Key Stats for Waste Management Stock

- 52-Week Range: $194.11 to $248.13

- Current Price: $217.92

- Street Mean Target: $256.04

- LTM Gross Margin: 40.6%

- LTM EBIT Margin: 18.7%

- LTM Net Debt (MM): $22.73 billion

Value your favorite stocks like WM with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

Why Sentiment and Momentum Blind the Market

Waste Management, Inc. (WM) has felt the squeeze of a cyclical consolidation window, with its stock experiencing a minor negative 6.6% price return over the past year to trade at $217.92. The market’s near-term anxiety is heavily tied to temporary industrial volume optimizations and sticky municipal contract labor costs.

This short-term underperformance has led momentum allocators to look elsewhere, mistaking a routine macroeconomic leveling period for a structural operational breakdown.

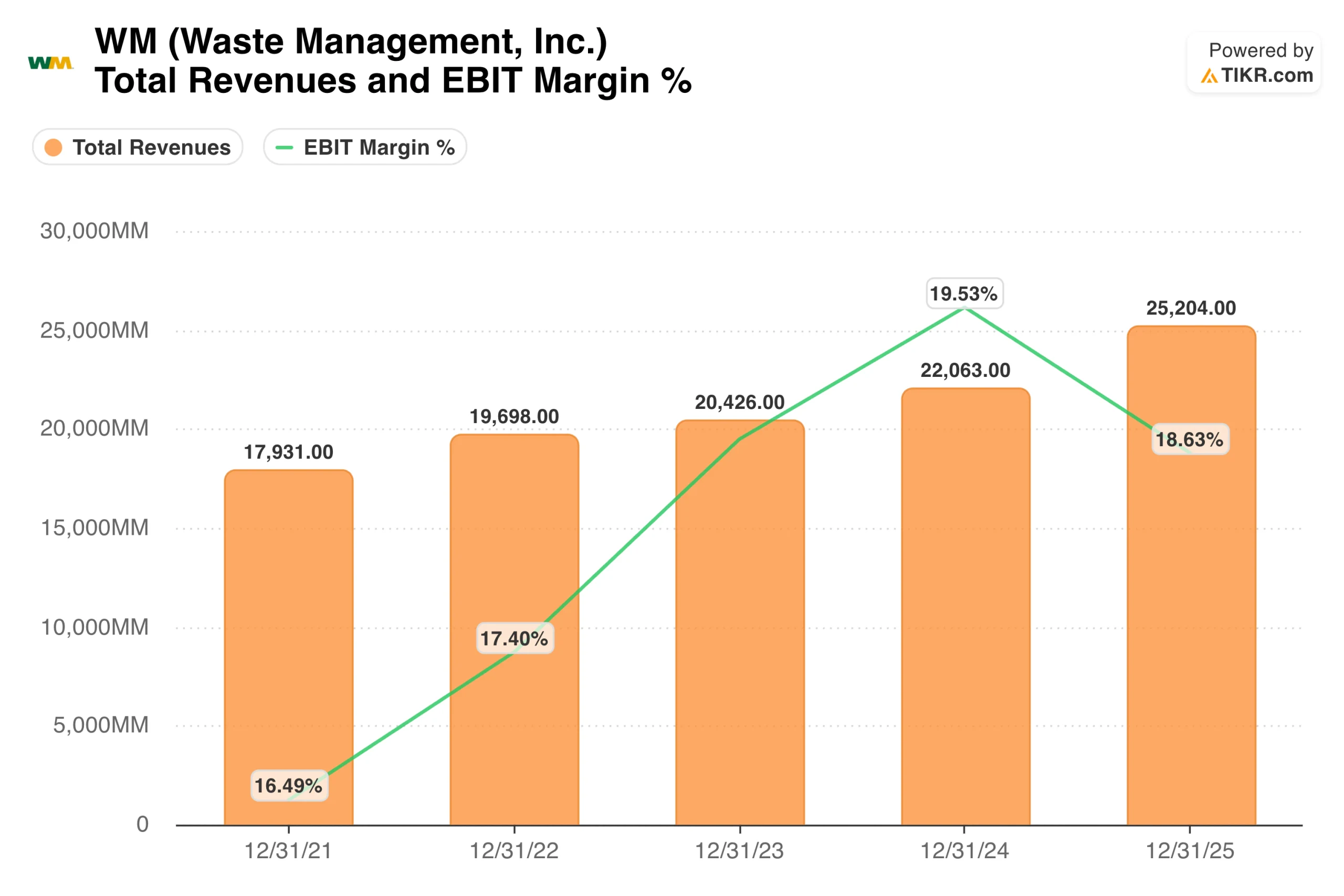

Wall Street’s persistent focus on immediate volumetric expansion metrics creates an exceptional entry window for patient, long-term allocators. Total revenues scaled upward sequentially from $17.93 billion in 2021 to an impressive $25.20 billion in late 2025.

However, aggressive investments in recycling automation and energy transition technology compressed absolute EBIT margins from a 2024 high of 19.53% down to 18.63%. Without a real logistical alternative to WM’s disposal infrastructure, market sentiment remains overly sensitive to temporary price-cost spreads.

See historical and forward estimates for WM stock (It’s free!) >>>

How Capital Outlays and Infrastructure Builds Press the Capital Base

This minor operational margin shift represents an intentional, forward-looking capital deployment cycle rather than a destruction of corporate value. Management directed a substantial $3.22 billion into growth-oriented capital expenditures during the late 2025 operating period.

Because these multi-million-dollar outlays upgrade internal automation frameworks, they actively position the company to reduce its reliance on volatile manual municipal labor markets over the next decade.

The cash conversion efficiency of this layout is showcased by the underlying trend in capital returns. Annual free cash flow expanded significantly to a record $2.81 billion in late 2025, proving the self-funding nature of the asset base.

This exceptional liquidity optimization ensures that WM can comfortably service its heavy $22.73 billion net debt load without diluting its basic share count of 401.58 million outstanding shares.

See what analysts think about WM stock right now (Free with TIKR) >>>

The Efficiency Flywheel: Asset-Heavy Monopolization

The central corporate reality within Waste Management’s business model resides in its immense capital expenditure requirement versus its highly efficient return profile. At first glance, deploying billions of dollars into landfills and heavy collection truck fleets appears like a capital-intensive drag that should suppress equity performance.

However, these immense infrastructure investments serve as an unbreachable geographic moat that keeps competitors entirely out of the regional ecosystem.

This capital layout grants WM exceptional pricing power across its collection routes and landfill networks. By indexing tipping fees directly to underlying inflationary markers, management passes driver wage and fleet maintenance volatility straight onto its captive municipal client base.

The resulting cash engine easily sustains an elite 13.2% Return on Invested Capital (ROIC) and supports a balanced 49.5% dividend payout ratio. As automated route optimizations continue to scale, incremental processing revenue drops directly to the bottom line as pure operational leverage.

Unlocking Value: What the TIKR Forecast Breakdown Implies

Moving past trailing operational periods, the forward valuation architecture isolates a remarkably resilient terminal value progression for capital allocators. Reviewing the historical 1-year total return drop of 8.5% against the stellar 10-year return of 256.6% underscores exactly why short-term market friction is misleading.

While net income margins are modeled to stabilize at 14.3% in the mid-case scenario, the underlying predictability of asset utilization protects the investment from major earnings shocks.

These stable performance parameters yield a structurally tight distribution of forward return probabilities. The automated model proves that even if top-line revenue growth triggers down to a conservative low-case footprint of 4.8%, the cash generation capabilities remain robust enough to establish a $398.67 stock price floor.

By insulating real corporate yields from competitive disruptions, the underlying forecast framework transforms a low-growth utility narrative into a reliable compounding machine that targets a $494.06 stock price by 2034.

Is WM Worth Buying at $217.92?

At the current price of $217.92, the TIKR forward valuation model establishes a highly defensive, predictable entry point for long-term equity allocators. Under a mid-case forecast scenario, realizing a fair value price target of $363.10 by December 2030 generates a reliable 11.7% annualized internal rate of return (IRR).

This baseline scenario operates on an organic revenue growth CAGR of 5.4% and assumes net income margins normalize at 14.3%.

Crucially, the conservative low-case adjustments show immense downside protection, projecting a 7.3% annual return ($398.67 over the model horizon) even if revenue expansion slows to 4.8%. This tight forecast variance demonstrates an exceptional fundamental margin of safety that requires zero speculative multiple expansion to build equity value.

For disciplined, risk-conscious investors looking to capture a durable monopoly asset backed by a growing 1.7% dividend yield, initiating a position at today’s price is a phenomenal defensive move.

See analysts’ growth forecasts and price targets for WM stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!