Autodesk, Inc. (NASDAQ: ADSK) trades near $299/share and has delivered modest returns over the past year. Growth remains steady but not especially fast, and investors are watching to see whether margins can continue to expand as the company scales its subscription platform.

Recently, Autodesk shared new progress in its cloud transformation, including stronger adoption of Autodesk Construction Cloud and higher engagement across its design collaboration tools. The company also highlighted improving customer retention and stable usage patterns, suggesting demand remains resilient even in a softer macro environment. These updates show Autodesk is strengthening its competitive position as more workflows move online.

This article outlines where Wall Street analysts think Autodesk could trade by 2028, using the latest consensus targets and TIKR’s Guided Valuation Model. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

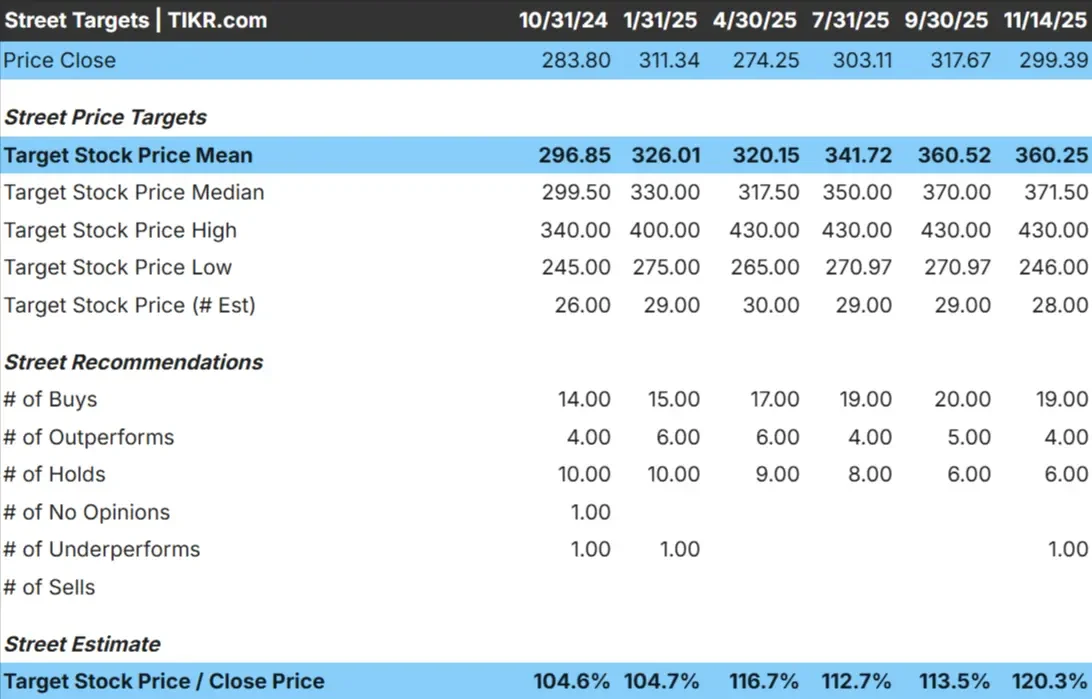

Autodesk trades at about $299/share today. The average analyst price target is $360/share, which points to around 20% upside. Forecasts show a steady range and reflect balanced sentiment:

- High estimate: ~$430/share

- Low estimate: ~$246/share

- Median target: ~$372/share

- Ratings: 19 Buys, 4 Outperforms, 6 Holds, 1 Underperforms

Analysts see modest upside from current levels. For investors, this means Autodesk could deliver slightly better-than-market returns if demand holds steady and margins continue to improve as its cloud transition progresses.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Autodesk: Growth Outlook and Valuation

The company’s fundamentals appear healthy, supported by subscription revenue and strong profitability:

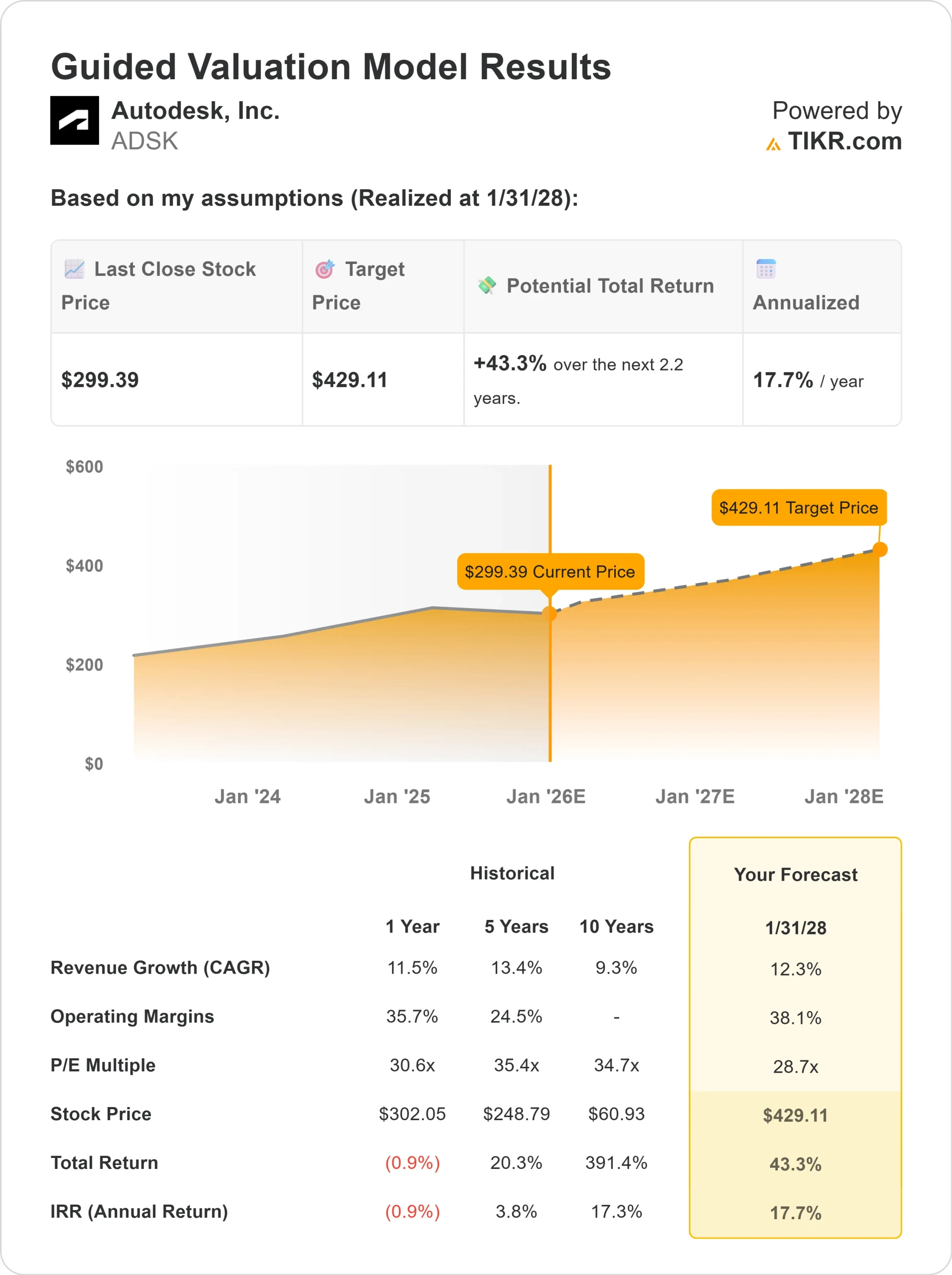

- Revenue growth: 12.3%

- Operating margins: 38.1%

- Shares valued at a 28.7x forward P E multiple in the model

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 28.7x forward P E suggests about $429/share by 2028

- That implies roughly 43% upside, or about 17.7% annualized returns

These numbers suggest Autodesk can compound steadily over the next few years. The company is not a rapid-growth story, but its predictable cash flow and margin strength give it a clear and sustainable earnings trajectory. For investors, Autodesk’s long term appeal lies in its stable revenue base and its growing cloud ecosystem.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Autodesk benefits from a large, sticky subscription base that provides reliable recurring revenue. Adoption of its cloud collaboration tools continues to increase, making customers more deeply integrated into its ecosystem.

Management has emphasized stable usage patterns and ongoing interest from architecture, engineering, and construction clients. For investors, these factors support a long term outlook where earnings can rise steadily even in mixed market conditions.

Bear Case: Growth Normalization and Valuation Risk

The main concern is that Autodesk’s growth may remain steady rather than accelerate. If revenue expansion slows or customer additions weaken, the stock’s premium valuation could be harder to justify.

There is also growing competition from alternative design platforms that offer lower cost or specialized tools. For investors, the risk is that any misstep in execution or softening in demand could weigh on the stock, given its higher earnings multiple.

Outlook for 2028: What Could Autodesk Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Autodesk could trade near $429/share by 2028. From today’s $299/share level, that represents roughly 43% upside, or about 17.7% annualized returns.

This outcome assumes steady growth and consistent margin performance. For Autodesk to deliver even more upside, it would likely need faster cloud adoption, deeper enterprise penetration, or stronger pricing power. Without that, investors should expect reliable but moderate compounding.

For investors, Autodesk stands out as a high quality software compounder with attractive long term potential. The potential returns are meaningful, but the story depends on the company continuing to execute and reinforcing its leadership across design and engineering workflows.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>