Key Stats for Alphabet Stock

- Current Price: $370.92

- Target Price (Mid): ~$645 by 12/31/2030

- Street Target: ~$432

- Potential Total Return: ~74% over the next 4.5 years

- Annualized IRR: ~13% / year

- Max Drawdown: 20.42% on 3/30/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Alphabet (GOOGL) closed at $370.92 on July 15, and the most famous investor alive spent part of that morning on television taking personal credit for owning it. Berkshire Hathaway’s position is now north of $31 billion. That is the kind of headline that usually ends an argument. It didn’t, because Warren Buffett used the same interview to name the exact problem that has kept this stock rangebound all year, and he did not soften it.

The stock rose 3.17% that session, though the tape is not the story here. What Buffett actually said is. He bought the franchise. He also said he likes at least four or five other Berkshire businesses better, and he flagged the AI spending as the open question facing Google and everyone competing with it. Six days from now, the company reports and gets a chance to answer him.

Buffett Named the Bear Case Out Loud, Then Bought Anyway

The news was narrow. Speaking with CNBC’s Becky Quick on Wednesday, Buffett settled who was behind Berkshire’s Alphabet position, an open question because Greg Abel took over as CEO in January. “I initiated it,” Buffett said, adding that he and Abel approve each other’s decisions but that “he is the decider.” Berkshire first disclosed the stake in the third quarter of 2025 and has expanded it since, including a $10 billion private placement earlier this year priced at $351.81 per Class A share. Worth noting for anyone tempted to buy alongside him: that entry sits about 5% below where the stock closed on Wednesday, and the open-market accumulation began when shares were far cheaper still.

Investors read the confirmation as a durability signal, because Berkshire avoided technology almost entirely until Apple.

What matters is what he said next. “The real question with Google and all of its competitors now, because they’re all laying out hundreds of billions, and that’s real money,” Buffett said. “That’s the game they’re playing now. They weren’t playing that game with computer software.” He also said plainly that he doesn’t like Alphabet as well as at least four or five other businesses Berkshire owns. That is not an endorsement of the AI capex cycle. That is a man buying a franchise while telling you it has become capital-intensive in a way it never used to be.

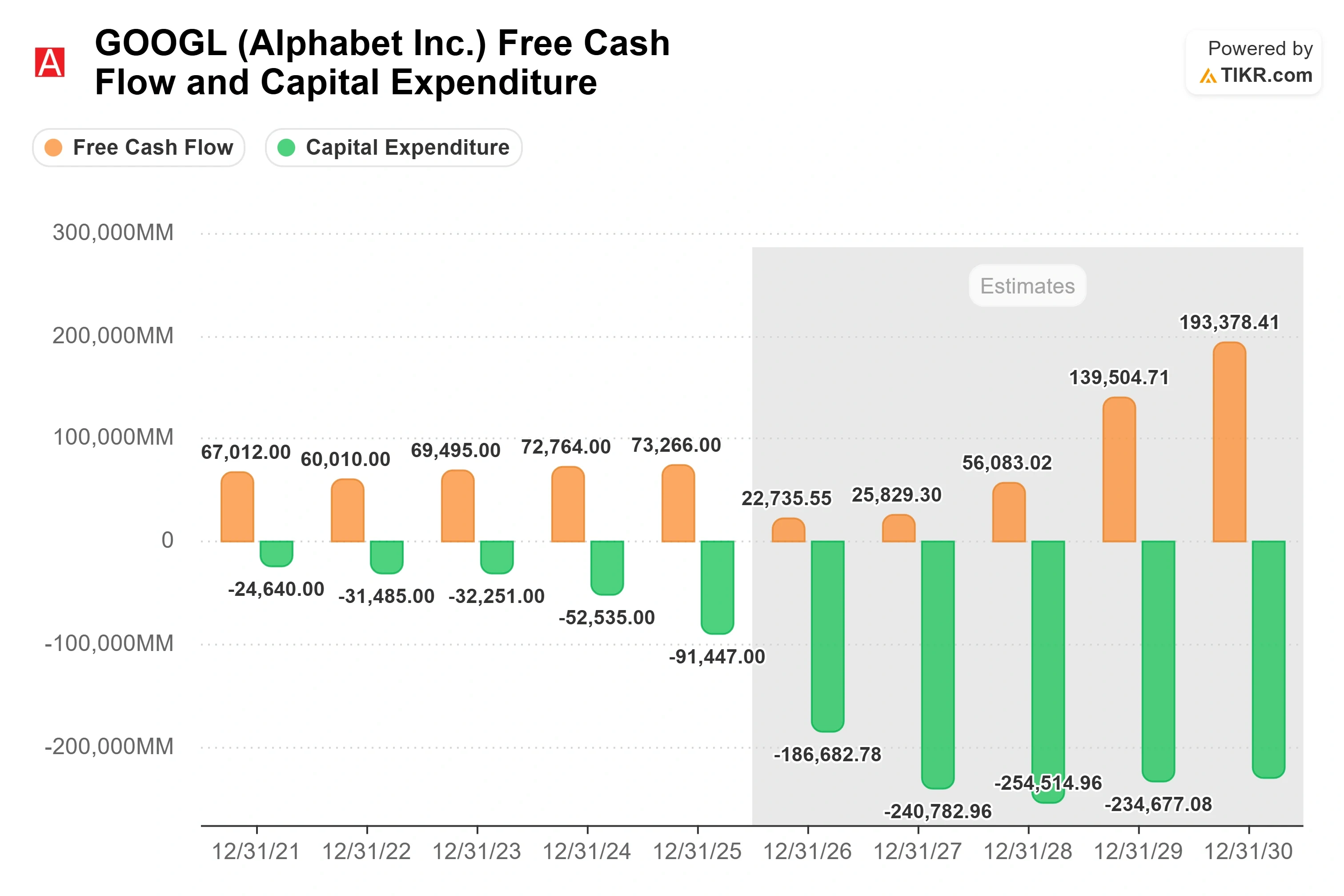

The numbers carry his point. Capital expenditure hit $35,674 million in the March quarter alone. TIKR’s estimates show free cash flow, the cash left after a company funds its operations and capital spending, compressing to around $23 billion in 2026 from $73,266 million in 2025, a drop of roughly 69%, before recovering toward around $56 billion in 2028 and around $140 billion in 2029 as the buildout cycles through depreciation. Free cash flow margin falls from 18.2% to under 5% in a single year. That is the price of the buildout, stated exactly.

See historical and forward estimates for Alphabet stock (It’s free!) >>>

Management Says the Constraint Is Supply, Not Demand

Alphabet’s answer is that it is not spending on speculation. It is spending because it cannot serve the customers it already has. CEO Sundar Pichai put it directly on the company’s June 3 special call: the company is “experiencing strong demand for our AI solutions and services from enterprises and consumers at levels that are meaningfully exceeding our available supply.” That framing flips the risk. A company overbuilding into hoped-for demand has made a capital allocation error. A company building into demand it is currently turning away has a revenue timing problem, which is a far better problem to own.

The evidence sits in Cloud. CFO Anat Ashkenazi said the segment delivered a record $20 billion in first-quarter revenue while expanding margins to 33% and more than tripling operating income to almost $7 billion. Pichai put Cloud’s growth rate at 63% year over year. Backlog, meaning contracted revenue not yet recognized, nearly doubled sequentially to $462 billion, and Pichai told investors the company expects to recognize just over 50% of it as revenue over the next 24 months. Customers are committing for years, not buying capacity by the month.

The June 1 equity raise was funding exactly this, and Berkshire’s $10 billion was part of it. That sum is a small slice of a $180 billion to $190 billion annual budget, so his participation is a directional signal rather than a decisive one: Buffett appears to believe Alphabet earns a return on this spending and that most of the field will not. That reading is not confirmed until the returns arrive.

Where the money shows up first is in unit costs, and the direction there is encouraging. Pichai said the company reduced Gemini serving costs by 78% in 2025, and Ashkenazi said hardware and engineering breakthroughs since Gemini 3 have cut the cost of core AI responses by more than 30%. She also reported Google Services operating margin, or operating profit as a share of revenue, expanding to 45% from 42% a year ago, while Pichai noted Search revenue grew 19% with queries at an all-time high. The AI transition is not eating the ads business. So far, it is widening it.

See how Alphabet performs against its peers in TIKR (It’s free!) >>>

The Multiple Says the Market Already Believes Half of It

At $370.92, shares trade at 29.31x NTM P/E, meaning price divided by expected earnings over the next twelve months, and 18.54x NTM EV/EBITDA. Against its own history that is elevated: NTM P/E sat at 19.15x a year ago, and the stock has climbed back from a 20.42% drawdown that bottomed on March 30. The Street’s mean target sits near $432, only about 16% above the current price, which tells you consensus has already banked most of the recovery. The market has paid for the Cloud acceleration. It has not paid for the second act, which is the spending converting into cash rather than into depreciation.

Peer data sharpens the picture without settling it. In TIKR’s Interactive Media and Services group, Reddit (RDDT) trades at 26.74x NTM P/E and 23.04x NTM EV/EBITDA, and Pinterest (PINS) trades at 12.56x and 9.19x. Alphabet carries a premium to the group’s 10.28x median P/E, and it has earned one, because neither peer runs a $462 billion backlog or a 60.4% gross margin on $422,498 million of trailing revenue. But the comparison is thin. Neither Reddit nor Pinterest is spending $190 billion a year on compute. The peer set prices an ads business and says almost nothing about this capex cycle, which has to be argued on Alphabet’s own numbers.

The figure that should give a bull pause is 317.83x NTM market cap to free cash flow. That is less a valuation signal than a sign that free cash flow has temporarily stopped being the right yardstick for this business. Fine, if the compression is a two-year window. A problem if 2027 capex, which Ashkenazi said would “significantly increase” compared to 2026, keeps pushing recovery to the right. The scale of the commitment is documented in Alphabet’s June 1 offering prospectus filed with the SEC, which lays out the $80 billion raise and Berkshire’s placement within it. Nobody outside the company can currently tell the two-year scenario from the longer one, which is a fair reading of why Buffett bought and hedged in the same breath.

TIKR Advanced Model Analysis

- Current Price: $370.92

- Target Price (Mid): ~$645

- Potential Total Return: ~74%

- Annualized IRR: ~13% / year

See analysts’ growth forecasts and price targets for Alphabet stock (It’s free!) >>>

The two revenue drivers are Google Cloud, where a $462 billion backlog with just over half converting inside 24 months gives visible compounding, and Search advertising, where AI Mode and AI Overviews are expanding monetizable query volume rather than cannibalizing it. The margin driver is Cloud operating leverage, with segment margin at 33% in the first quarter and further expansion expected as utilization rises against new capacity. The primary risk is that 2027 capex climbs faster than backlog converts, pushing the cash recovery beyond the model’s window and forcing a multiple reset from today’s 29x.

Upside: Cloud holds above 55% growth, and Search margins stay near 45%, and the mid case looks conservative. Downside: even TIKR’s low case, at a roughly 14% revenue CAGR and around 31% margin, still produces around 10% annualized returns, which is the strongest argument in the stock’s favor, because the pessimistic scenario is not a loss.

One note on horizon. TIKR’s price forecast chart runs to 2035, where the mid case reaches around $1,170, and the low and high cases sit near $855 and $1,570. The figures above are the 2030 anchor, and that is the one to hold management against.

Conclusion

July 22, after the close. Cloud grew 63% in the first quarter, and Pichai said just over half of the $462 billion backlog converts within 24 months. Anything at 55% or better says the backlog is real and the capex is buying revenue. Below 50%, and the conversion math starts to look like a promise rather than a schedule, with 2027 capex still climbing behind it.

Buffett bought the franchise and flagged the spending in the same breath. Six days from now the company gets to answer him.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Alphabet?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Alphabet, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Alphabet alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Alphabet on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!