Key Stats for Western Digital Stock

- 52-Week Range: $55 to $603

- Current Price: $527

- Street Mean Target: $537

- Street High Target: $685

- Analyst Consensus: 17 Buys / 4 Outperforms / 3 Holds / 1 Underperform

- TIKR Model Target (Dec. 2030): $944

Western Digital Posts Record Q3 Results as AI Storage Demand Outruns HDD Supply

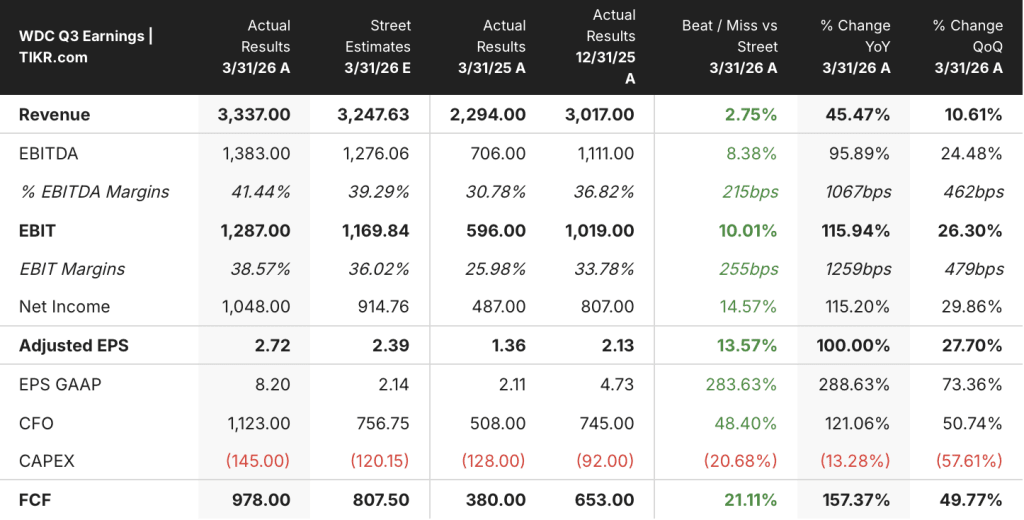

Western Digital Corporation (WDC) reported fiscal Q3 2026 results on April 30, delivering $3.34 billion in revenue against a $3.25 billion consensus estimate, with non-GAAP EPS of $2.72, almost double the $1.38 reported in the same quarter a year ago.

The headline beat does not capture the more important shift.

Gross margin crossed 50% for the first time, landing at 50.5%, a 440 basis point sequential expansion driven by higher-capacity nearline drive mix, UltraSMR technology adoption, and improved pricing across all three end markets.

Cloud represented 89% of revenue at around $3 billion, up 48% year over year, as hyperscalers deepened their dependence on WDC’s nearline HDD portfolio to absorb the data generated by large-scale AI inferencing.

CEO Irving Tan described the compounding demand dynamic on the Q3 2026 earnings call: “Every token, every prompt and every query answered and checkpoint saved creates data that requires persistent, scalable and cost-efficient storage. And the majority of this data is stored on hard disk drives.”

Operating income reached around $1.3 billion, up 116% year over year, translating into a 38.6% operating margin.

Western Digital stock’s free cash flow for the quarter was $978 million, representing a 29% FCF margin, and management returned $752 million to shareholders through buybacks in that same period.

The company ended Q3 with a net positive cash position: $2 billion in cash against only $1.6 billion in remaining convertible debt, a transformation that followed the SanDisk stake monetization that reduced debt by around $3.1 billion in a single quarter.

The board approved a 20% dividend increase to $0.15 per share per quarter, reflecting management confidence in the durability of the free cash flow base.

For Q4, management guided revenue of $3.65 billion at the midpoint, with gross margin expected between 51% and 52%, and EPS guidance of $3.25, implying sequential earnings growth is not slowing.

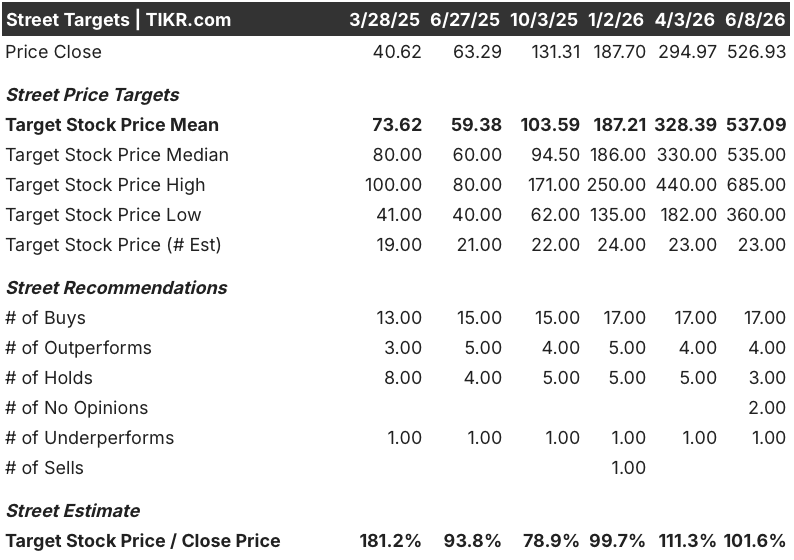

WDC Analyst Consensus Sits at 17 Buys, but the Street Mean Target Has Nearly Closed the Gap to Current Price

The analyst table as of June 8 shows 17 Buys, 4 Outperforms, 3 Holds, and 1 Underperform across 25 analysts, a distribution that reflects high conviction tempered by the stock’s vertical run over the prior 12 months.

The street mean target sits at around $537, barely above the current price of around $527, which looks like a ceiling until the target history puts it in context: the mean was around $328 as recently as April.

The street high target of around $685 represents a potential 30% upside from current levels, anchored to analysts who model the 40-terabyte ePMR volume ramp and HAMR qualification progress through the second half of calendar 2026.

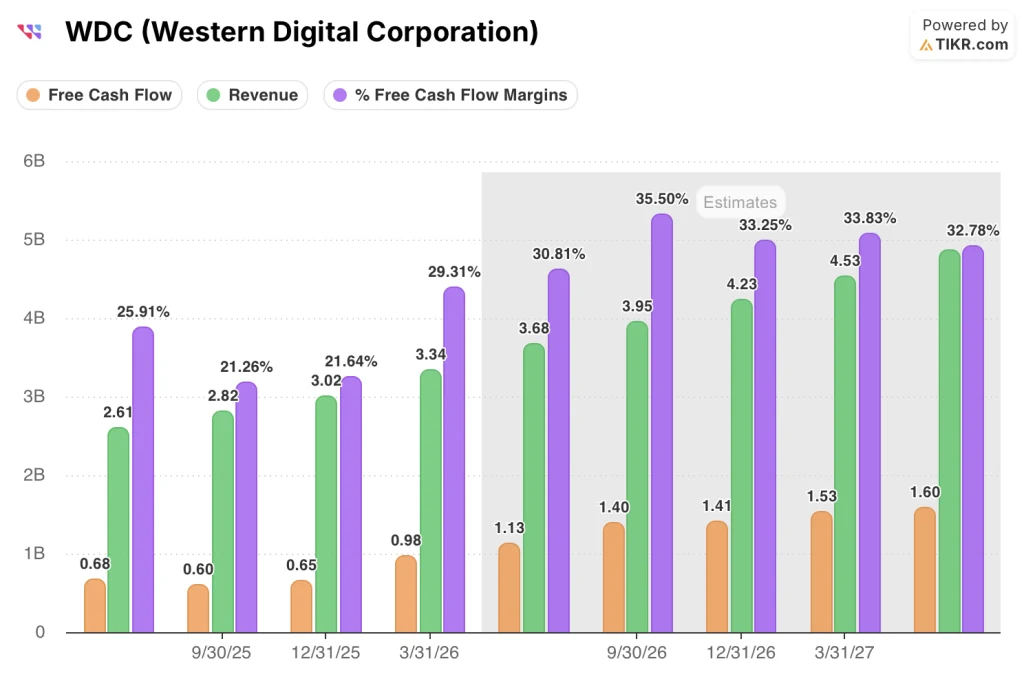

FCF consensus for the June quarter stands at around $1.1 billion, and the forward trajectory extends that further: analysts model FCF of around $1.4 billion in the September quarter and around $1.4 billion in the December quarter, implying a run rate that approaches $5.5 billion annually by the end of fiscal 2027.

Revenue consensus for Q4 2026 sits at around $3.7 billion, growing around 41% year over year, followed by roughly 40% growth in both the September and December quarters.

The exabyte demand picture is what makes the forward estimates credible rather than aspirational. CFO Kris Sennesael stated at the May 5 Barclays conference that long-term exabyte growth expectations have moved beyond 25% CAGR, adding it could be “maybe something trending that starts with a 3” — a demand revision that has not yet been fully absorbed into consensus price targets.

Western Digital stock’s mean target has kept pace with the stock so far this year, but the high target at $685 prices in the scenario the majority of analysts still assign less than full probability. With the FCF margin approaching 30% and LTAs now extending into 2029, the risk the street is pricing is execution risk on the ePMR ramp, not demand risk, and a clean ramp closes that gap quickly.

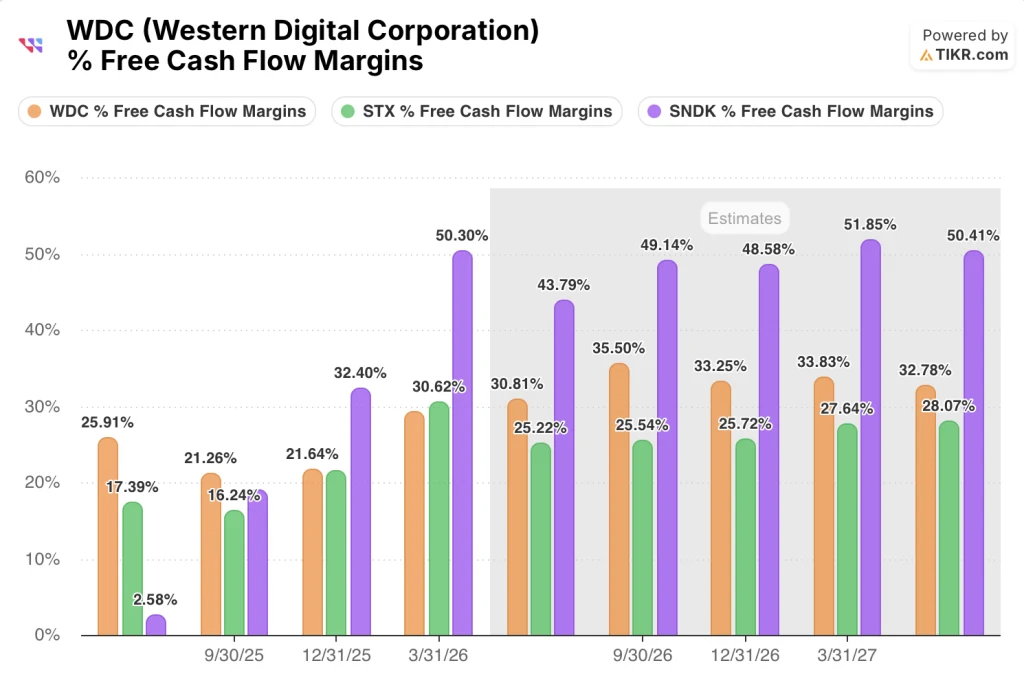

Western Digital Stock Leads Seagate on FCF Margin but Trails SanDisk as All Three Converge on 30%-Plus

Western Digital stock’s 29% free cash flow margin in Q3 puts it ahead of Seagate Technology (STX), which posted 30.62% in the same quarter but is expected to pull back to around 25% in the June quarter as WDC pushes toward around 31%.

SanDisk (SNDK) runs the highest FCF margins in the peer group, hitting 50.30% in Q3 and expected to sustain above 43% through the next several quarters, reflecting the different economics of its NAND flash business versus WDC’s HDD-focused model.

The implication for Western Digital stock is straightforward: at around 31% to 34% FCF margin through fiscal 2027, WDC converts more of its revenue growth into cash than Seagate does, which supports a more aggressive buyback program and a faster path to the dividend growth that management has already demonstrated twice in the past year.

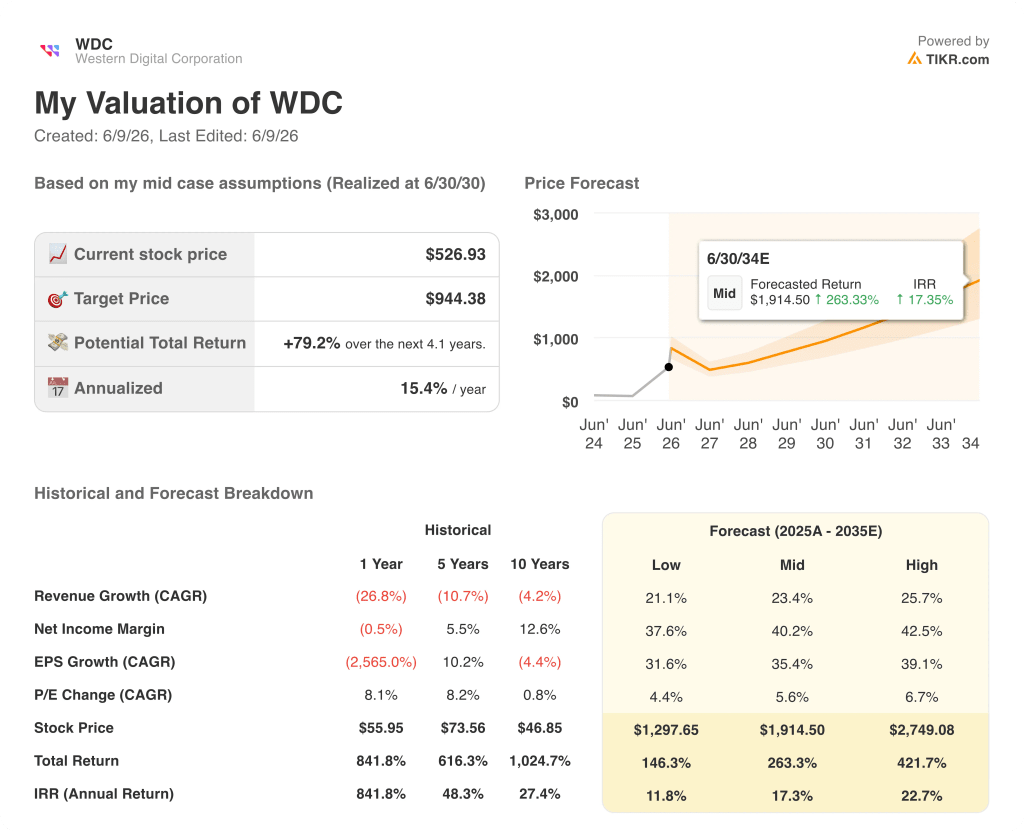

Western Digital Stock Is Undervalued Relative to Its Free Cash Flow Trajectory at Current Analyst Targets

The TIKR model targets $944 for Western Digital stock by June 2030, implying a potential total return of around 79% from the current price of around $527, with an annualized return of around 15% over roughly 4 years.

That target is the mid case. The low case produces around $1,298, and the high case around $2,749, with the spread hinging on revenue CAGR assumptions between roughly 21% and roughly 26% and net income margins expanding toward roughly 43%.

The FCF trajectory is what makes the mid case credible. At a 29% FCF margin in Q3, with management targeting 30% and above, free cash flow is on pace to approach around $1.4 billion per quarter by late fiscal 2027, a compounding rate that makes the buyback program self-sustaining without further debt reduction.

The only real variable is execution: the 40-terabyte ePMR ramp in the second half of calendar 2026, HAMR qualification with four customers ahead of the 2027 ramp, and the modest dilution from the June convertible note exchange that the buyback program is sized to absorb.

At around $527, Western Digital stock is undervalued relative to the FCF compounding path that LTAs through 2029 and greater-than-25% exabyte growth have already locked in.

What is Western Digital stock’s price target?

The street mean target for Western Digital stock (WDC) is around $537 as of June 8, 2026, with 25 analysts covering the name. The street high target is around $685.

The TIKR model mid-case target is around $944, realized over approximately 4 years.

Is Western Digital a good investment in 2026?

Western Digital has delivered three consecutive quarters of revenue growth above 40% year over year, with gross margins crossing 50% and free cash flow approaching a 30% margin.

Long-term exabyte demand from AI training, inferencing, and physical AI is expected to compound above 25% CAGR for the next three to five years.

The key risks are execution on the 40-terabyte ePMR ramp and HAMR qualification timelines.

Should You Invest in Western Digital Corporation?

The only way to know whether WDC is priced right for you is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly this question.

Pull up Western Digital Corporation stock and you will see years of historical financials, what Wall Street analysts project for revenue, EPS, and free cash flow through 2028, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Western Digital Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze WDC stock on TIKR for Free →