Key Stats for Visa Stock

- 52-Week Range: $294 to $376

- Current Price: $320

- Street Mean Target: $399

- Street High Target: $450

- Analyst Consensus: 29 Buy / 7 Outperform / 3 Hold

- TIKR Model Target (Sept. 2030): $614

Visa Stock Just Posted Its Strongest Revenue Growth in 13 Years While Shares Lagged the Market

Visa Inc. (V), the global payments network processing transactions across more than 200 countries and territories, reported fiscal Q2 2026 net revenue of $11.2 billion after its Q2 2026 earnings call, up 17% year-over-year.

CEO Ryan McInerney called it the strongest net revenue growth since 2022 on a nominal basis and, excluding the post-pandemic recovery and the Visa Europe acquisition, the strongest since 2013.

The business runs on volume.

Payments volume reached $3.7 trillion in the quarter, up 9% year-over-year in constant dollars, with processed transactions growing at the same rate to 66 billion.

Cross-border volume, a metric investors watch as a real-time proxy for global trade and travel health, grew 11% in constant dollars excluding intra-Europe, consistent with the prior quarter despite Middle East airspace disruptions cutting into CEMEA travel in March.

The quarter’s outperformance relative to internal expectations came from three sources: higher-than-expected foreign exchange volatility, stronger value-added services revenue, and lower-than-expected client incentives tied to deal timing.

Value-added services, which McInerney positioned as one of Visa’s four structural growth drivers alongside consumer payments, commercial solutions, and blockchain settlement, grew 27% in constant dollars to $3.3 billion and now represent 30% of total net revenue.

Visa Direct processed 3.7 billion transactions in the quarter, up 23% year-over-year, while commercial payments volume grew 11% in constant dollars, the fastest growth rate in the segment in recent quarters.

EPS came in at $3.31, up 20% year-over-year, better than expected, and the board authorized a new $20 billion multi-year share repurchase program on top of the $13 billion remaining from the prior authorization.

The company also raised its full-year net revenue growth guidance to low double-digit to low teens and increased its full-year EPS growth outlook to the low teens.

Analysts Are Unanimously Bullish on Visa Stock and the Gap to Target Is Widening

Visa stock trades around $320 against a Street mean target of around $399, an implied upside of around 25% from current levels, with the high target sitting at around $450.

That distribution, 36 of 39 analysts at a positive rating with zero sells, is about as clean a conviction signal as exists in large-cap coverage.

Consensus estimates project Q3 2026 EPS of $3.44, up around 16% year-over-year, followed by Q4 at $3.61, up around 14%.

For fiscal year 2026, full-year normalized EPS is expected to compound further through fiscal 2027, with quarterly estimates reaching $3.66 and $3.69 in the first two quarters of that year.

Revenue consensus follows the same trajectory: Q3 2026 revenue is estimated at around $12.1 billion, up around 13% year-over-year, with Q4 at around $12.1 billion, up around 11%, pointing to a full-year revenue run-rate well above the $11 billion quarterly threshold Visa crossed for the first time this quarter.

Visa stock currently looks undervalued relative to where that earnings trajectory is heading.

At 29 buys from 39 analysts, the Street is not positioned for disappointment, but the stock sitting 15% below its 52-week high while EPS growth is accelerating suggests the market has priced in geopolitical caution that the actual volume data is not confirming.

JP Morgan called it in a post-earnings note: “There’s a lot to be impressed by in Visa’s print, particularly in the context of investor concerns going in that cross-border growth would dramatically slow in April.”

TD Cowen was equally direct: Visa “posted its strongest growth profile in years supported by multiple self-reinforcing levers while doing well to articulate upside potential from agentic commerce and stablecoins.”

The risk to watch is cross-border travel volume, where Middle East disruptions pushed CEMEA payments volume growth down roughly 2.5 points from Q1 in constant dollars, and where further escalation could suppress the FIFA World Cup-driven inbound traffic baked into H2 guidance.

Visa Stock Carries the Lowest EPS in Its Peer Group for a Reason That Has Nothing to Do With Performance

Visa stock’s normalized EPS of $3.31 in the most recent quarter sits below every peer in the comparison set: Mastercard (MA) at $4.76, Capital One (COF) at $4.57, and American Express (AXP) at $3.99.

That gap does not reflect an earnings deficiency at Visa, it reflects a structural difference in the business model, because both Capital One and American Express carry consumer credit exposure that inflates their per-share earnings while introducing a credit cycle risk that Visa’s network model has never had to price.

Among the pure-network peers, Mastercard runs ahead of Visa stock at $4.76 versus $3.31, a gap that narrows meaningfully when viewed through EPS growth rather than absolute level: Visa’s Q2 EPS grew 20% year-over-year while the forward consensus for Visa stock through the first quarter of 2027 reaches $3.66, compounding at a rate consistent with the mid-teens trajectory management has guided.

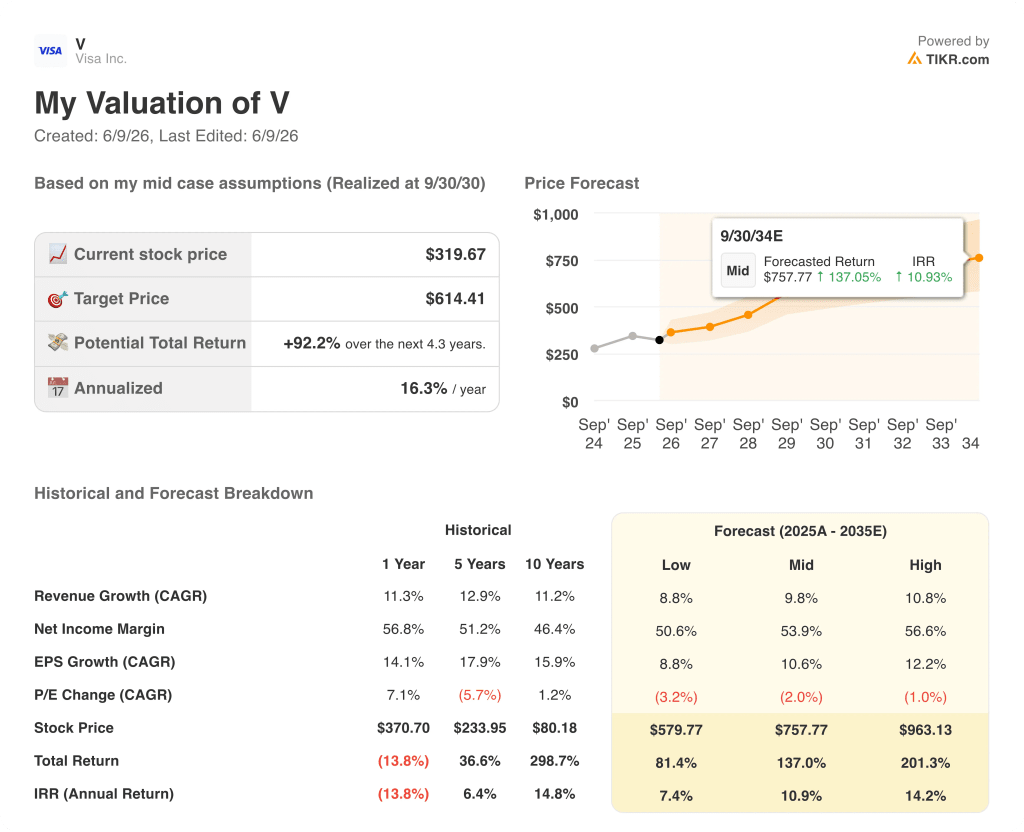

Is Visa Stock Undervalued in 2026? TIKR Model Points to $614 by September 2030

TIKR’s base case values Visa stock at approximately $614 by September 2030, implying around 92% total return from the current price of around $320, or roughly 16% annualized over approximately 4.3 years.

The TIKR model’s mid scenario is built on a revenue CAGR of around 10% from 2025 through 2035, net income margins holding near 54%, and EPS compounding at approximately 11% annually, partially offset by modest multiple compression of around 2% per year.

If revenue growth comes in near the low end of the model’s range, around 9%, with margins around 51%, the stock reaches approximately $580 by September 2030, still an around 81% total return and around 7% annualized.

If Visa captures the agentic commerce, stablecoin settlement expansion, and FIFA-driven commercial volume acceleration that McInerney outlined, with revenue CAGR near 11% and margins near 57%, the model outputs around $963 by September 2030, a total return near 201% and an IRR near 14%.

The base case requires nothing unusual from Visa: the same EPS compounding the network has delivered across its 10-year historical average of around 16% annually, with some multiple contraction assumed.

At around $320 with a TIKR base-case target of around $614, Visa stock is undervalued by any construction of the forward earnings picture the data supports.

What do analysts say about Visa stock?

Thirty-nine analysts cover Visa stock as of June 2026, with 29 Buy ratings, 7 Outperform ratings, and 3 Hold ratings, and zero sell-side downgrade or sell recommendations.

The Street mean price target sits around $399, implying roughly 25% upside from the current price near $320. The high target is around $450.

Consensus EPS estimates project around 16% year-over-year growth in Q3 2026, accelerating from the 20% posted in Q2.

Should You Invest in Visa Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Visa Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Visa Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze V stock on TIKR for Free →