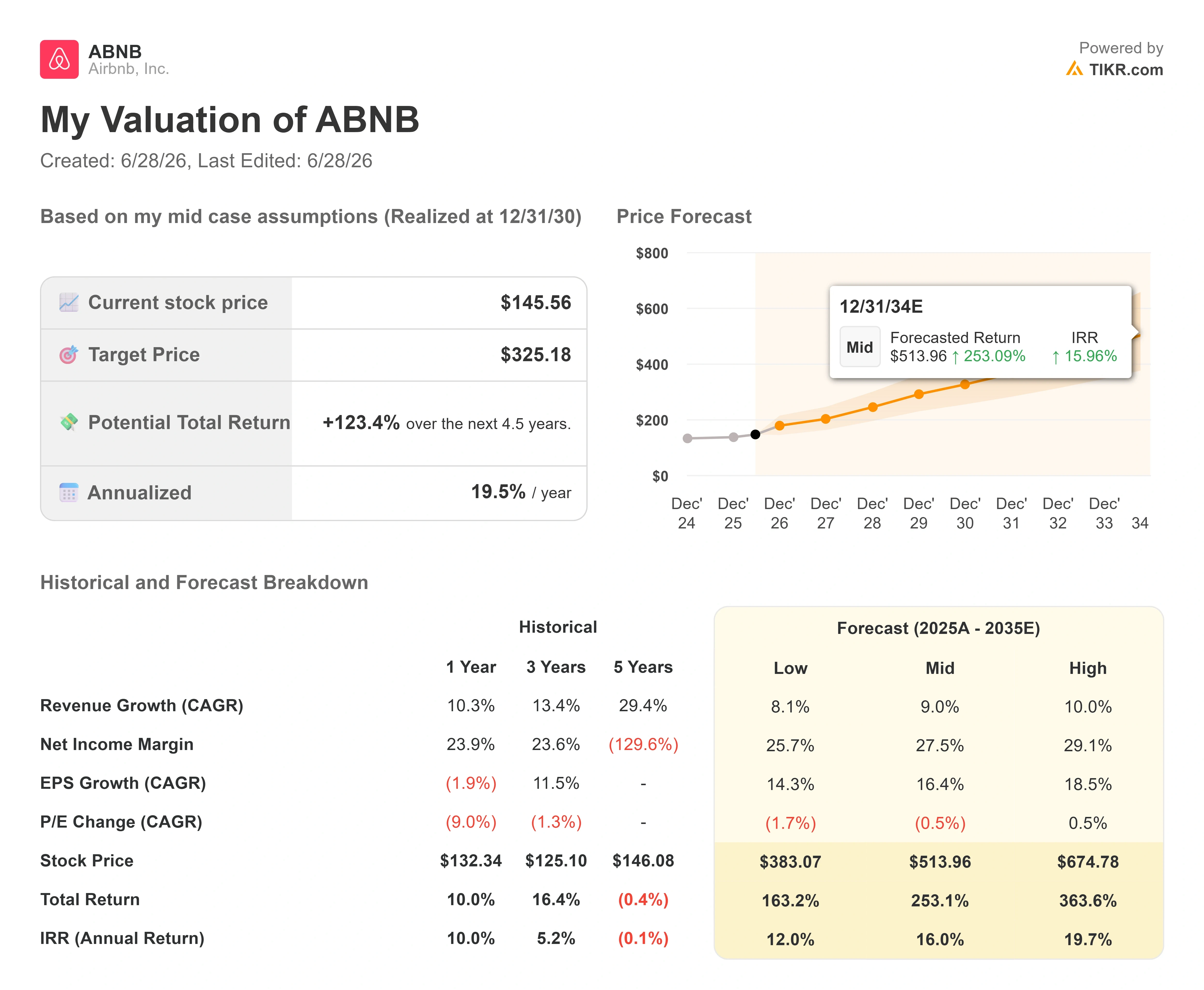

Key Stats for Airbnb Stock

- Current Price: $145.56

- Target Price (Mid): ~$325

- Street Target: ~$156

- Potential Total Return: ~123%

- Annualized IRR: ~20% / year

- Earnings Reaction: 0.73% (May 7, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Airbnb, Inc. (ABNB) spent five years going nowhere, and then in one afternoon, it broke out. On June 24, shares jumped about 5% intraday before closing up 4.2% near $145, the stock’s highest level in more than a year and a push back toward its 52-week high of $147.58. By the June 26 close, ABNB sat at $145.56. The move matters because of what did not cause it. There was no new earnings beat and no product launch. Cheaper oil and falling Treasury yields did the work, and that is the tension the market now has to resolve.

That distinction is the whole story for Airbnb stock in 2026. A breakout built on a strong quarter is a vote on the business. A breakout built on a softer macro backdrop is a vote on rates and travel sentiment, which can reverse just as quickly as they turned. Bulls see a healthy company finally getting permission to re-rate. Bears see a thin, externally driven pop into resistance, with a fresh regulatory headache attached. The question neither side can answer yet is whether this level holds or fades like every other rally near the top of the range.

The macro spark was specific, and it lifted the whole travel sector, not just Airbnb. The 10-year Treasury yield slipped below 4.5% as WTI crude slid about 3% to roughly $70, easing fears about discretionary travel spending. Lower gas prices make road trips and domestic getaways cheaper, and lower rates support the valuation multiples of growth-oriented platforms. According to StockStory’s market coverage, the move was meaningful precisely because ABNB rarely moves this much. The stock has logged only six single-day swings above 5% in the past year, so the market clearly read this as more than noise.

The Business Earned Some of This Before the Macro Helped

Strip out the rates story and the underlying quarter still supports a higher price. In Q1 2026, revenue grew 18% year-over-year to $2.7 billion, clearing the high end of guidance by 2 percentage points. Gross Booking Value, the total value of reservations before cancellations, rose 19% to around $29 billion. Nights and Seats Booked grew 9%, held back by roughly 100 basis points of cancellations tied to the Middle East conflict. Headline EPS of $0.26 actually missed consensus, weighed down by a one-time $70 million tax charge and a deliberate step-up in marketing, which is part of why the stock rose just 0.73% the day after results. The engine, though, is running faster than the share price has rewarded.

CEO Brian Chesky framed the durability of the model directly on the earnings call. “We have millions of homes everywhere in the world at nearly every price point. And that’s something most travel companies can’t replicate,” he said, tying that breadth to consistent results even when travel patterns shift. That matters here because the macro tailwind that lifted the stock on June 24 is the same kind of demand swing Chesky argues Airbnb absorbs better than asset-heavy rivals. The breakout and the thesis point the same direction.

Two product engines back that up. Nights booked on the app grew 22% and now make up 63% of total nights, up from 58% a year ago. Reserve Now, Pay Later, which lets guests book now and pay closer to the stay, drove about 20% of global GBV after expanding to most of the world in Q1. First-time bookers grew 10%, the fastest pace since 2022. Management estimates its three newest features added roughly 3 points of nights growth and 4 points of GBV growth in the quarter. These are platform features now, not one-time promotions, which is why guidance shows acceleration rather than a post-launch fade.

See historical and forward estimates for Airbnb stock (It’s free!) >>>

Hotels Are the Quiet Top-of-Funnel Machine

The most underappreciated line in the quarter was hotels. CFO Ellie Mertz said hotels are still a single-digit percentage of nights but growing at more than double the rate of the overall business. The reason Airbnb cares is conversion, not just inventory. “Over 55% of people who book a hotel on the platform come back to book a home,” Mertz said. That reframes hotels as an onboarding ramp for the core homes business, a way to pull in travelers who would never have started with an Airbnb stay. Chesky compared the broader strategy to Amazon’s move from books into everything, where each new category gets cheaper to add because the next service is only marginally different from the last.

The World Cup gives that strategy a stage this summer. Mertz said it is slated to be the largest event in Airbnb’s history, spanning 16 cities across three countries, and that over 100,000 homes have listed for the first time since outreach began. Using the Paris Olympics as a guide, Airbnb retained more than half of event-driven listings six months later, so the supply bump is partly permanent. For a model with free cash flow margins near 37% and no inventory to carry, every retained host drops almost entirely to gross profit.

The Bear Case Did Not Disappear With the Breakout

The same week the stock broke out, the City of Chicago sued Airbnb. On June 23, the city filed a complaint in Cook County alleging Airbnb processed bookings for unregistered and unlicensed units tied to a high-volume host cited nearly 200 times in 2024 and 2025. The city is seeking fines, disgorgement of profits, and an injunction. Per the City of Chicago’s official release, the case targets one host and one platform, so the immediate financial exposure looks small. The longer-term risk is precedent, since a win for Chicago could embolden other large cities where regulation already constrains supply.

The core growth picture has its own soft spots. Nights and Seats Booked growth of 9% in Q1 decelerated from prior years, and management guided Q2 slightly lower on another estimated 100-basis-point conflict headwind. On valuation, ABNB is not cheap on a relative basis. Its NTM EV/EBITDA of around 15x sits above Booking Holdings at around 13x and Trip.com at around 7x, though below asset-heavy operators Marriott at around 19x and Hilton at around 21x. The premium to Booking is the crux of the debate. Bulls argue it is fair for a business compounding faster, converting more revenue to cash, and carrying around $9.5 billion in net cash versus Booking’s net debt. Bears argue a premium multiple plus a macro-driven breakout plus fresh regulatory noise is a fragile setup near the top of the range. The analyst community leans constructive but split: 19 buys, 4 outperforms, 18 holds, 0 underperforms, and 2 sells, with a mean target around $156, roughly 8% above the current price.

See how Airbnb performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $145.56

- Target Price (Mid): ~$325

- Potential Total Return: ~123%

- Annualized IRR: ~20% / year

See analysts’ growth forecasts and price targets for Airbnb stock (It’s free!) >>>

Using TIKR’s mid-case scenario, realized at 12/31/30, the model targets around $325 for ABNB, implying around 123% total return and roughly a 20% annualized IRR over the next 4.5 years. The case rests on two revenue CAGR drivers: continued nights growth from app adoption and international expansion, and take-rate expansion from the simplified single fee structure and the insurance program. The margin driver is operating leverage on an 83% gross-margin model, where AI-led cost savings (cost per booking fell about 10% year-over-year) and roughly 60% of code is now AI-authored, letting the company scale features without scaling headcount.

The mid case assumes around 9% revenue growth and a net income margin climbing toward 27.5% by 2030.

The upside: if hotels, experiences, and a future loyalty or flights offering compound the way the Amazon-style ecosystem implies, the high case points to around $675 by the mid-2030s.

The downside: the primary risk is regulation, where a wave of city-level enforcement like Chicago’s could compress supply in dense urban markets and slow the night’s growth, the entire model depends on.

Conclusion

The breakout is real, but it is on probation. The cleanest test arrives with Q2 earnings, which historical timing suggests should land in early-to-mid August. Watch Nights and Seats Booked growth: management guided to a slight deceleration from 9%, so anything that holds near 9% or better confirms the macro tailwind is being backed by real demand, while a drop toward the mid-single digits would suggest June’s pop was borrowed from rates rather than bookings. The second thing to watch is the World Cup read-through in the same report, since this is the largest event in company history and the first hard proof of whether the supply-and-conversion playbook scales. If both land, the five-year sideways chart finally has a reason to break. If they miss, the $147 area becomes the ceiling it has been before.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Airbnb?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Airbnb, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Airbnb alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!