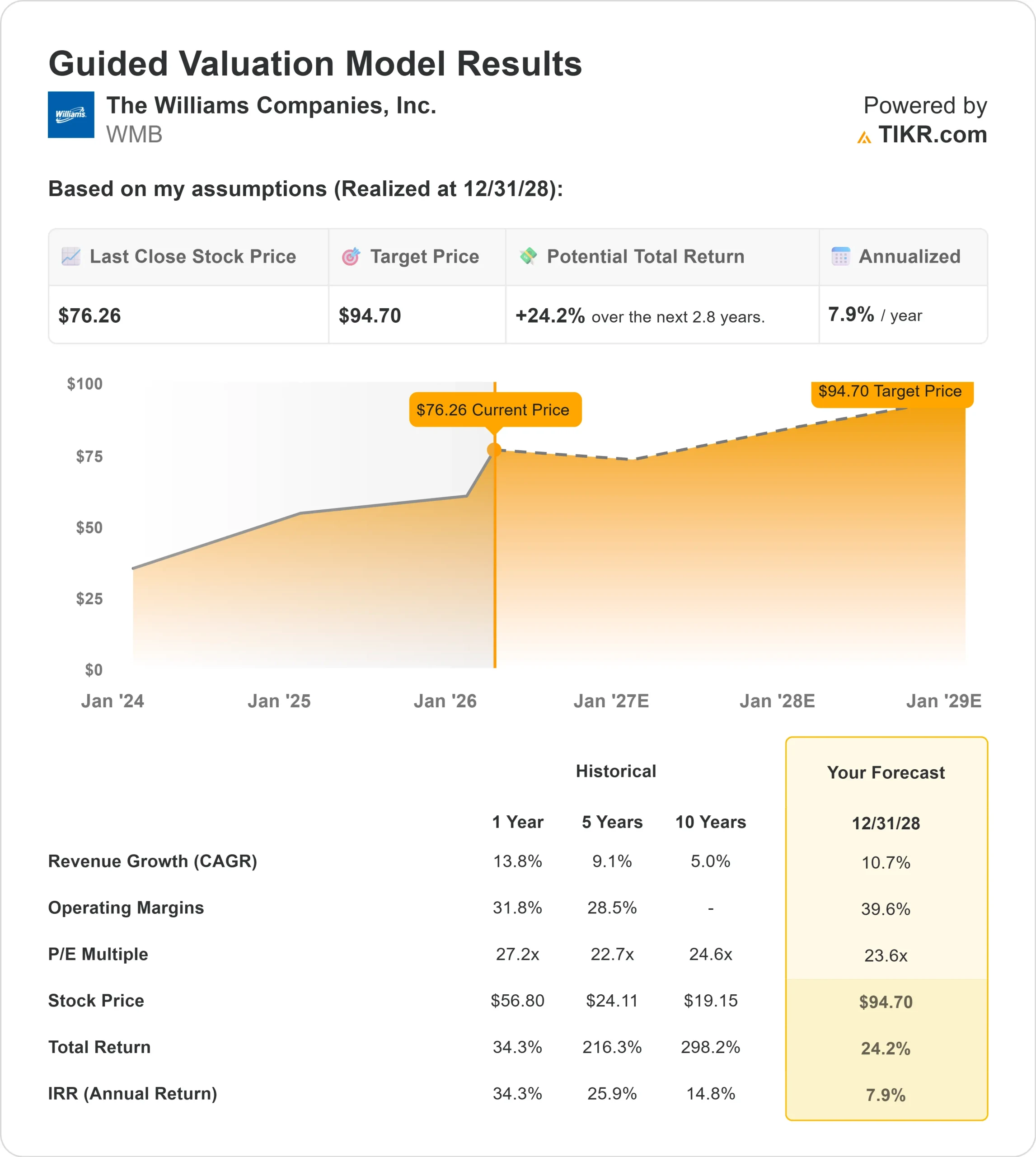

Key Stats for WMB Stock

- Past 6-Month Performance: 31%

- 52-Week Range: $52 to $77

- Valuation Model Target Price: $95

- Implied Upside: 24%

Value your favorite stocks like WMB with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Williams Companies stock climbed about 31% over the last 6 months, rising to around $76 per share as investors responded to accelerating power demand tailwinds and a sharply improved long-term growth outlook.

Shares have pushed toward the upper end of their $52 to $77 52 week range, reflecting sustained institutional accumulation rather than a short-lived bounce.

The rally was driven primarily by the company’s Analyst Day update, where management raised its long-term adjusted EBITDA growth target to more than 10% annually through 2030 and reinforced visibility into contracted expansion projects.

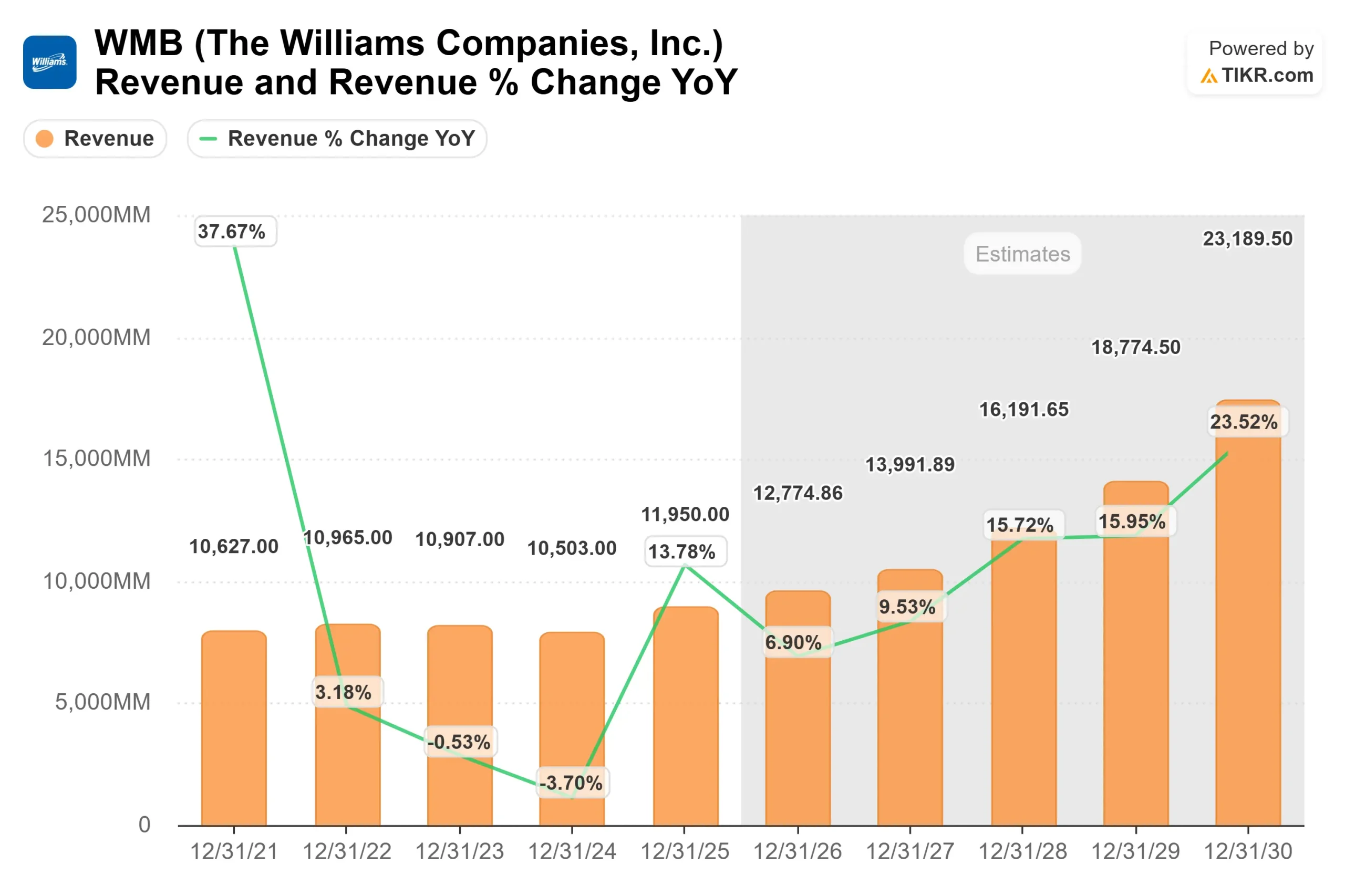

Williams reported record 2025 adjusted EBITDA of $7.75 billion, up 9% year over year and marking its 13th consecutive year of EBITDA growth.

Management guided to 2026 adjusted EBITDA of $8.2 billion at the midpoint with 9% EPS growth, signaling continued earnings acceleration into next year.

Institutional positioning added fuel to the move. Brookfield increased its stake by 190% to 12.0 million shares, Norges Bank initiated a new position worth about $765 million, American Century Companies raised its holdings by 12.2% to 6,782,278 shares valued near $429.7 million, and Mitsubishi UFJ Asset Management lifted its stake to 2,706,923 shares.

While some firms trimmed exposure, including APG Asset Management cutting 3.2% and Artisan Partners reducing 10.2%, overall institutional ownership stands near 86.44%, indicating broad conviction behind the stock’s advance.

At Analyst Day, Williams also announced a new 340 megawatt Socrates the Younger power project and upsized its Aquila and Apollo projects, extending contract terms to 12.5 years.

The company now has $7.3 billion of fully contracted power innovation projects expected to generate about $1.4 billion of annual EBITDA by 2029.

CEO Chad Zamarin said the 10% plus growth target is “not an aspiration, but is a destination that is well charted,” underscoring management’s confidence in its contracted pipeline and power backlog.

See analysts’ growth forecasts and price targets for Williams Companies (It’s free) >>>

Is WMB Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 10.7%

- Operating Margins: 39.6%

- Exit P/E Multiple: 23.6x

Revenue is projected to rise from about $12.8 billion in 2026 to over $23.0 billion by 2030, driven by rising LNG exports, expanding power generation demand, and additional pipeline capacity across the Transco corridor.

The most important driver remains volume growth through contracted, fee-based infrastructure, where incremental throughput directly expands EBITDA without meaningful commodity exposure.

Operating margins approaching 40% reflect the fixed-cost nature of pipeline infrastructure and growing mix shift toward long-term take-or-pay contracts.

By 2030, more than 60% of EBITDA is expected to come from long-duration contracted revenue streams, improving earnings stability while growth accelerates.

Based on these inputs, the valuation framework implies a target price of $95, representing about 24% total upside from around $76 today.

With visible execution on pipeline expansions, LNG connectivity, and power innovation projects throughout 2026, Williams appears modestly undervalued if management delivers on its contracted growth roadmap.

Estimate a company’s fair value instantly (Free with TIKR) >>>

How Much Upside Does WMB Stock Have From Here?

Investors can estimate Williams Companies potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See Williams Companies true value, or any stock’s, in under 60 seconds (Free with TIKR) >>>