Key Stats for Adobe Stock

- Today’s Performance: -7%

- 52-Week Range: $197 to $405

- Valuation Model Target Price: $317

- Implied Upside: 56%

Analyze your favorite stocks like Adobe Inc. with TIKR (It’s free) >>>

What Happened?

Adobe Inc. stock fell about 7% today, trading near $204 per share as investors reacted to the company’s fiscal Q2 report, CFO transition, and concerns that its AI strategy may pressure near-term recurring revenue before it creates stronger long-term growth.

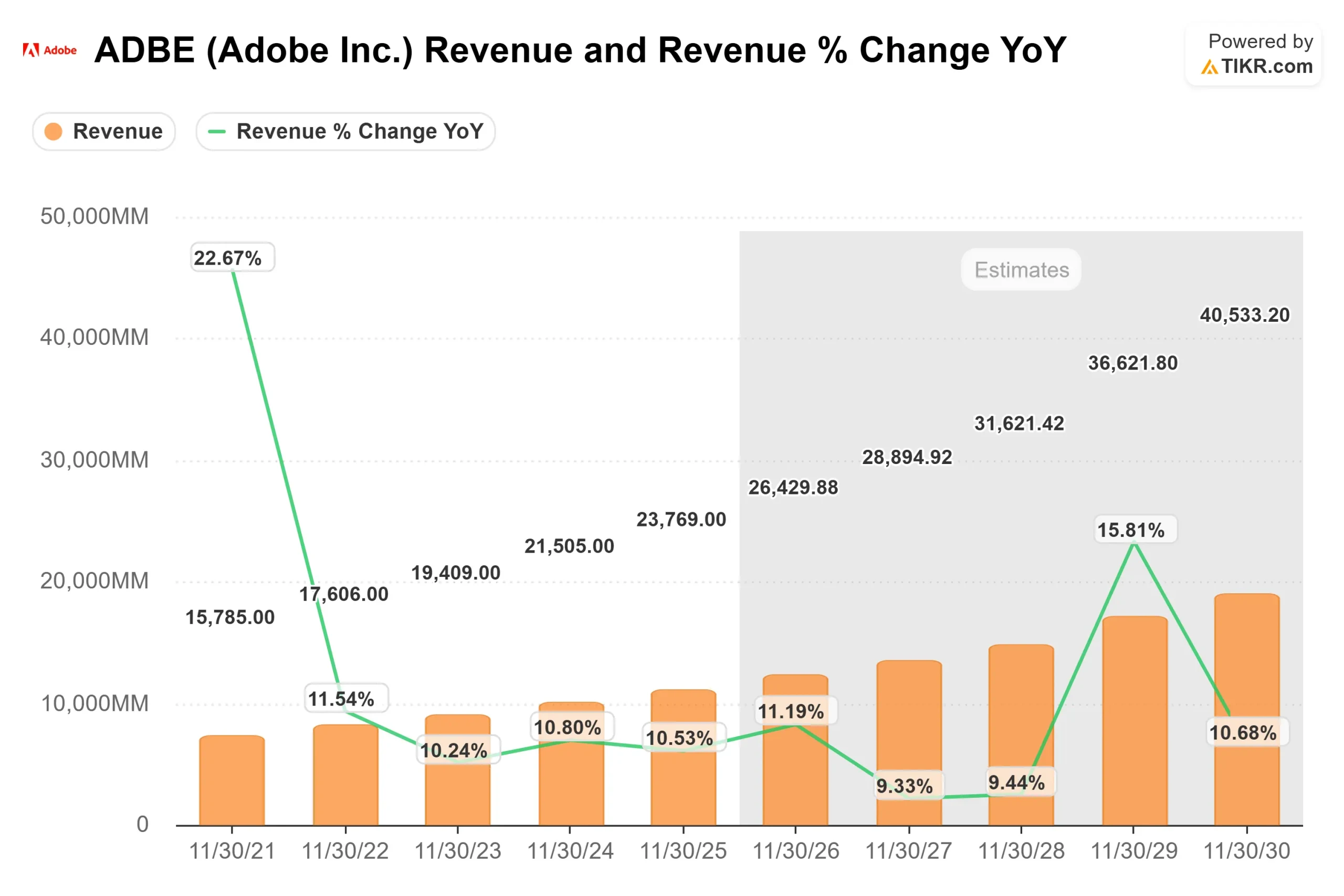

The stock moved lower because Adobe’s strong earnings were overshadowed by three specific concerns: its bigger push into freemium AI products, delayed Creative Cloud pricing actions, and weaker second-half annual recurring revenue expectations from individual subscribers. Adobe reported record Q2 revenue of $6.62 billion, up 13% year over year as reported, with GAAP EPS of $4.25 and non-GAAP EPS of $5.96, while management raised fiscal 2026 guidance to $26.5 billion to $26.6 billion in revenue and $24.35 to $24.45 in non-GAAP EPS.

This week, on Adobe’s fiscal Q2 earnings call, management said AI-first annual recurring revenue rose 3x year over year to more than $500 million, total Adobe ending ARR reached $27.1 billion, and Semrush added about $480 million of ARR after the acquisition closed. CEO Shantanu Narayen said “now is the time to aggressively acquire the next generation of Adobe loyalists,” highlighting Adobe’s push into freemium funnels across Acrobat, Express, and Firefly even as that strategy weighs on near-term ARR visibility.

The competitive backdrop also made the selloff sharper. Adobe is defending Creative Cloud, its core design software suite, against AI-native and lower-friction rivals such as Canva, Figma, Microsoft Designer, and OpenAI’s image-generation tools. Canva has scaled to more than 265 million monthly active users and about $4 billion in annual recurring revenue, which shows why investors are watching whether Adobe can keep creators inside its ecosystem as AI makes design tools easier to access.

Analyst actions added pressure, with RBC lowering its price target to $285 from $350, TD Cowen cutting its target to $245 from $285, Stifel downgrading Adobe to Hold from Buy and lowering its target to $200 from $350, and KeyBanc lowering its target to $195 from $235. Recent fourth-quarter filing updates showed some institutional support, including Fieldview Capital Management opening a new Adobe position worth about $4 million and Clear Street Group raising its stake to about 111,000 shares worth about $39 million, though those filings are backward-looking and were not the main driver of today’s selloff.

Value Adobe Inc. instantly (Free with TIKR) >>>

Is Adobe Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): around 9%

- Operating Margins: around 45%

- Exit P/E Multiple: around 10x

Adobe’s 9% revenue growth assumption is not built on a sudden AI boom. It assumes steady expansion across Creative Cloud, Document Cloud, and Experience Cloud, with AI helping engagement and paid conversion rather than completely changing the company’s growth rate overnight.

Creative Cloud is Adobe’s core design software suite, Document Cloud includes Acrobat and PDF workflows, and Experience Cloud helps enterprises manage marketing, customer data, and digital campaigns.

See analysts’ growth forecasts and price targets for Adobe Inc. (It’s free) >>>

The key upside driver is AI monetization. Firefly is Adobe’s generative AI tool for creating images, videos, and other content, Acrobat AI Assistant helps users summarize and work with PDFs, Express is Adobe’s easy-to-use design app, and GenStudio helps companies create and manage marketing content at scale.

Semrush also gives Adobe a deeper marketing software angle by adding search, content, and brand visibility data into Experience Cloud, which could make the platform more valuable for companies managing digital campaigns across search, AI assistants, and social channels.

The 45% operating margin assumption looks defensible because Adobe still has a high-margin subscription software model, but margin quality depends on whether higher AI infrastructure and product investment can be offset by stronger paid conversion and enterprise spending.

Based on these inputs, the model estimates a target price of $317, implying about 56% total upside, suggesting Adobe appears undervalued if AI products, enterprise demand, and the Semrush integration translate into durable paid growth.

How Much Upside Does Adobe Stock Have From Here?

Investors can estimate Adobe’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Adobe Inc. in under 60 seconds with TIKR (It’s free) >>>