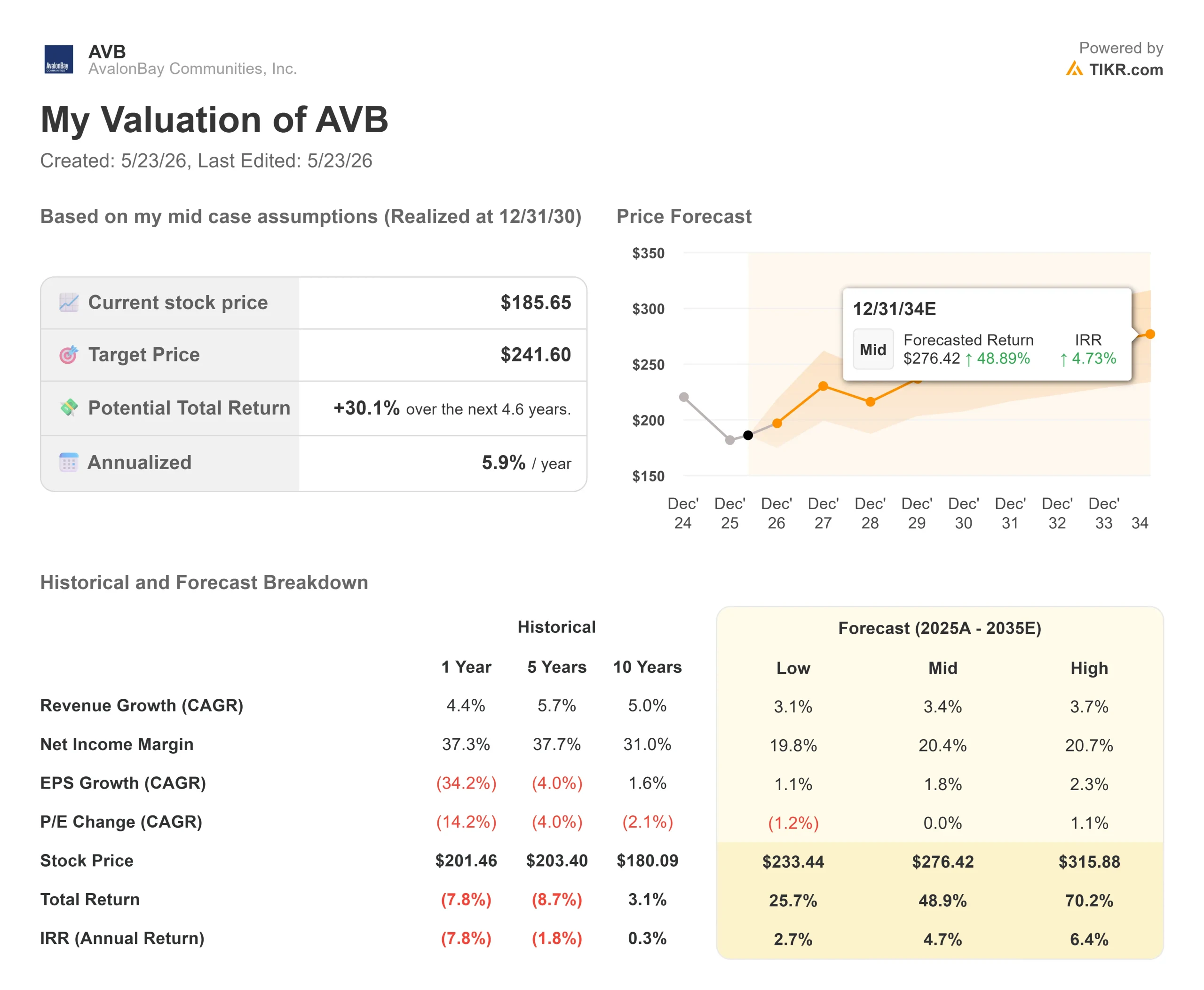

Key Stats for AvalonBay Communities Stock

- Current Price: $185.65

- Target Price (Mid): ~$242

- Street Target: ~$195

- Potential Total Return: ~30%

- Annualized IRR: ~6% / year

- Earnings Reaction: +5.29%

- Max Drawdown: 22.99%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The Merger That Redrew the Apartment Map

AvalonBay Communities (AVB) just became a different company. On May 21, 2026, AvalonBay and Equity Residential (EQR) announced a merger of equals that creates the largest apartment landlord in U.S. history, with a combined enterprise value of approximately $69 billion, an equity market cap of roughly $52 billion, and more than 180,000 rental apartments across the country’s highest-barrier coastal markets.

The market shrugged. AVB fell 1.5% on announcement day before recovering to $185.65. The Street target sits at around $195, and 15 of the 20 analysts tracked by TIKR hold a neutral stance (3 Buys, 2 Outperforms, 15 Holds). The consensus treats this as a mature-sector consolidation play.

That reading may miss what management actually committed to on the joint investor call. The thesis is not primarily about cost savings. It is about whether a platform of this scale can produce a structurally different growth rate than either company could deliver alone, and whether that possibility is priced into AVB at $185.65.

What Management Said on the Call

The joint call was hosted by AvalonBay CEO Benjamin Schall and outgoing Equity Residential CEO Mark Parrell. Schall described the deal’s core logic as a “flywheel”: operational scale drives margin improvement, better margins improve development returns, stronger returns lower the cost of capital, and a lower cost of capital enables more growth. Each rotation compounds the next.

The headline numbers are real. The deal targets $175 million in gross operating synergies, reduced to $125 million net after California property tax reassessments triggered by the transaction. Management expects more than 85% of those savings to be in place by the end of 2027 and the full amount within 18 months of closing.

But Schall was clear that the synergy figure is a starting point. “The ability here to create a truly differentiated model where we can lean into a set of capabilities to deliver a structurally higher level of growth,” he said, “that’s beyond what either of our companies can deliver today.”

Scale as a Real Operating Advantage

Schall used Northern California to illustrate what market density actually changes. The combined company will hold 84 communities and approximately 24,000 homes in that region alone. At that level of concentration, regional managers carry wider portfolios with better data visibility, teams can specialize in single functions across dozens of properties, and each new asset added to the platform arrives at near-zero marginal overhead cost.

With 95% market overlap between the two companies’ portfolios, every efficiency identified in one region applies across nearly the entire combined footprint. That is how management argues operating profit margins, which have been stuck around 70% at both companies for years, can finally move higher. Parrell attributed the stagnation mainly to soft revenue growth, not poor cost discipline. On the revenue side, the combined company plans to layer in ancillary services, including bulk internet, resident insurance, and furnished housing programs already piloted by AvalonBay.

The AI and Data Angle

One of the most substantive parts of the call was the companies’ joint investment in EliseAI, an AI platform that handles conversational interactions with prospective residents across the lease inquiry and customer journey. Parrell noted that it is expensive to build, it will be sold to the broader industry, and the combined company will not own it outright. The point: Newco will have the financial scale to fund proprietary AI tools that neither company could justify independently.

The combined platform will hold data from 4 million lease transactions, 9 million service requests, and over 60 million pieces of customer feedback, per Schall’s prepared remarks referencing the investor presentation. The practical targets are demand forecasting, renewal and concession optimization, and predictive maintenance decisions. None of this shows up in the $125 million synergy figure.

See historical and forward estimates for AvalonBay Communities stock (It’s free!) >>>

The Development Engine

The combined company enters with a $4.4 billion development pipeline representing approximately 10,800 homes across 32 communities, with initial stabilized yields projected above 6%. Beyond active construction, the entity holds roughly $4.2 billion in development rights covering approximately 9,800 additional homes. More than half of the future pipeline includes affordable or mixed-income components.

Schall’s stated baseline ambition on the call: double the development activity that both companies were running independently. A stronger operating model means more projects clear the return threshold, which means more external growth, which feeds the flywheel.

AvalonBay’s standalone track record supports the ambition. According to its investor relations materials, Q1 2026 development starts totaled nearly $190 million, with full-year 2026 starts targeting $800 million at projected stabilized yields of 6.5% to 7%.

What the Market Is Skeptical About

Three concerns are driving the cautious analyst stance.

Execution risk. The deal still requires shareholder votes from both companies, with closing expected in the second half of 2026. The $50 million Proposition 13 property tax reassessment, which is almost entirely in California, is a good-faith estimate subject to negotiation with assessors over 18 to 24 months per Parrell’s comments on the call. Synergies are projections until they appear in reported results.

Near-term revenue headwinds. AVB’s same-store revenue grew 1.6% in Q1 2026. The Mid-Atlantic region is absorbing ongoing job losses. Concessions remain elevated in Denver. The margin expansion thesis needs a revenue environment that is not fully cooperating yet.

Valuation multiples. AVB trades at 18.70x NTM EV/EBITDA and 16.27x NTM P/FFO as of May 22. At those levels, with a complex integration ahead, the Street’s ~$195 consensus target reflects limited appetite to pay a premium for a thesis that still needs to prove itself.

See how AvalonBay Communities performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $185.65

- Target Price (Mid): ~$242

- Potential Total Return: ~30%

- Annualized IRR: ~6% / year

See analysts’ growth forecasts and price targets for AvalonBay Communities stock (It’s free!) >>>

The TIKR mid-case model uses a 3.4% revenue compound annual growth rate through the forecast period, driven by two factors: same-store NOI growth as operating scale gradually improves margins, and incremental revenue from the development pipeline as new communities deliver at stabilized yields above 6%. Net income margins are forecast to stabilize around 20% in the mid case. The primary risk is integration disruption: transition costs or management distraction could compress margins in the near term and cause the revenue CAGR to undershoot.

The mid-case implies roughly 30% total return to 12/31/30, or about 6% annualized. That is a modest return on its own. The upside case is that the flywheel accelerates ahead of the model’s conservative assumptions. The downside case is that integration friction drags on long enough that the Street’s $195 target proves more accurate for the next 12 to 18 months.

The TIKR model is built on AVB as a standalone entity. The merger’s potential earnings uplift is not yet embedded in consensus estimates. That gap is either an opportunity or a mirage, depending entirely on how the combined company executes over the next 18 months.

Conclusion

The AVB thesis will be tested by a clear, measurable event: does the combined company deliver its $125 million in net synergies on the 18-month timeline management publicly committed to on May 21?

The first post-merger quarterly earnings call, expected after the deal closes in the second half of 2026, will be the first real signal. Watch for synergy progress, same-store NOI margin direction, and whether development activity is scaling toward the doubled pace Schall described. AVB’s last standalone quarterly update is estimated for July 29, 2026, which sets the baseline.

If synergies track to plan and development is accelerating, the case for AVB approaching the TIKR mid-case target of around $242 by 12/31/30 strengthens. If the integration shows early friction, the ~$195 Street consensus suggests the market will not wait.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in AvalonBay Communities?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AvalonBay Communities, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AvalonBay Communities alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze AvalonBay Communities on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!