Key Takeaways for Quanta Services Stock

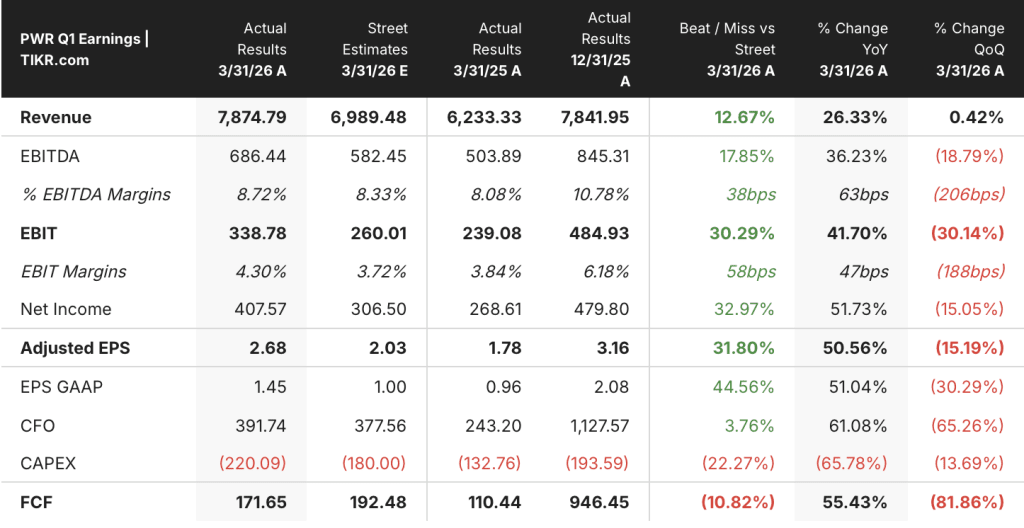

- Quanta Services stock posted Q1 2026 revenue of $7.87 billion, up 26% year over year, beating Street estimates by 13%

- Adjusted EPS of $2.68 came in 32% above consensus, with adjusted EBITDA reaching $686 million

- Gross profit grew 33% year over year to $1.11 billion, yet gross margin held at 14%, leaving operating margin at just 4%, a gap of roughly 10 percentage points

- The TIKR model mid-case target price for Quanta Services stock is $901, implying 30% total return over the next 4.6 years at 6% annualized

Quanta Services Stock Posts 26% Revenue Growth as the Margin Gap Tells the Real Story

Quanta Services (PWR) opened 2026 with its strongest first-quarter revenue result on record, reporting $7.87 billion in Q1 2026 sales on April 30, a 26% increase from $6.23 billion in the same period a year earlier.

CEO Duke Austin described the result as reflecting “robust double-digit growth” across revenues, adjusted EBITDA, and adjusted earnings per share, anchored by a record $48.5 billion backlog that management said gives clear visibility into the remainder of the year.

At the Bernstein Strategic Decisions Conference in late May, Austin went further, telling investors that utility capital conversations now extend well past 2030, with combined-cycle gas generation orders already pushing build timelines into 2033 and beyond.

CFO Jayshree Desai raised full-year revenue guidance to a range of $34.7 billion to $35.2 billion, full-year adjusted EBITDA guidance to $3.49 billion to $3.65 billion, and full-year adjusted EPS guidance to a range of $13.55 to $14.25.

Austin attributed Q1 execution strength in part to the Underground and Infrastructure segment, where work mix improvements, including contributions from the DSI mechanical platform acquisition, drove what he called “incremental margin improvement” that he expects to continue toward double-digit operating margins within that segment.

Track PWR’s income statement across every quarter on TIKR. See the full history in one place.

Why Quanta Services Stock’s 10-Point Margin Gap Is the Investment Question for 2030

Quanta Services stock’s revenue growth trajectory across the past eight quarters is difficult to dispute, with year-over-year gains accelerating from 11% in Q2 2024 to 24% in Q1 2025 and now 26% in Q1 2026, reaching $7.87 billion for the most recent period.

Gross profit followed that acceleration, growing 33% year over year in Q1 2026 to $1.11 billion, recovering sharply from the $0.83 billion trough in Q1 2025 when gross margin compressed to 13%.

The more important dynamic is what happens between gross profit and operating income: with gross margin at 14% in Q1 2026 and operating margin at only 4%, Quanta Services stock is absorbing roughly 10 percentage points of revenue in operating costs before a dollar reaches the operating line.

Total operating expenses rose to $0.77 billion in Q1 2026, up 28% from $0.60 billion a year prior, a rate that essentially matched revenue growth and prevented gross profit expansion from converting into operating leverage.

Operating income still grew 45% year over year to $0.33 billion, a meaningful improvement from the $0.23 billion Q1 2025 result, but operating margin at 4% remains at the low end of the eight-quarter range that spans 4% to 7%, with the 7% peak reached in Q3 2025 now serving as the high-water mark the business has not yet sustained.

How Quanta Services Stock’s Operating Margin Compares to Infrastructure Peers in Q1 2026

Quanta Services stock posted a 4% operating margin in Q1 2026, sitting between MasTec’s (MTZ) 4% and Dycom’s (DY) 7% in the same period, placing PWR in the middle of the infrastructure services peer range rather than at either extreme.

Dycom’s 7% operating margin in Q1 2026 represents the peer ceiling and establishes that double-digit gross margins can convert into meaningfully higher operating returns when the cost structure is tighter, a gap of roughly 3 percentage points above where Quanta Services stock currently operates.

MasTec’s 4% operating margin in Q1 2026 confirms that the lower end of the peer range is not a Quanta-specific problem, but the trajectory divergence matters: Dycom held above 8% in Q2 and Q3 2024 while both PWR and MTZ compressed, suggesting the margin gap between Quanta Services stock and its highest-performing peer is structural, not cyclical.

The TIKR Model Puts Quanta Services Stock at $901 by 2030, With the Return Riding on Margin Delivery

The TIKR base case values Quanta Services stock at a mid-case target of $901, against a current price of $692, representing around 30% total return over the next 4.6 years at roughly 6% annualized.

If Quanta Services stock’s revenue grows at around the mid-case CAGR and operating margins begin to close the gap toward the 7% range seen in Q3 2025, the pathway to $901 becomes credible on current execution trends.

Should operating leverage stall and the cost structure continue absorbing gross profit gains at the current rate, with margins staying in the 4% range, the low-case scenario around $960 by 2034 at roughly 4% annualized reflects a longer, slower compounding story.

If mix shift in the Underground segment and the integrated solutions model accelerate margin expansion as Austin suggested at Bernstein, and revenue growth holds near 13% CAGR, the high-case path to around $1,745 by 2034 at roughly 11% annualized becomes the scenario where the 2030 earnings-doubling thesis delivers ahead of schedule.

Is Quanta Services stock a good investment right now?

The TIKR mid-case model targets $901 for Quanta Services stock, implying around 30% total return over 4.6 years at roughly 6% annualized from a current price of $692.

Revenue grew 26% year over year in Q1 2026, and the record $48.5 billion backlog provides visibility into that growth continuing.

The key risk is whether operating margin, currently at 4%, expands toward the 7% level seen in Q3 2025 as the revenue base scales.

Why is Quanta Services stock’s operating margin so low compared to its gross margin?

Quanta Services stock carries a roughly 10-point gap between its 14% gross margin and its 4% operating margin in Q1 2026.

Total operating expenses reached $0.77 billion in the quarter, up 28% year over year, consuming the majority of gross profit growth.

SG&A of $0.62 billion and goodwill amortization from acquisitions are the primary cost layers between the gross line and operating income.

What is driving Quanta Services stock’s revenue growth in 2026?

Quanta Services stock reported $7.87 billion in Q1 2026 revenue, up 26% year over year, driven by broad-based growth across electrical infrastructure, the Underground and Infrastructure segment, and technology and large load facilities.

Management raised full-year revenue guidance to a range of $34.7 billion to $35.2 billion, supported by a record $48.5 billion backlog and accelerating demand from utilities and hyperscalers for mission-critical infrastructure build-out.

Should You Invest in Quanta Services Stock?

Quanta Services stock is a direct play on what Duke Austin called a decades-long infrastructure cycle, with utilities being asked to double in size and hyperscalers demanding construction certainty at a scale the industry has not encountered before.

The Q1 2026 income statement confirms the revenue story is real: 26% top-line growth, 33% gross profit growth, 45% operating income growth.

The unresolved question is whether operating margins can expand toward the 7% range on a sustained basis, or whether the cost structure keeps resetting each quarter near 4%.

At $692, the TIKR mid-case implies 6% annualized return through 2030.

Investors who believe the margin gap narrows as mix shifts and the integrated solutions model matures have a reasonable case.

Investors who require evidence of sustained operating leverage before adding exposure should watch the next two to three quarters closely, as Q3 and Q4 have historically been when Quanta’s cost structure catches up to its revenue.

Access Professional Tools to Analyze PWR stock on TIKR for Free →