Key Stats for Mastercard Stock

- Current Price: $492.88

- Target Price (Mid): ~$884

- Street Target: ~$647 Potential

- Total Return: ~82%

- Annualized IRR: ~14% / year

- Earnings Reaction: (1.48%) on 4/30/26

- Max Drawdown: (21.27%) on 6/3/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Mastercard Incorporated (MA) sits 18% below its 52-week high of $601.77, trading near $493 as of June 9, 2026. That gap has not opened because the business is deteriorating. It has opened because investors are uncertain whether the two technologies Mastercard is betting on most aggressively are tailwinds or threats.

At RBC Capital Markets’ Global Financial Technology Conference on June 9, Chief Product Officer Jorn Lambert spent an hour answering that question. His answers suggest the thesis is further along than the stock price implies.

Agent Pay Is Not a Feature. It Is a New Transaction Layer.

The core fear about agentic commerce AI models like ChatGPT or Gemini completing purchases on a consumer’s behalf is that it disrupts the traditional checkout flow, on which Mastercard earns fees. Lambert reframed the question at the conference.

“Over the last decades, the actors in e-commerce have been either the consumer, which initiated a transaction, or the merchant that initiates,” Lambert said. “Now we have an agent initiating a transaction. And the consumer is not authenticated at the merchant property. The consumer is authenticated at the agent property.”

That creates a trust problem Mastercard is structurally built to solve. The company’s Agent Pay program, built on the same tokenization infrastructure powering mobile payments globally, performs four functions: keeping malicious bots out, ensuring every party in the transaction chain knows which agent initiated it, cryptographically authenticating the consumer, and capturing the consumer’s original intent for dispute resolution. Microsoft, OpenAI, and Google are among the early partners.

Lambert’s estimate is that 20% to 30% of e-commerce will shift into agentic channels over the next several years. For a business processing 170 billion transactions annually, even a portion migrating to a natively tokenized channel adds services revenue, not just transaction volume.

The more interesting opportunity Lambert teased for the following day was machine-to-machine payments, where AI agents autonomously purchase services from other AI agents. His example: a small business owner asks an AI assistant to build a website, and the assistant independently contracts a domain registrar, a design platform, a payment gateway, and image libraries, completing multiple micro-transactions in seconds. “That is exactly what we like to do,” Lambert said. That is a net-new addressable market that does not exist today on any payment rail.

See historical and forward estimates for Mastercard stock (It’s free!) >>>

Why Stablecoins Expand Mastercard’s Market, Not Shrink It

The second fear is that stablecoins are cannibalizing card payments. Lambert was direct about why this framing is wrong. “Cards don’t move money,” he said. Cards are a messaging and authentication layer. Settlement happens behind the transaction on ACH or equivalent rails. Stablecoins are a faster settlement alternative to ACH, not a replacement for the Mastercard network layer.

In March 2026, Mastercard moved to own that settlement layer by agreeing to acquire BVNK, a UK-based stablecoin infrastructure provider, for $1.5 billion with up to $300 million in contingent payments. Per Mastercard’s deal announcement, BVNK processes approximately $30 billion in annual transaction volume across more than 130 countries, with clients including Worldpay, Deel, and Flywire. The deal is pending regulatory approval and expected to close before year-end 2026.

Lambert’s logic for the acquisition mirrors the same network-effect playbook that built the card business. Rather than becoming a blockchain, a stablecoin issuer, or a crypto wallet, Mastercard is positioning itself as the interoperability layer connecting all of them to the fiat world and to each other. The use cases he flagged as genuinely underpenetrated for Mastercard today: cross-border remittances, international payroll, and accounts payable flows between businesses. These are not card businesses. They are high-friction markets where stablecoins add real value, and where Mastercard has little existing share to protect.

“If you can organize this,” Lambert said, “I think we’ll have a very big runway.”

What the Numbers Say

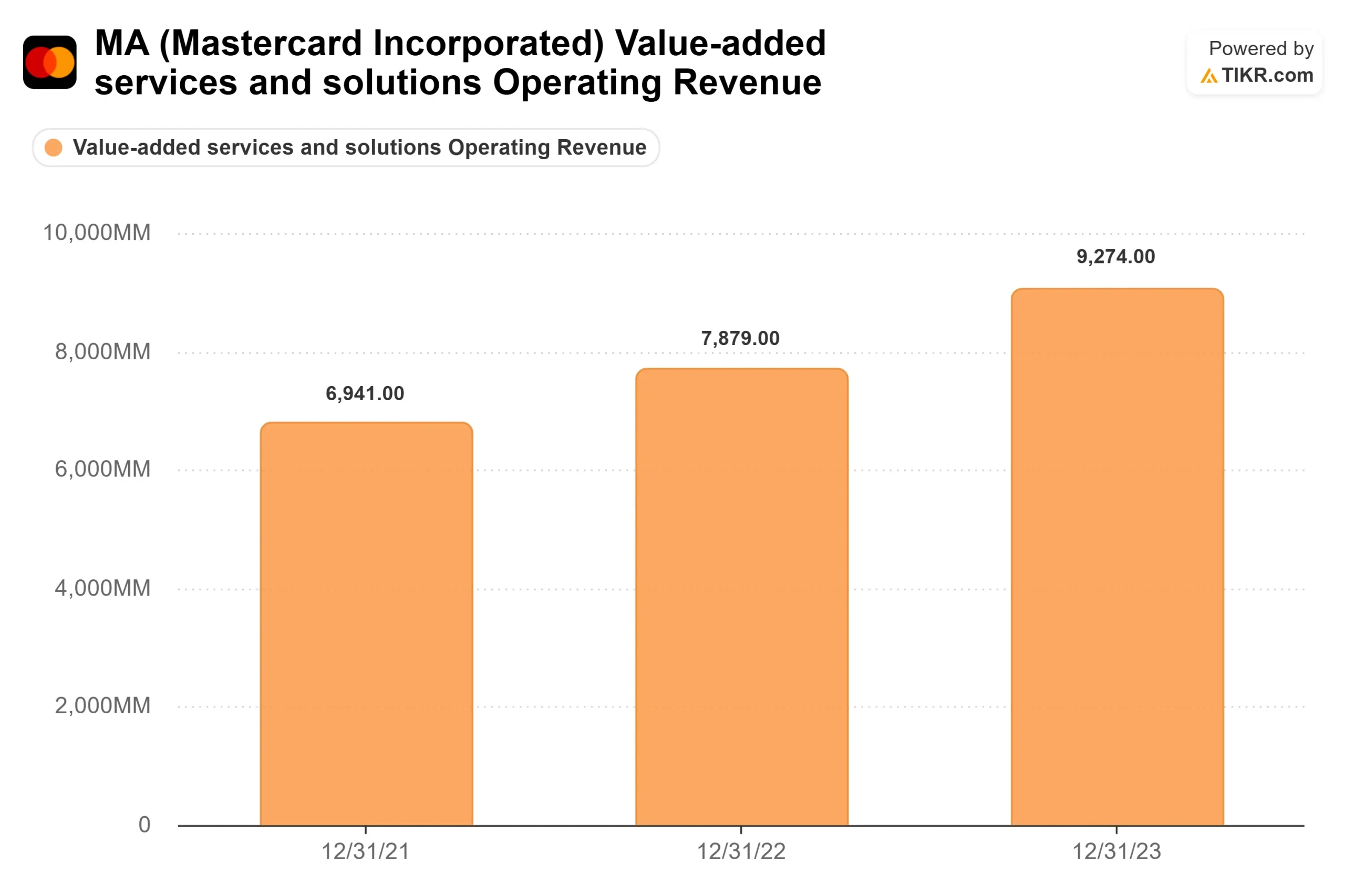

The business backing this strategy is producing consistent results. According to Mastercard’s Q1 2026 earnings release, net revenue grew 16% year-over-year to $8.4 billion, services and solutions revenue grew 22% on a currency-neutral basis, and the company beat analyst estimates on both revenue and EPS in each of the past five reported quarters per TIKR’s Beats & Misses data.

Yet the stock fell (1.48%) on earnings day, per TIKR. Management guided that Middle East geopolitical tensions were pressuring cross-border travel volumes into Q2, with recovery expected in the second half of the year. That guidance is what the market is pricing.

The LTM free cash flow figure is $16.4 billion (per TIKR’s FY2025 actuals). The ROIC sits at 77.7%, and the LTM EBIT margin at 59.5%. On an NTM EV/EBITDA basis, the stock trades at 18.22x as of 6/8/26, down from 26.41x at the start of 2025. The NTM P/E is 24.0x.

Of the 41 analysts covering the stock per TIKR’s Street Targets data as of 6/8/26, 29 rate it a Buy, 8 an Outperform, 2 a Hold, 2 a No Opinion, and 0 a Sell. The Street’s mean price target is ~$647. The analyst community has not changed its view on the business.

See how Mastercard performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $492.88

- Target Price (Mid): ~$884

- Potential Total Return: ~82%

- Annualized IRR: ~14% / year

See analysts’ growth forecasts and price targets for Mastercard stock (It’s free!) >>>

The TIKR mid-case model uses a revenue CAGR of around 9.5% and a net income margin of around 47%. Both are conservative: Mastercard’s 1-year, 5-year, and 10-year historical revenue CAGRs are 16.4%, 16.5%, and 13.0%, respectively, and the business delivered a 48.1% net income margin in fiscal 2025. The two primary revenue drivers are payment network volume growth led by the ongoing displacement of cash and checks, and value-added services expansion, which has been compounding faster than the core network.

The primary risk is the cross-border travel headwind. If the Middle East conflict extends into the second half of the year and suppresses high-margin travel volumes, full-year guidance comes under pressure. That is a real risk, not a theoretical one.

On the upside, the high case around 10.4% revenue CAGR and a 49.5% net income margin point to a target of approximately $1,486 with an IRR of around 14%. On the downside, the low case at around 8.5% growth and a 44% margin implies a target of approximately $902, still a positive return from current levels.

Conclusion

The single number that will determine whether the bull thesis accelerates or stalls is cross-border travel volume growth in Q2, reported on July 23, 2026. Management’s recovery thesis depends on sequential improvement from the depressed April levels they flagged on earnings day. If that improvement shows up, the geopolitical overhang clears, and the stock has a path back toward its 52-week highs. If cross-border travel remains soft through Q2, the recovery timeline extends, but the underlying business, the agentic infrastructure build, and the BVNK acquisition do not change.

The market is paying a 10-year low forward multiple for a business that just told investors it is building the trust layer for how AI agents will transact and how stablecoins will settle. July 23 is when the market gets its first answer on whether the near-term headwind is clearing.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Mastercard?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Mastercard, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Mastercard alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Mastercard on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!