Key Stats for Palantir Stock

- 52-Week Range: $123 to $208

- Current Price: $136

- Street Mean Target: $184

- Street High Target: $255

- Analyst Consensus: 18 Buys / 1 Outperform / 10 Holds / 1 Underperform / 1 Sell

- TIKR Model Target (Dec. 2030): $985

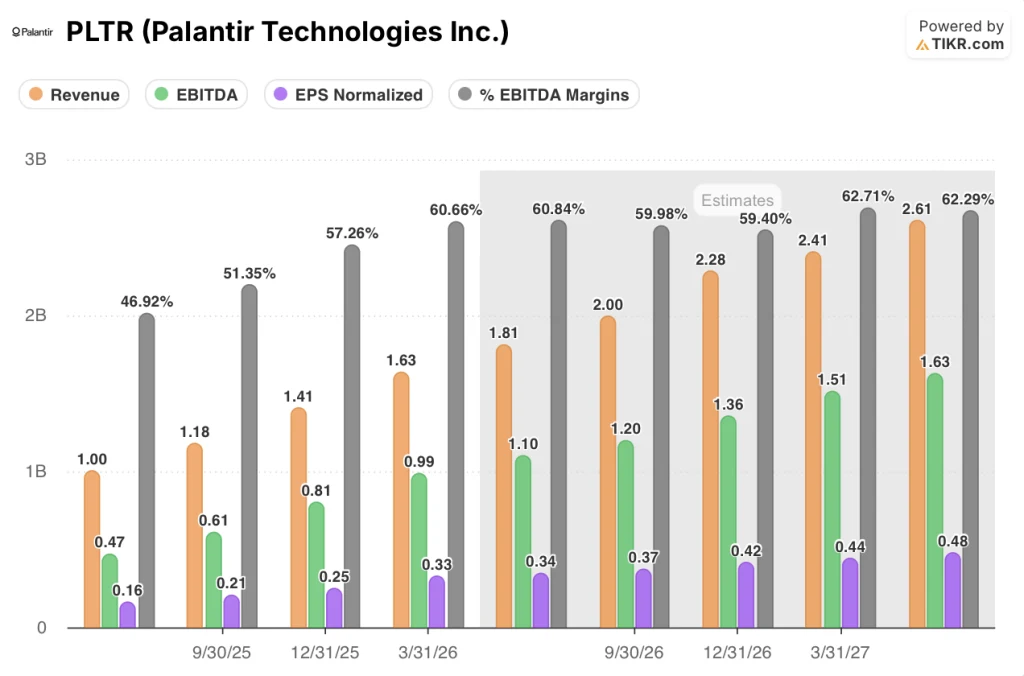

Palantir Stock Delivers 85% Revenue Growth in Q1 2026 and Raises Full-Year Guidance by 10 Points

Palantir Technologies (PLTR) reported Q1 2026 revenue of $1.633 billion, growing 85% year over year, the highest reported growth rate in its history as a public company.

The U.S. business crossed a milestone that management had been targeting for over a year, delivering 104% year-over-year revenue growth to around $1.282 billion, the first time since the company’s direct public offering that U.S. growth has exceeded triple digits.

U.S. commercial revenue was the engine, growing 133% year over year and 18% sequentially to around $595 million.

U.S. government revenue followed, growing 84% year over year and 21% sequentially to around $687 million.

The quarter was not driven by a single outsized contract or one-time recognition event.

Palantir closed $1.3 billion in commercial total contract value bookings, representing 42% growth year over year, and for the third consecutive quarter, U.S. commercial TCV bookings exceeded $1 billion, with Q1 coming in at around $1.2 billion, up 45% year over year.

Net dollar retention reached 150%, an 1,100-basis-point increase from the prior quarter, a figure that does not yet capture revenue from new customers acquired in the past 12 months.

The company ended Q1 with $11.8 billion in total remaining deal value, up 98% year over year.

Customer count grew to 1,007, up 31% year over year.

Free cash flow came in at around $925 million for the quarter, representing a 57% margin, and the company held approximately $8 billion in cash and treasury securities at quarter end.

On the Q1 call, CEO Alex Karp put it directly: “Our free cash flow this quarter is larger than our revenue a year ago in the same quarter.”

Management raised full-year 2026 revenue guidance to a midpoint of around $7.656 billion, representing roughly 71% growth year over year, a 10-point increase over the prior quarter’s guidance, their largest ever full-year guidance raise.

The Rule of 40 score, combining revenue growth and adjusted operating margin, reached 145%, up 18 points quarter over quarter and the 11th consecutive quarter of expansion.

Six partnerships and contract expansions were announced in the days surrounding the report, spanning construction (McCarthy Building), insurance (GNP Seguros), legal technology (Kirkland and Ellis), cloud distribution (Google Cloud), defense analytics (Ukraine’s Brave1 Dataroom), and U.S. agricultural security (a USDA contract of up to around $300 million).

What Wall Street Thinks About Palantir Stock After Record Growth

The consensus shift has been sharp.

At the end of Q1 2025, Palantir stock had 3 Buys and 15 Holds among covering analysts. By early June 2026, that distribution had moved to 18 Buys, 1 Outperform, 10 Holds, 1 Underperform, and 1 Sell, with 27 analysts now covering the stock.

The mean price target of around $184 implies roughly 35% upside from the current price of around $136, and the high target of around $255 reflects nearly 87% upside from the same level.

Revenue consensus supports the bullish case.

Q2 2026 consensus revenue stands at around $1.81 billion, representing roughly 80% year-over-year growth and 11% sequential growth from Q1, with management guiding to a range of around $1.797 billion to $1.801 billion.

For the remainder of 2026, consensus revenue estimates reach approximately $2.00 billion in Q3 and approximately $2.28 billion in Q4, implying full-year consensus closer to around $7.7 billion.

EBITDA consensus for Q2 2026 sits at around $1.10 billion, representing a roughly 61% EBITDA margin and approximately 134% year-over-year growth.

The EPS trajectory anchors the argument.

Q1 2026 normalized EPS came in at $0.33, growing 154% year over year. Consensus projects Q2 2026 normalized EPS of $0.34, then $0.37 in Q3, $0.42 in Q4, and approximately $0.44 in Q1 2027, each quarter marking consecutive expansion.

At around $136, with the company guiding to over $4.44 billion in adjusted operating income for the full year and consensus projecting EPS growth accelerating through every remaining quarter of 2026, Palantir stock is undervalued relative to what the earnings trajectory implies. A company growing EPS at triple-digit rates while expanding adjusted operating margins to 60% does not typically trade at a 26% discount to the Street’s mean price target, and the fact that it does reflects valuation hesitation about duration, not disagreement about execution.

The risk is front and center. The UK parliamentary committee’s designation of Palantir as an “unacceptable point of weakness” in British public sector dependency creates a headline overhang on the international government segment, and continued insider selling at prices between roughly $132 and $160 reinforces the perception that the stock is fully valued at current levels rather than cheap.

The catalyst to watch is Q2 earnings, where management is guiding to adjusted operating income of between around $1.063 billion and $1.067 billion. If U.S. commercial revenue approaches $700 million or above, the growth rate for the segment will have been sustained at over 100% for two consecutive quarters, the kind of durability that historically forces a consensus re-rating.

Is Palantir Stock Undervalued in 2026? TIKR’s $985 Target and the Compression That Makes It Work

TIKR’s base case values Palantir stock at approximately $985 by December 2030, implying around 622% total return from the current price of around $136, or roughly 54% annualized over approximately 4.6 years.

The model builds in P/E compression of around 8% to 10% per year across all three scenarios, which means every dollar of return in every case is carried by earnings growth alone.

If U.S. commercial momentum holds at the pace management has guided and the EPS CAGR of around 53% in the mid case mirrors the 132% three-year historical rate, the model projects a 2035 price of approximately $4,624, a roughly 3,288% total return and an IRR of around 51%.

If growth decelerates and the low-case EPS CAGR of around 47% proves closer to reality, the implied 2035 price drops to approximately $2,727, still representing an IRR of around 42%.

The high case, anchored to EPS CAGR of around 59% and full-year U.S. commercial revenue growth guidance of at least 120% sustaining, produces a 2035 price of approximately $7,559 and an IRR of around 60%. In all three scenarios, Palantir stock is undervalued today because the compression the model expects is already built into a price that still implies outsized returns even at the lowest growth assumption.

What is the price target for PLTR?

The current Street mean target is approximately $184 per share, with the high target at approximately $255. TIKR’s base case model targets approximately $985 per share, implying roughly 622% total return over approximately 4.6 years from the current price.

Is Palantir stock undervalued or overvalued?

At approximately $136, Palantir stock trades at a 26% discount to the Street mean target while the company grows revenue at 85% year over year and guides to roughly 71% growth for the full year.

Whether that is cheap depends on how much of the forward earnings trajectory an investor is willing to price today.

TIKR’s base case model, embedding EPS CAGR of around 53% through 2035 and built-in P/E compression of around 8% per year, implies a mid-case price of approximately $4,624 by 2035 and a nearer-term target of approximately $985.

Should You Invest in Palantir Technologies?

The only way to determine whether Palantir stock’s valuation is justified is to stress-test the assumptions yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to do exactly that.

Pull up Palantir Technologies stock and you will see years of historical financials, what Wall Street analysts expect for revenue and normalized EPS in the quarters and years ahead, how the valuation multiples have moved over the past two years, and whether price targets are trending up or down across the entire coverage universe.

You can build a free watchlist to track Palantir Technologies alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PLTR stock on TIKR for Free →