Key Takeaways:

- Turnaround Focus: Nike is resetting its strategy after shares have fallen 13% this year, prioritizing wholesale rebuilds, product innovation, and brand momentum recovery.

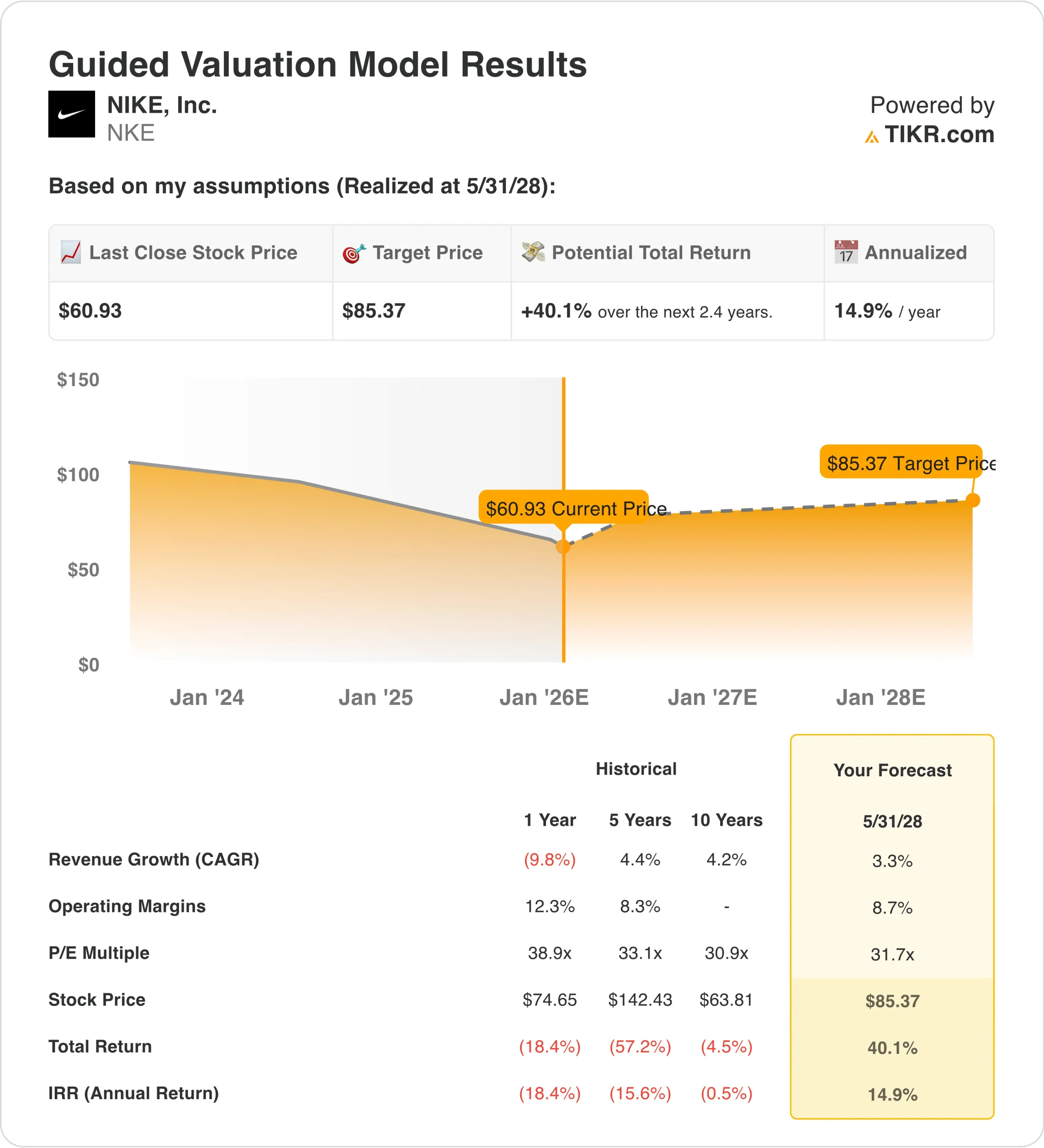

- Price Projection: Based on normalized growth and margin recovery, Nike stock could reach $85 by May 2028.

- Potential Gains: This target implies a 40% total return from the current $61 share price.

- Annual Return: The model projects roughly 15% annualized returns over the next 2 years as execution improves.

Nike (NKE) is one of the world’s largest athletic apparel and footwear companies, generating over $46.5 billion in trailing twelve-month revenue through its global brand portfolio spanning footwear, apparel, and equipment.

Investor attention increased after Apple (AAPL) CEO Tim Cook purchased $3 million in Nike shares, signaling confidence in the company’s leadership-led reset under CEO Elliott Hill.

Revenue declined from $51 billion to $46 billion over the past year as inventory reductions, softer China demand, and fewer promotions weighed on near-term sales.

Operating margins fell below 7% as pricing pressure and higher costs reduced profitability, even as Nike generated $6 billion in free cash flow supporting balance sheet flexibility.

With a market value over $90 billion, Nike is repositioning toward performance categories and wholesale partnerships to stabilize revenue and rebuild earnings power.

Despite improving execution, the stock trades near 32x earnings, raising the question of whether current valuation fully reflects the pace of margin normalization ahead.

What the Model Says for Nike Stock

We evaluated Nike based on a reset toward steady execution, assuming revenue growth of 3% as wholesale relationships and product cycles normalize.

The model assumes operating margins recover to 9% with a stable 32x exit multiple, reflecting gradual earnings repair rather than peak-cycle expansion.

Under these assumptions, Nike could reach $85 by May 2028, implying a 40% total return or 15% annually.

Model how Nike’s margins and growth outlook could affect fair value through 2028 for free →

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Nike stock:

1. Revenue Growth: 3.3%

Nike’s revenue declined 9.8% YoY in the most recent year as China demand softened and inventory normalization weighed on wholesale and direct channels.

Over the past decade, Nike’s revenue growth averaged ~4–5% outside pandemic distortions, reflecting global brand scale but limited unit expansion.

Near-term execution is constrained by reduced promotional activity and deliberate pullback from lower-return lifestyle categories under the “Win Now” strategy.

Product reinvestment in performance footwear and running supports stabilization, but does not yet justify a sharp re-acceleration.

China revenue remains volatile, limiting upside visibility despite global recovery signals.

In line with analyst consensus projections, a 3.3% growth outlook balances brand resilience against category maturity and a cautious wholesale recovery.

2. Operating Margins: 8.7%

Nike’s operating margin declined to ~8.0% LTM, down sharply from mid-teens levels seen earlier in the cycle.

Historically, margins ranged between 12–15% during periods of strong product cycles and favorable channel mix.

Recent margin pressure reflects higher markdowns, weaker China profitability, and reinvestment in innovation and marketing.

Management actions are focused on cost discipline and channel reset, but benefits are gradual rather than immediate.

Inventory normalization reduces risk, yet limits near-term operating leverage.

Based on consensus market estimates, an 8.7% operating margin reflects recovery from trough conditions while remaining below peak-cycle profitability.

3. Exit P/E Multiple: 31.7x

Nike currently trades near 31–32× normalized earnings, despite earnings compression and slowing revenue momentum.

Over the last decade, Nike’s P/E averaged ~30–34×, supported by brand strength and global consumer reach.

Investor confidence remains cautious due to execution risk, but insider buying signals belief in long-term recovery.

Sustained valuation requires stabilization in China and proof that innovation spending can rebuild margins.

According to aggregated analyst estimates, a 31.7× exit multiple sits within Nike’s long-term trading range while acknowledging limited scope for near-term re-rating.

What Happens If Things Go Better or Worse?

Nike’s outcomes hinge on whether its leadership reset restores margins, stabilizes wholesale channels, and reaccelerates core footwear demand. Here is how Nike stock might look in different scenarios through 2028:

- Low Case: f revenue growth stays near 5%, net income margins remain around 7% due to ongoing promotions and cautious wholesale ordering, and valuation softens as earnings recovery disappoints → 10% annual return.

- Mid Case: If revenue grows around 5%, margins recover toward 8% as inventory clears and pricing discipline improves, and valuation remains stable as profitability normalizes → 15% annual return.

- High Case: If revenue growth improves toward 6%, margins recover into 9% as product innovation gains traction, and valuation expands modestly on stronger earnings momentum → 20% annual return.

Nike’s return profile depends more on margin repair than aggressive sales growth, with earnings recovery setting the pace for shareholder returns.

At the base case, the $85 target appears achievable if wholesale rebuilds and product execution lift margins back toward normalized levels.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!