Key Stats for Accenture Stock

- Past-Week Performance: -8.5%

- 52-Week Range: $188.7 to $326.7

- Current Price: $196.7

What Happened?

Accenture (ACN), the global IT services and consulting firm racing to become the dominant enterprise AI integrator, booked $2.2 billion in advanced AI work in a single quarter, nearly doubling the prior year, while the stock sits 39% below its 52-week high at $198.87.

The trigger was Q1 FY2026 earnings reported last December, where revenue of $18.7 billion hit the top of guidance, adjusted EPS grew 10% to $3.94, and bookings of $20.9 billion including 33 clients each committing more than $100 million in a single quarter confirmed the demand thesis.

Advanced AI revenue, which Accenture defines as revenue from GenAI, Agentic AI and Physical AI deployments directly embedded in client operations, crossed $1.1 billion in a single quarter for the first time, and cumulative bookings across 11,000 projects reached $11.5 billion since the metric launched in 2023.

Just today, Accenture completed its acquisition of Faculty, a UK-based AI firm, with Faculty CEO Marc Warner immediately appointed as Accenture’s Chief Technology Officer and over 400 AI professionals joining the company, adding Faculty’s enterprise decision intelligence platform Frontier to Accenture’s product suite.

Julie Sweet, Chair and Chief Executive Officer, stated on the Q1 FY2026 earnings call that “advanced AI is increasingly embedded in our large transformation programs, either enabling future enterprise use or being implemented directly as part of our solutions,” a claim now backed by the $1.2 billion Ookla acquisition closed March 3 for network intelligence capabilities.

A $3 billion acquisition budget for FY2026, at least $9.3 billion in planned capital returns, a Reinvention Services organizational restructure taking effect March 31, and Q2 FY2026 earnings scheduled March 19 together build a multi-catalyst runway for a business guiding 5%–8% adjusted EPS growth as enterprise AI adoption remains, by management’s own account, still in early innings.

Wall Street’s Take on ACN Stock

The $2.2 billion advanced AI bookings quarter, nearly doubling year-over-year, directly underpins FY2026 revenue guidance of 2%–5% local currency growth and TIKR’s FY2027 consensus estimate of $78 billion, as bookings typically convert to revenue over 2–4 quarters.

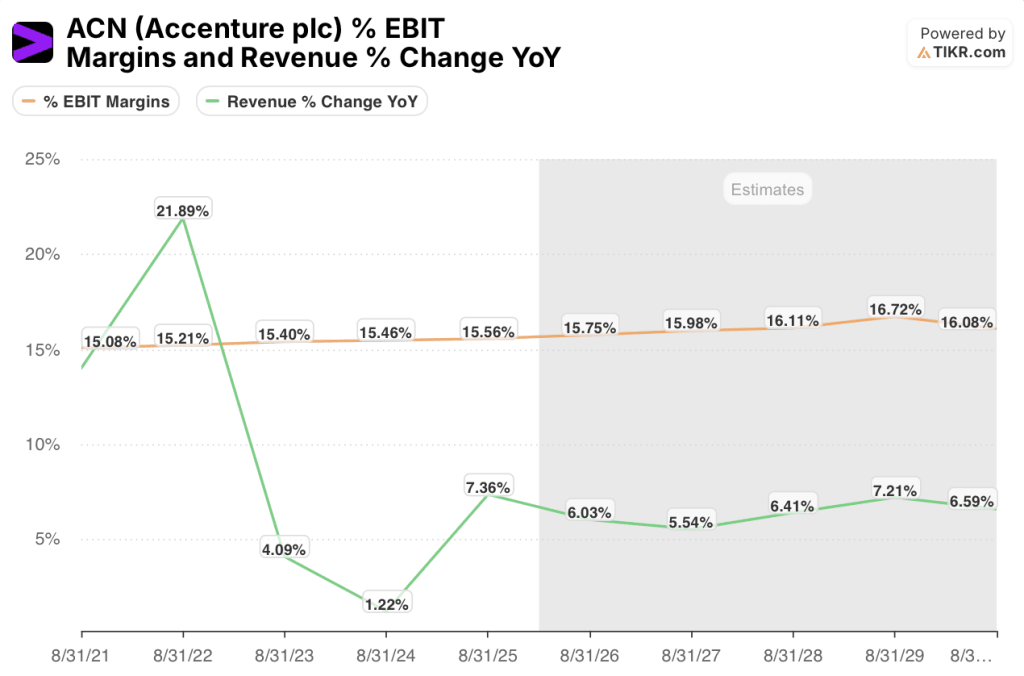

TIKR consensus projects Accenture’s EBIT margin to expand from 15.6% in FY25 to 15.8% in FY26 and 16.0% in FY27, supported by the talent rotation strategy that already delivered 7% revenue-per-person growth in Q1.

Wall Street is constructively positioned but not euphoric: 14 buys, 4 outperforms, 9 holds, and 1 sell among 27 analysts, with a mean price target of $280.22 implying 42.5% upside from $196.65, suggesting analysts see the AI demand inflection but are waiting for revenue acceleration to show up more visibly in reported results.

The analyst target range spans $210 to $330, and the distance between those poles maps directly to the two outcomes already seeded in the story: full-scale enterprise AI adoption converting the $11.5 billion in cumulative advanced AI bookings into accelerating revenue justifies the high end, while prolonged discretionary spending weakness and federal headwinds justify the low.

What Does the Valuation Model Say?

TIKR’s mid-case model prices ACN at $312.04 by August 2030, a 58.7% total return at 10.9% annualized IRR, anchored to 5.6% revenue CAGR and net income margins expanding from 11.7% in FY25 toward 12.0% by the forecast period, justified by the Reinvention Services reorganization, the Faculty and Ookla acquisitions, and the $3 billion annual M&A budget compounding specialist AI capabilities.

The market is treating Accenture as a slowing IT services firm, but 33 clients booking more than $100 million each in a single quarter contradicts that framing entirely.

TIKR’s $312.04 target requires Accenture to sustain 5.6% revenue CAGR, a rate already supported by $20.9 billion in Q1 bookings and the Reinvention Services structure taking effect March 31.

Managed services bookings, the long-term recurring revenue contracts that provide earnings visibility, hit $11.1 billion in Q1 with a book-to-bill of 1.2, a ratio above 1.0 signaling the pipeline is growing faster than revenue, confirming the model’s durability assumption.

If enterprise AI adoption stalls at the proof-of-concept stage and clients delay full-scale transformation programs, the advanced AI bookings pipeline stops converting, EBIT margin expansion reverses, and TIKR’s $312.04 mid-case target becomes unreachable.

March 19 Q2 FY2026 earnings deliver the first read on whether the Reinvention Services reorganization and Faculty integration are translating into accelerating managed services bookings; watch the book-to-bill ratio against Q1’s 1.2.

Should You Invest in Accenture plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ACN stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Accenture plc alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ACN stock on TIKR for Free →