Xylem Inc. (NYSE: XYL) trades near $141/share after a steady multi year run supported by strong demand for water infrastructure and consistent earnings growth. The company continues to benefit from long duration projects in utilities and industrial markets, which has helped support premium margins and a healthy balance sheet.

Recently, Xylem delivered strong multi year momentum, including rapid improvements in revenue, EBITDA and earnings. The company has also expanded deeper into advanced analytics and smart water technology, creating new opportunities for recurring revenue and efficiency driven solutions. These developments reinforce Xylem’s position as a leader in modern water infrastructure at a time when global demand is accelerating.

This article explores where Wall Street analysts believe Xylem could trade by 2027. We have compiled consensus price targets and TIKR’s Guided Valuation Model to outline the stock’s potential return path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

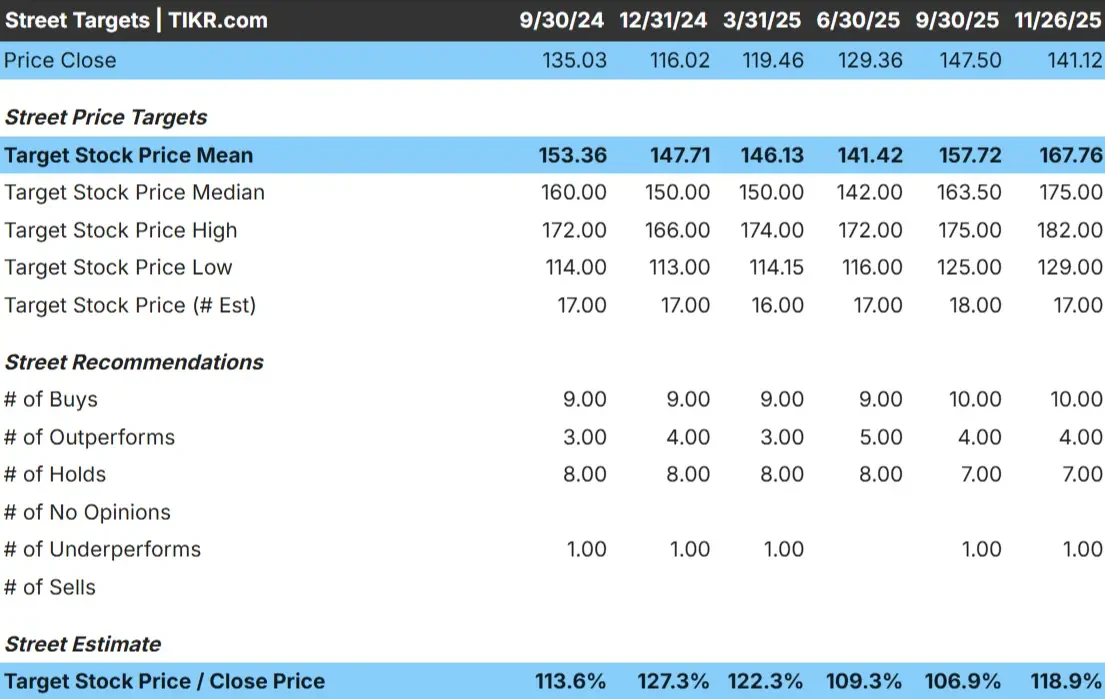

Xylem trades near $141/share, and the latest analyst targets point to about $168/share, which represents roughly 19% upside. This places the stock in the modest upside category, where expectations are positive but not aggressive.

From the analyst target grid:

- High estimate: $182/share

- Low estimate: $129/share

- Median target: $175/share

- Ratings: 10 Buys, 4 Outperforms, 7 Holds, 1 Underperform

Analysts see room for continued gains, but the spread between the high and low targets suggests a balanced outlook. For investors, this means Xylem’s future returns will likely depend on steady earnings growth rather than dramatic sentiment driven moves. The stock may outperform if margins strengthen or if demand for water infrastructure accelerates.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Xylem Growth Outlook and Valuation

The company’s fundamentals appear solid based on the valuation inputs shown in the model:

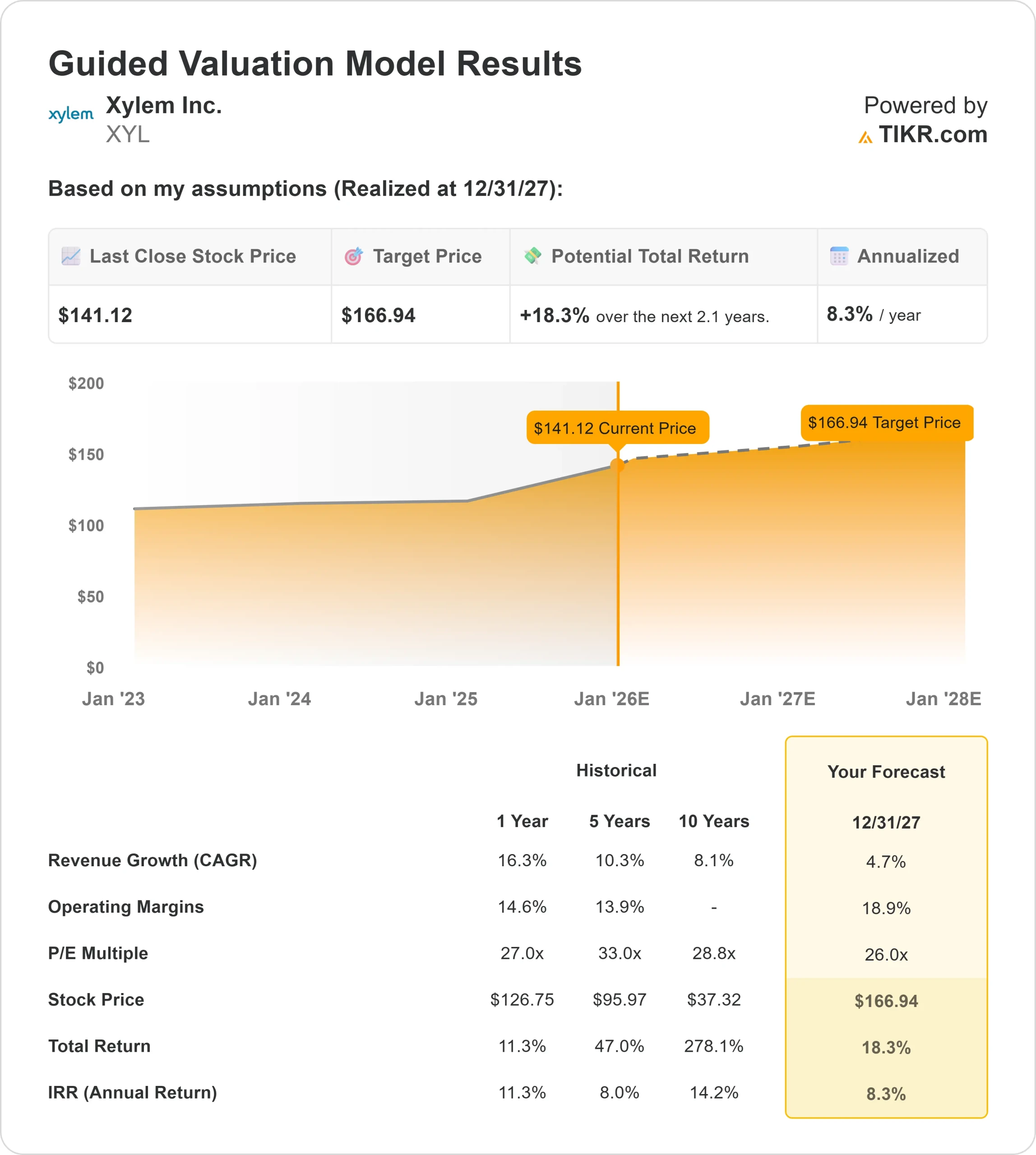

- Revenue is projected to grow about 4.7% through 2027

- Operating margins are expected to reach roughly 18.9%

- The model is based on a 26x forward P E

- Based on analysts average estimates, TIKR’s Guided Valuation Model using a 26x forward P E suggests Xylem could trade near $167/share by 2027

- That implies roughly 18.3% total return and about 8.3% annualized gains

These numbers point to a return profile driven by consistent earnings and stable margins rather than rapid acceleration. Xylem appears positioned for steady mid single digit compounding supported by durable industry demand and a strong competitive foundation. The outlook is constructive, but meaningful upside would likely require faster revenue growth or stronger operating leverage.

For investors, Xylem looks more like a dependable, high quality operator than a fast growth opportunity. Returns will come from steady execution, healthy margins and infrastructure driven demand unless the company can unlock a higher growth trajectory in its digital and smart water solutions.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Xylem benefits from several long term structural trends. Global utilities are modernizing aging water systems, and demand is rising for smart monitoring, leak detection and digital infrastructure. These solutions help customers improve efficiency and reduce waste, which strengthens Xylem’s value proposition.

The company is also positioned well thanks to strong execution and disciplined capital allocation. Its technology portfolio continues to expand, and management maintains a focus on innovation, customer relationships and long term adoption of advanced solutions. For investors, these strengths support a stable growth path and reinforce confidence in Xylem’s ability to deliver durable performance.

Bear Case: Valuation and Cyclicality

Even with its strengths, Xylem trades at a premium valuation relative to typical industrial companies. If growth slows or margins come under pressure, the stock could face limited upside in the near term. The company’s valuation leaves little room for missteps.

Water infrastructure spending can also vary with municipal budgets and economic cycles. Project delays or reduced funding could create temporary softness in demand. For investors, the key risk is that Xylem may continue to perform well operationally while the stock delivers only moderate returns due to valuation pressure.

Outlook for 2027: What Could Xylem Be Worth?

Based on analysts average estimates, TIKR’s Guided Valuation Model using a 26x forward P E suggests Xylem could trade near $167/share by 2027. That implies an 18% total return, or roughly 8% per year, from today’s price of about $141/share.

This outlook reflects a path of steady compounding rather than rapid acceleration. It assumes Xylem maintains strong margins, executes well across its portfolio and benefits from ongoing investment in global water infrastructure. For investors, the stock appears positioned to deliver dependable long term performance with a clear path to moderate gains.

Unlocking higher returns would likely require faster adoption of Xylem’s digital solutions, improved pricing power or a meaningful increase in infrastructure spending.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>