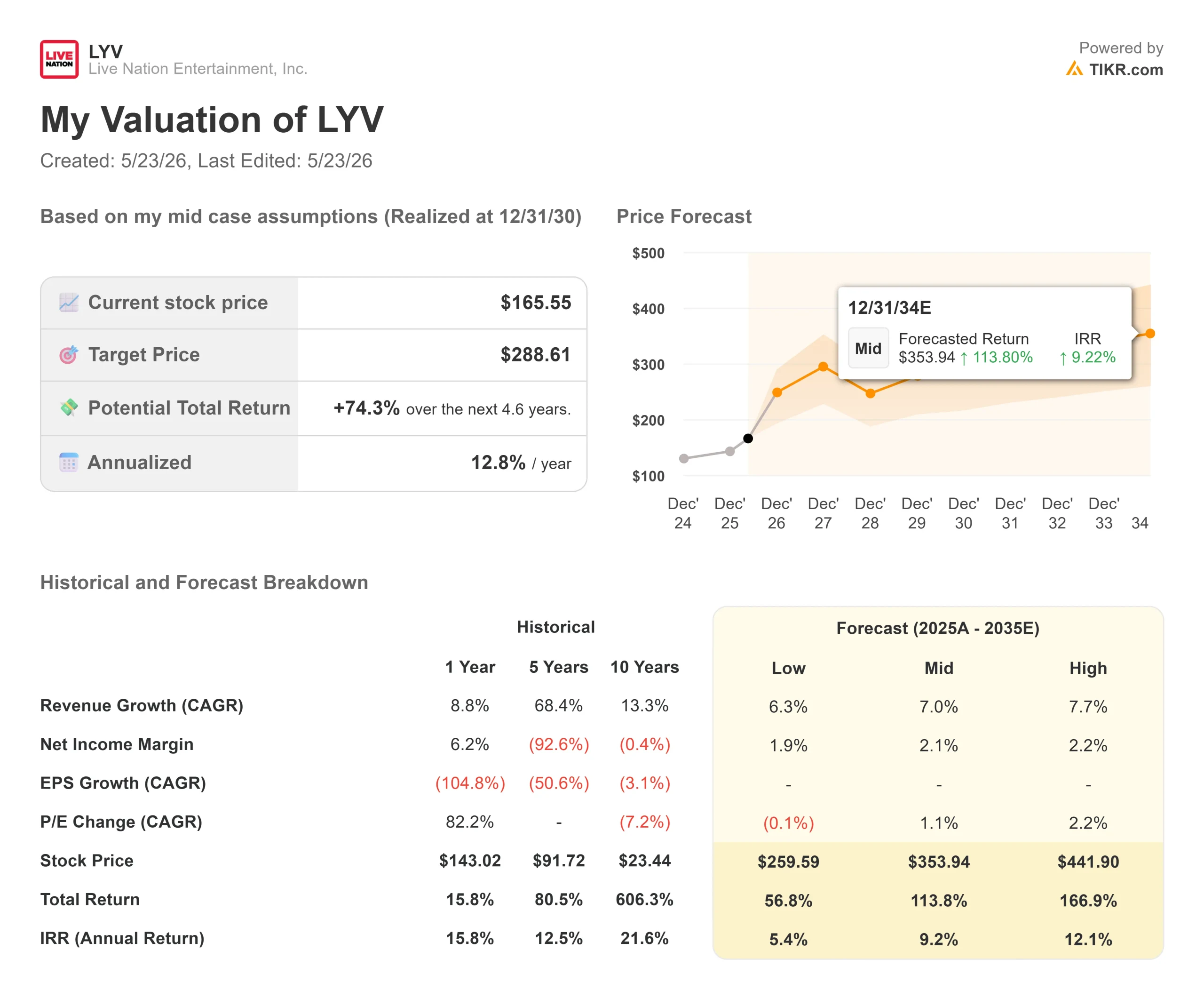

Key Stats for Live Nation Stock

- Current Price: $165.55

- Target Price (Mid): ~$289

- Street Target: ~$185

- Potential Total Return: ~74%

- Annualized IRR: ~13% / year

- Q1 2026 Earnings Reaction: +6.71% (May 5, 2026)

- Max Drawdown: 27.84% (11/24/25)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

The 2026 narrative on Live Nation Entertainment (LYV) has been shaped mostly by courtrooms. A federal jury found Ticketmaster liable on all antitrust counts in April. A $450 million legal accrual wiped out operating income in Q1. Analysts are split between those who see a structurally impaired business and those who see a legal cloud hanging over one of the most entrenched franchises in live entertainment.

Joe Berchtold, President and CFO of Live Nation, appeared at the J.P. Morgan 54th Annual Global Technology, Media and Communications Conference on May 20 with a different set of numbers. The company had already sold 119 million tickets for 2026 shows as of that date, up from the 107 million disclosed at Q1 earnings three weeks prior. That means 11.5 million tickets moved in three weeks, more than the same period last year. The question is whether the legal overhang obscures that long enough to give investors a real entry point.

What the CFO Said That the Headlines Missed

Berchtold was direct about what he called “anecdotal and misleading” press coverage on concert demand. His data at JPMorgan backs that up.

Ticket sales are tracking double digits ahead of last year across stadiums, arenas, and amphitheaters. Cancellation rates remain in the historical 1% to 2% range. With the summer amphitheater season roughly 5% complete at the time of the conference, on-site per-capita spending was already running above last year, with no signs of consumer trade-down.

The average U.S. get-in price sits at $34 to $35, up roughly 18% from 2019, while general inflation ran approximately 30% over the same period. Only 2% of U.S. tickets exceed $500, and about 60% are priced below $100. The affordability argument holds when you look at the actual price distribution rather than the headline anecdotes.

One forward indicator Berchtold highlighted is deferred revenue, which is ticket proceeds recognized when the show is performed rather than when the ticket is sold. That figure grew in the high-20s percent range in Q1 2026, representing over $5 billion in gross transaction value (the total dollar amount of tickets processed on the platform). It does not appear in the headline quarterly revenue, but it signals what is coming.

See historical and forward estimates for Live Nation stock (It’s free!) >>>

The Legal Overhang Is Real, But the Remedies Are Already Defined

The antitrust story is the central debate for any LYV position, and the facts are more defined than the market appears to be pricing in.

In March 2026, the DOJ settled with Live Nation mid-trial, stopping short of a forced Ticketmaster breakup. Under the deal, Live Nation exits 13 exclusive amphitheater booking agreements, opens Ticketmaster’s infrastructure to competing platforms, caps service fees at owned venues at 15%, and funds a $280 million pool for participating states.

Thirty-three state attorneys general rejected that deal and pressed forward. On April 15, a federal jury found Live Nation liable on all counts, sending LYV down more than 6% on the day. The remedy phase, where Judge Arun Subramanian will decide whether structural relief, including a possible Ticketmaster breakup, is warranted, is still ahead. Legal analysts at Crowell & Moring note that with pending motions and an all-but-certain appeal, final resolution is unlikely before 2028. Live Nation has said the verdict “is not the last word on this matter.”

At JPMorgan, Berchtold addressed these changes without apparent concern. On nonexclusive ticketing contracts, he said the company is “fine with that,” arguing most venues will still choose Ticketmaster because it is the superior product. On opening owned amphitheaters to third-party promoters, he pointed out that per-capita on-site spending has grown from roughly $16 to $46 over the past decade. Opening the buildings to outside promoters may trim some promotion revenue, but it adds high-margin ancillary revenue from operations. He called it a net positive.

The Q1 earnings reaction already shows investors separating the legal story from the operating one. Despite a $389.1 million net loss driven almost entirely by the litigation accrual, LYV jumped 6.71% on May 5 after reporting $3.79 billion in revenue, up 12% year over year, and beating estimates.

The International Runway Berchtold Keeps Coming Back To

Every topic at JPMorgan circled back to international. Berchtold was specific at every turn.

At concerts, he contrasted the U.S. and U.K. (the two most penetrated markets) with Western Europe, Latin America, and Asia, citing 2x to 4x growth potential in markets where a hyperlocal strategy is still early. In Latin America, OCESA (Live Nation’s Mexico-and Colombia-based promoter) anchors the expansion. Berchtold used Mexico as a proof of concept: one touring cycle produced stadium shows across 10 cities, and a new venue is now under development in Guadalajara.

In Japan, Berchtold flagged the HIP (Hayashi International Promotions) acquisition and a new Ticketmaster president who has committed to selling tickets in Japan within one year, replacing the typical multi-year rollout. The Venue Nation pipeline (Live Nation’s dedicated division for building and operating large-scale venues) stands at roughly 20 venues in construction or fully permitted, with about 10 at the large arena or amphitheater scale. Of the top 75 cities outside the U.S., Berchtold said 47 either lack a modern arena or are underpenetrated for their market size. That gap is the construction runway.

On the competitive landscape, CTS Eventim (EVD), Live Nation’s closest European peer, trades at 6.63x NTM EV/EBITDA on a market cap of approximately €5.4 billion. Live Nation trades at 15.39x NTM EV/EBITDA on a market cap of $38.5 billion. That premium reflects global scale, the Ticketmaster platform, and a sponsorship network that Eventim does not replicate. Whether it is sustainable depends on the legal outcome and whether international markets deliver what Berchtold is projecting.

See how Live Nation performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $165.55

- Target Price (Mid): ~$289

- Potential Total Return: ~74%

- Annualized IRR: ~13% / year

See analysts’ growth forecasts and price targets for Live Nation stock (It’s free!) >>>

The TIKR mid-case model uses a revenue CAGR of around 7%. Consensus estimates on the TIKR project approximately $39 billion in revenue by 2030. Two drivers underpin that growth rate: international concert and venue expansion across Latin America and Asia, and Ticketmaster’s rollout into new markets where incremental ticket volume flows through largely fixed platform infrastructure.

The margin driver is Sponsorship and Advertising, which generated $1.33 billion in revenue in 2025, up from $1.20 billion in 2024, and is running 85% to 90% sold for 2026 per Berchtold’s comments at JPMorgan. Venue expansion compounds this segment directly, as each new arena or amphitheater unlocks naming rights and in-venue sponsorship assets.

The primary risk is structural. The ticketing segment contributed $1.13 billion in operating income in 2025, at margins that the concert and venue segments do not yet match. If Judge Subramanian orders a Ticketmaster divestiture, the integrated model underlying this thesis changes materially, earnings expectations reset, and the EV/EBITDA multiple compresses simultaneously. If the remedy stays limited to the behavioral changes already in the DOJ settlement, a business with consensus free cash flow estimates approaching $2.7 billion by 2030 looks meaningfully undervalued at today’s multiple.

Conclusion

The event that will confirm or break this thesis is Judge Subramanian’s remedy ruling. A remedy confined to the behavioral changes already in the DOJ settlement leaves the investment case intact. A breakup order, even if ultimately overturned on appeal, resets the multiple and introduces years of uncertainty around Ticketmaster’s standalone earnings.

While that plays out, watch Q3 2026 earnings, the peak of the summer concert season. If on-site per-cap spending holds above last year and deferred revenue maintains its double-digit pace, the gap between the legal narrative and the operational reality becomes much harder to justify.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Live Nation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Live Nation, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Live Nation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Live Nation on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!