Key Stats for Constellation Energy Stock

- 52-Week Range: $242 to $413

- Current Price: $251

- Street Mean Target: $367

- Street High Target: $441

- Analyst Consensus: 13 Buys / 6 Outperforms / 2 Holds / 1 Sell

- TIKR Model Target (Dec. 2030): $480

CEG Beats Q1 Estimates, Prices a $3.1 Billion Secondary, and Drops Anyway

Constellation Energy (CEG), the largest nuclear power operator in the United States, posted Q1 2026 adjusted operating earnings of $2.74 per share, beating the consensus estimate of $2.57 per share.

Total Q1 revenue came in at $11.12 billion, up 63.8% from $6.79 billion in Q1 2025, driven by the addition of Calpine assets following the January 2026 close of its $16 billion acquisition.

The company reaffirmed full-year 2026 adjusted operating earnings guidance of $11 to $12 per share and said it expects Calpine to contribute approximately $2 per share of EPS accretion for the full year.

On May 14, Constellation announced a minority equity purchase agreement in five Pine Creek RNG facilities, adding approximately 3 million MMBTUs of additional renewable natural gas production annually.

On June 1, existing shareholders launched an 11 million-share secondary offering priced at $281, a 2.3% discount to the prior close, with no proceeds going to the company.

Constellation used the event to immediately step in as a buyer, repurchasing 2 million shares from the underwriters at the $281 offering price under its existing $5 billion buyback authorization.

The move came after CEO Joe Dominguez said on the Q1 earnings call, “at these prices, we see our stock as a compelling use of our cash,” referring to an earlier buyback of approximately 1.2 million shares at an average price of around $285 in the weeks after the March investor day.

On June 2, FERC granted a waiver allowing Constellation to transfer certain grid injection rights from its Eddystone natural gas plant to the Three Mile Island restart project, known as Crane Clean Energy Center, clearing the path for a 2027 restart target that had been threatened by a potential 2031 grid connection delay.

On June 8, Constellation unit Calpine completed a 25-megawatt expansion at The Geysers geothermal complex in California, the latest operational execution in its newly integrated gas and geothermal portfolio.

The 25-megawatt Geysers expansion will supply electricity for more than 25,000 homes annually, with 18 megawatts contracted to Clean Power Alliance.

Why 19 of 21 Analysts Are Still Bullish on Constellation Energy Stock After a 19% YTD Decline

Constellation Energy stock’s revenue is expected to reach around $8.7 billion in Q2 2026 and around $10.4 billion in Q3 2026, representing year-over-year growth of around 43% and 59% in each quarter, according to forward consensus estimates.

The EPS growth trajectory is steeper than the revenue line suggests.

Q2 2026 normalized EPS is estimated at $2.57, rising to $3.67 in Q3 and $2.85 in Q4, adding up to a full-year consensus view broadly consistent with the $11 to $12 guidance range.

The driver behind that trajectory is Calpine, which added a combined cycle and cogeneration fleet producing 23 million megawatt hours in Q1 alone at a 47.1% capacity factor, alongside Constellation’s nuclear fleet operating at a 92.3% capacity factor.

The nuclear production tax credit (PTC), which grows with inflation and is embedded across the fleet, provides a visible floor that most analyst models are treating as structural rather than cyclical.

Constellation Energy stock’s free cash flow before growth is forecast at $8.4 billion across 2026 and 2027 combined, rising to between $11.5 billion and $13 billion in 2028 and 2029, a trajectory of roughly 45% growth on the midpoint from one two-year period to the next.

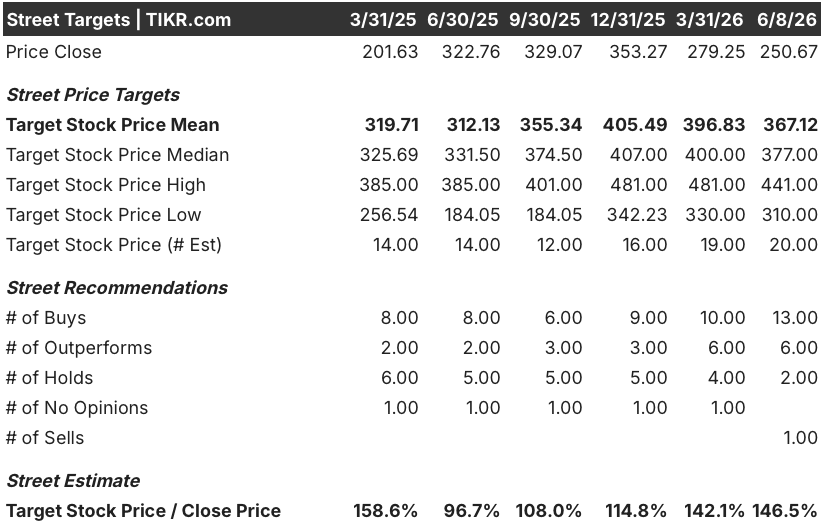

At current prices, 13 analysts rate Constellation Energy stock a Buy, 6 rate it Outperform, 2 Hold, and 1 Sell, for a total coverage base of 22 analysts.

The street mean target stands at $367, implying around 46% upside from the June 8 close of $251, while the street high of $441 implies around 76% upside.

With management buying back shares at $281 and $285, and the street mean sitting at $367, Constellation Energy stock looks materially undervalued at $251.

The risk the market is pricing in is real: PJM regulatory clarity has not fully arrived, the Crane restart timeline remains contingent on FERC’s final order, and the June 30 lockup expiration on 25 million Calpine-linked shares creates a near-term supply risk that could pressure the stock further.

Constellation Energy Stock Leads NRG and Vistra on EPS Normalized Every Quarter in Sight

Constellation Energy stock posted normalized EPS of $2.74 in Q1 2026, ahead of NRG Energy (NRG) at $1.73 and Vistra (VST) at $1.46 in the same quarter.

The gap widens in the forward estimates: CEG is projected at $3.67 in Q3 2026 against $2.91 for NRG and $2.11 for Vistra, a lead that reflects the Calpine accretion flowing through the earnings line while peers lack a comparable step-change catalyst.

By Q1 2027, CEG’s estimated $2.64 still sits above Vistra’s $3.18 on that single quarter, the one period where Vistra’s estimate overtakes CEG, though NRG’s $2.08 trails both, making Constellation Energy stock the consistent earnings leader across the peer set with only one quarter of compression relative to VST in the visible window.

Is Constellation Energy Stock Undervalued in 2026? TIKR’s $480 Target Says Yes

TIKR’s base case values Constellation Energy at around $480 by December 2030, implying around 92% total return from the current price of $251, or roughly 15% annualized over approximately 4.6 years.

If Calpine accretion holds and PJM regulatory clarity arrives on the timeline management expects, the mid-case path to around $628 by December 2034 represents a total return of around 151% at an IRR of around 11%.

If the Crane restart reaches full capacity credit on the 2027 schedule and the data center contracting pipeline in both ERCOT and PJM materializes at scale, the high case reaches around $809 by December 2034, an IRR of around 15%.

If PJM clarity slips and the June 30 lockup on Calpine-linked shares creates forced selling, Constellation Energy stock could remain range-bound through 2026 — but even the low case reaches around $472 by December 2034 at an IRR of around 8%, still roughly doubling from here.

The risk is timing, not the thesis.

Is Constellation Energy stock a buy in 2026?

At $251, the stock trades well below the street mean target of $367 and the street high of $441, with 19 of 21 analysts holding a buy or outperform rating.

Management itself stepped in to repurchase shares at $281 to $285, signaling conviction.

The primary near-term risk is the June 30 lockup expiration on 25 million Calpine-linked shares, which could create additional selling pressure before the thesis fully plays out.

What is the price target for CEG stock?

The street mean target is $367, implying around 46% upside from the June 8, 2026 close of $251.

The street high stands at $441.

The TIKR model mid-case target is around $480, realized at December 2030, representing a potential return of around 92% over approximately 4.6 years at an annualized rate of around 15%.

Should You Invest in Constellation Energy?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to evaluate exactly this question.

Pull up Constellation Energy stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and EPS in the quarters ahead, how the Calpine acquisition changed the earnings profile, and whether analyst price targets are moving toward or away from $367.

You can build a free watchlist to track Constellation Energy alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CEG stock on TIKR for Free →