Key Stats for Marriott International Stock

- 52-Week Range: $254 to $397

- Current Price: $391

- Street Mean Target: $378

- Street High Target: $446

- Analyst Consensus: 11 Buys / 1 Outperform / 12 Holds / 1 Underperform / 1 Sell

- TIKR Model Target (Dec. 2030): $421

Marriott Beats Q1 Estimates and Raises Full-Year RevPAR Guidance, but the Middle East Is the Story Nobody Wanted

Marriott International (MAR), the world’s largest hotel company with nearly 9,500 properties across 141 countries, reported Q1 2026 adjusted EPS of $2.72, beating the consensus estimate of $2.55.

Global RevPAR rose 4.2% year over year in Q1, with U.S. and Canada up 4.0% and international up 4.6%.

The breadth of that domestic performance stood out.

Luxury RevPAR in U.S. and Canada rose nearly 7%, while select service RevPAR climbed 3.5% — a significant shift from Q4 2025 when select service was down more than 1% year over year.

Asia Pacific RevPAR rose over 7%, driven by higher average daily rates and a surge in demand from Chinese guests.

RevPAR in Caribbean and Latin America rose 2%, led by record leisure results in the Caribbean, though Mexican luxury resorts weighed on the regional number.

Then came the disruption.

In March, the Middle East conflict (which erupted in late February) hit Marriott’s properties hard, with Middle East RevPAR dropping over 30% in that single month alone.

Marriott raised its full-year global RevPAR guidance to 2% to 3% growth, up from the prior 1.5% to 2.5% range, but that upgrade comes with a significant asterisk: CFO Jen Mason said the conflict could trim full-year global RevPAR growth by 100 to 125 basis points, with the most severe hit expected in Q2 when Middle East RevPAR is projected to fall about 50%.

The World Cup offset is real but limited in scale.

Mason confirmed on the Q1 2026 earnings call that the tournament is “still expected to add 30 to 35 basis points to global RevPAR growth this year,” with uplift spread across Q2 and Q3 — and the company’s June and July bookings in U.S. and Canada markets are pacing up, including in non-World Cup markets.

Development momentum remained strong.

Q1 global deal signings were up 9% year over year, the global pipeline reached a record of nearly 618,000 rooms, and net rooms growth over the trailing 12 months hit 4.5%.

Co-branded credit card fees rose 37% in Q1 and are still expected to increase around 35% for the full year — and that figure does not yet include any impact from renegotiated U.S. card deals with Visa, Chase, and American Express, which management says are progressing and expected to close in the second half.

“We’re back to kind of pre-conflict trends in terms of domestic versus international travel bookings from the US,” Mason said on the earnings call.

Marriott stock also raised its quarterly dividend to $0.73 per share, payable June 30, 2026.

MAR Analysts Back the Growth Story but the Stock Is Priced Close to Fair Value

Marriott stock’s adjusted EBITDA increased 15% year over year in Q1 to around $1.4 billion, and the full-year EBITDA outlook sits between approximately $5.88 billion and $5.97 billion, representing around 9% to 11% growth.

Consensus estimates project Q2 2026 revenue of around $7.17 billion, up around 6% year over year, with EBITDA margins expected near 21.5%.

For Q3 2026, estimates call for revenue of around $6.92 billion, up roughly 7% year over year, with EBITDA expected near $1.48 billion.

Full-year 2026 adjusted EPS guidance is $11.38 to $11.63, representing around 14% to 16% growth.

EPS estimates extend the growth profile further: normalized EPS is projected at around $3.05 for Q2 2026, up approximately 15% year over year, rising to around $2.98 in Q4 2026.

The 37% credit card fee jump and over 70% increase in residential branding fees in Q1 demonstrate that Marriott’s non-RevPAR revenue streams are growing faster than the room business itself.

Of the 26 analysts covering MAR, 11 rate it a Buy, 1 rates it Outperform, 12 rate it Hold, 1 Underperform, and 1 Sell.

The Street’s mean target sits at around $378, below the current price of around $391 which is a “rare configuration” that signals the market has moved ahead of analyst consensus.

The Street high of $446 implies around 14% upside from current levels, but that target likely requires Middle East recovery, credit card renegotiation upside, and World Cup execution all going right simultaneously.

At around $391, Marriott stock is priced at or above what most analysts currently think it is worth, making it fairly valued relative to the current consensus even as the EPS and EBITDA growth trajectory remains one of the stronger profiles in global hospitality.

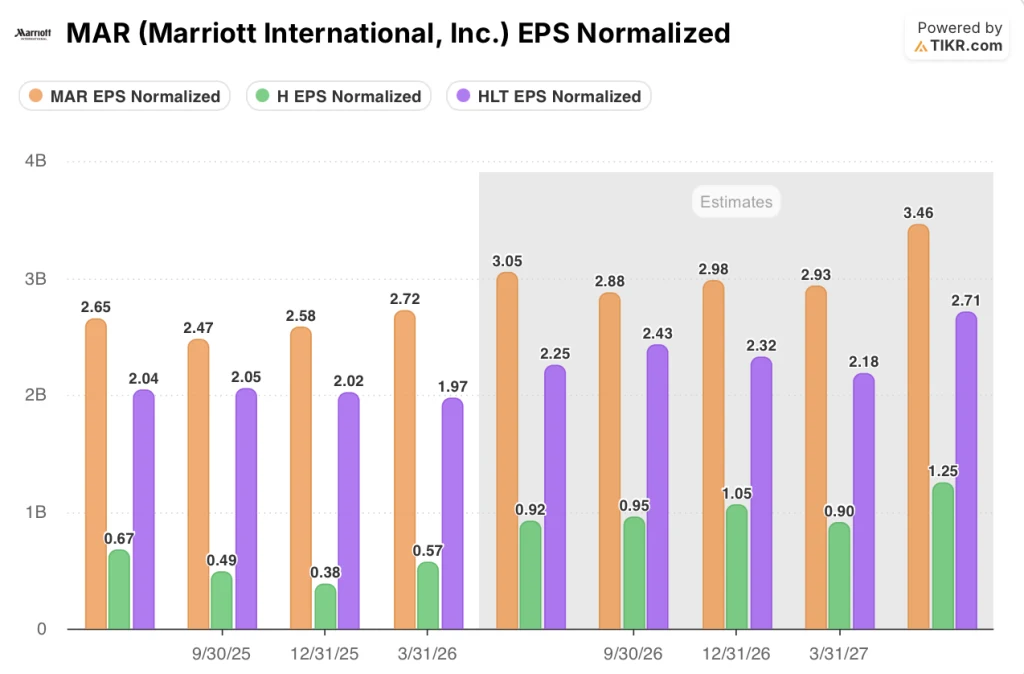

Marriott Stock Leads MAR, HLT, and H on EPS and the Gap Is Widening

Marriott stock’s normalized EPS of $2.72 in Q1 2026 was more than 2.3 times Hilton’s (HLT) $1.97 and nearly 5 times Hyatt’s (H) $0.57 in the same quarter.

The forward estimates extend that gap rather than narrow it: Q2 2026 consensus puts Marriott at $3.05, Hilton at $2.43, and Hyatt at $0.92.

By Q1 2027, Marriott stock’s normalized EPS is projected at $3.46, compared to $2.71 for Hilton and $1.25 for Hyatt — a spread that reflects Marriott’s larger system size, its co-branded credit card program generating fees at a scale neither peer matches, and a pipeline of nearly 618,000 rooms that dwarfs both competitors.

The implication for valuation is not straightforward: Marriott’s EPS lead is structural, but investors have already paid for it, which is exactly why the stock now trades above the Street mean while Hilton and Hyatt still sit below their respective consensus targets.

Is Marriott Stock Undervalued in 2026? What the TIKR Model Says at $421

TIKR’s base case values Marriott International at approximately $421 by December 2030, implying around 8% total return from the current price of around $391, or roughly 2% annualized over approximately 4.6 years.

If revenue grows at roughly 3.5% annually through 2030, net income margins hold near 11.5%, and EPS compounds at approximately 6% per year, the TIKR model’s mid-case lands near $476 by December 2034, representing around 22% total return and roughly 2% annualized return over the longer horizon.

If revenue growth slows to around 3.2% and EPS growth compresses to approximately 5%, the low case produces a stock price near $389 by 2030, essentially flat from current levels with around a (0.1)% annualized return.

If Marriott executes on credit card renegotiations, Middle East recovery arrives faster than guided, and EPS grows at roughly 6.5% annually, the high case reaches near $562 by 2034, implying around 44% total return and roughly 4% annualized return.

The TIKR model makes clear that Marriott stock is not a mispriced opportunity at current levels — the base case barely clears the current price, and the annualized return in the mid scenario sits at roughly 2%. The upside exists, but it requires capturing the high case: full credit card deal monetization, Middle East stabilization, and sustained EPS compounding above current consensus.

Is Marriott stock a buy right now?

At around $391, Marriott stock is trading above the Street’s mean price target of around $378, suggesting the easy upside has already been priced in.

The TIKR base case points to a target of approximately $421 by 2030, implying modest returns unless the World Cup tailwind and credit card renegotiations produce upside beyond current guidance.

Investors with a higher conviction on Middle East recovery and credit card deal monetization have a more compelling case.

What do analysts say about Marriott International stock?

Of 26 analysts covering MAR, 11 rate it a Buy or Outperform and 12 rate it Hold, with 2 negative ratings. The Street mean target of around $378 sits below the current price, a signal that analysts on balance view the stock as fairly valued or slightly stretched.

The Street high of $446 remains achievable if full-year EBITDA reaches the top end of guidance and credit card renegotiations close on favorable terms in the second half of 2026.

Should You Invest in Marriott International, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Marriott International stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Marriott International alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MAR stock on TIKR for Free →