Key Stats for Applied Digital Corporation (APLD)

- 52-Week Range: $9.02 – $50.73

- Current Price: $41.00 (June 9, 2026)

- Street Target Price (Mean): ~$67

- Market Cap: ~$11.7B

- Fiscal Q3 2026 Revenue: $126.6M (+139% YoY)

- Fiscal Q3 2026 Adjusted EBITDA: $44.1M (vs $6.3M YoY)

- Total Cash: ~$1.93B (including restricted)

- Confirmed Contracted Revenue Backlog: Over $36B

- Long-Term NOI Target: $1B annually within 5 years

Value your favorite stocks like APLD with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

From $9 to $41: What Is Actually Happening at Applied Digital

Applied Digital (APLD) designs, builds, and operates next-generation data centers for AI workloads, using proprietary direct-to-chip liquid cooling to support rack densities that conventional facilities cannot handle.

The company operates three segments: HPC Hosting, its core AI data center business; Data Center Hosting, which provides powered space to bitcoin mining customers; and Cloud Services, which is currently being spun out through a merger with EKSO Bionics to form ChronoScale Corporation.

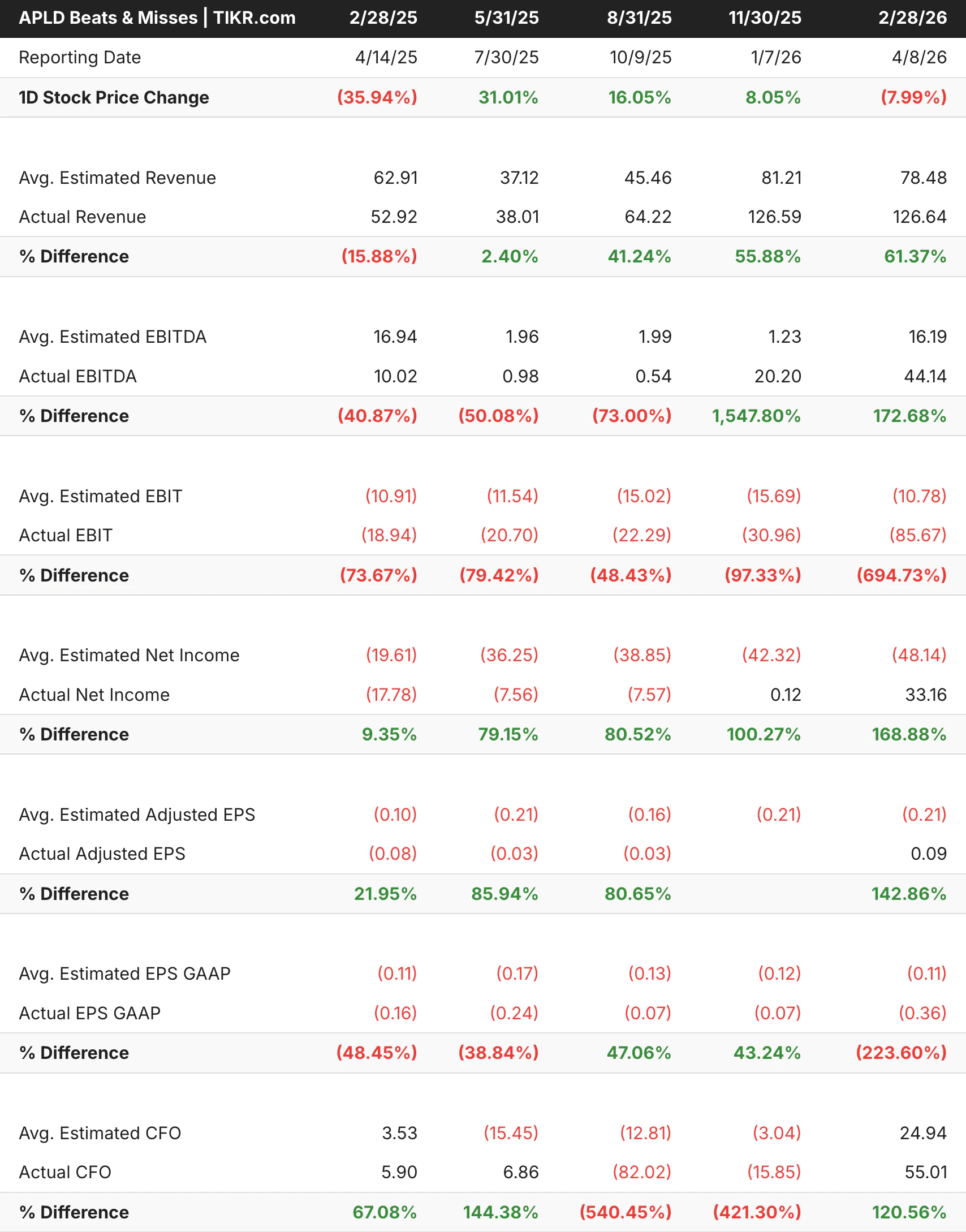

Fiscal Q3 2026, the quarter ended February 28, 2026, was the first full quarter of revenue from the company’s initial 100 MW building at Polaris Forge 1 in Ellendale, North Dakota. Revenue hit $126.6 million, up 139% from $52.9 million a year earlier.

Adjusted EBITDA came in at $44.1 million, up from $6.3 million a year ago. CEO Wes Cummins described the moment directly: “We believe that’s what matters to our customers, turning power into live AI capacity, delivered on time and performing as expected.”

The revenue and gross margin chart shows the historical buildup from $8.55 million in fiscal 2022 to $144.19 million in fiscal 2025, with gross margins climbing steadily toward 45% as the HPC Hosting business has scaled.

What the annual chart cannot yet show is the inflection already visible in the quarterly data: fiscal Q3 2026 revenue of $126.6 million now matches the entire fiscal year 2025’s revenue. The FY2026 annual figure, when reported on May 31, is on track to exceed $450 million.

See analysts’ growth forecasts and price targets for APLD (It’s free) >>>

The Contracted Pipeline and What the Execution Pattern Shows

Applied Digital now operates across five AI Factory campuses spanning 1.4 GW of contracted critical IT load. Total base-term contracted revenue stands at $36 billion, rising to approximately $86 billion if all renewal options are exercised, with roughly 70% of that revenue backed by U.S. investment-grade hyperscalers.

The most recent deal, Delta Forge 2, is a 210 MW campus under a 15-year take-or-pay lease with an investment-grade hyperscaler, expected to generate approximately $5.2 billion in base-term revenue. It is the third long-term lease Applied Digital has signed with the same counterparty.

Revenue has gone from a 16% miss a year ago to a 61% beat in Q3. Adjusted EBITDA moved from consistently large misses to a 172% beat, as the first fully operational building demonstrated the platform’s earnings power.

The EBIT line shows large misses throughout, but those are driven by non-cash items: $48.9 million in stock-based compensation and a $59.7 million write-down from the Cloud Services reclassification. The -8% stock reaction on Q3 reporting day reflects the GAAP headline rather than the operational reality.

Analyze Applied Digital stock on TIKR Free→

What the Street Is Saying About APLD

Analyst sentiment on Applied Digital is unusually unified: 11 analysts with active price targets rate the stock a buy, and 2 rate it outperform. There are no holds and no sells.

The mean target of around $67 implies roughly 63% upside from the current price, and the high target of $106 reflects a scenario in which the fully contracted pipeline delivers at expected margins.

The targets have moved in lockstep with business milestones, from roughly $12 in early 2025 to $67 today, as each building has come online on time and on budget.

What the Bulls Are Betting On

- The contracted backlog is exceptional for a company this size. Over $23 billion in 15- to 30-year take-or-pay leases with investment-grade hyperscalers provides revenue visibility that most growth companies never achieve. Each new building that comes online converts that backlog into durable cash flow.

- The 100 MW building is one-sixth of the contracted capacity. The operating leverage story has barely started. As the remaining capacity comes online, NOI should scale significantly toward the $1 billion annual target management has committed to within five years.

- On-time delivery is a genuine competitive advantage. In a market where hyperscalers are racing to secure power and purpose-built AI infrastructure, Applied Digital has delivered on schedule while others have faced delays. That track record is what wins the next lease.

What the Bears Are Watching

- The stock has a five-year beta of 5.7. Applied Digital is not a position for investors without tolerance for large swings. Delays in construction timelines, any reduction in hyperscaler capital spending, or a broader risk-off environment could move the stock sharply regardless of the underlying fundamentals.

- The debt load is significant and growing. Applied Digital carries approximately $2.7 billion in debt against a still-small earnings base, including $2.15 billion in senior secured notes at 6.75%. Servicing that debt requires the buildout to execute on schedule and at contracted margins, with limited tolerance for slippage.

- Tenant concentration is a real risk. CoreWeave represents approximately $11 billion of the contracted backlog at Polaris Forge 1. The post-quarter lease enhancements added meaningful protections, but dependence on a single tenant at the company’s flagship campus remains a factor for investors to weigh.

Access Professional Tools to Analyze APLD stock on TIKR for Free →

Should You Invest in Applied Digital Corporation?

Applied Digital is an infrastructure buildout story with a clear thesis: the world’s largest technology companies need massive, purpose-built AI compute capacity, they are signing 15-year take-or-pay contracts to secure it, and Applied Digital has the sites, the power, and the execution track record to deliver.

Near-term GAAP losses are real but largely non-cash. The adjusted EBITDA inflection and the over $23 billion in contracted backlog reflect a business performing ahead of expectations, and 11 analysts see it the same way.

Put on TIKR, and you get access to years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have trended over time, and whether price targets are trending up or down.

You can build a free watchlist to track Applied Digital Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!