company transitioned from a devastating net loss of $1,587 million and a negative operating margin in 2022 to a robust net income of $1,407 million and a 9.27% operating margin by 2025.

Once the physical distribution network and vending machine towers are fully built out, the corporate infrastructure requires minimal capital expenditures for maintenance, converting vehicle volume directly into clean operational cash flow.

What the TIKR Model Implies at $68

At its current price of $68.28, the TIKR valuation model highlights a pronounced mispricing asymmetry that favors long-term equity holders. The mid-case scenario targets a fair value share price of $128.88 by December 2030, offering an attractive 88.8% potential total return, or a 14.8% annualized IRR.

The baseline forecast assumes a conservative revenue CAGR of 15.9% and long-term net income margins steadying at 7.2%. Crucially, the low-case protection case targets a stock price of $136.94 over the full ten-year model horizon, delivering a resilient 8.4% annual return.

For a highly agile technology platform, this tight valuation band provides an extraordinary margin of safety against macro disruption.

See exactly how Carvana stock’s analyst price targets have moved over the past 12 months, and track every rating change as it happens, with TIKR for free →

The Tailwinds: Logistic Monopolies and Financing Flywheels

Carvana’s persistent competitive advantage lies in its vertically integrated national logistics network. By avoiding the steep regional franchise overhead costs that weigh down legacy competitors, the company preserves a lean, centralized inventory pool that can adapt dynamically to consumer demand shifts.

Furthermore, their proprietary auto loan securitization engine generates exceptionally high-margin transaction revenue upon every vehicle delivery.

As digital adoption accelerates among younger car buyers, Carvana continues to seize domestic market share from highly fragmented mom-and-pop dealerships. This structural migration allows the brand to expand its aggregate unit volumes without relying on aggressive retail promotional discounts.

This ongoing optimization positions the franchise to self-fund its inventory scaling entirely out of structural operational cash generation.

The Risks: Credit Market Swings and Volume Volatility

No aggressive retail turnaround thesis comes completely without operational risk. Carvana remains structurally sensitive to interest rate fluctuations; a prolonged spike in auto loan borrowing costs would immediately pressure consumer affordability and depress overall unit transaction volumes.

Additionally, if competitive pressure intensifies from traditional mega-dealers aggressively subsidizing their own digital platforms, Carvana could see its customer acquisition costs expand uncomfortably.

The company’s historical three-year net margin average of negative 15.0% serves as a stark reminder of how fast negative operating leverage can damage the income statement if car volumes contract.

Flawless regional execution across their reconditioning centers remains absolutely mandatory to hit the upper parameters of the model. Any material deceleration in vehicle sales will prompt immediate institutional de-risking, given the stock’s forward P/E multiple.

Is CVNA Worth Buying at $68?

Carvana is no longer the speculative, debt-laden gamble that polarized Wall Street short-sellers for years. The raw financial metrics reveal an optimized, institutional-quality e-commerce powerhouse that has successfully crossed over the operational leverage hump.

The TIKR terminal data indicate that the market is still discounting the durability of management’s structural margin improvements.

Instead, you are buying a robust cash generator at a visible cyclical trough where the margin of safety is backed entirely by physical corporate expansion and compounding earnings power.

For disciplined investors searching for institutional-quality market leaders trading at a rare discount, pulling the trigger at today’s compressed price is a highly compelling long-term allocation.

See analysts’ growth forecasts and price targets for DELL stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!