Key Stats for MPC Stock

- Year-to-Date Performance: 29%

- 52-Week Range: $115 to $216

- Valuation Model Target Price: $250

- Implied Upside: 19%

Value your favorite stocks like Marathon Petroleum with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Marathon Petroleum Corporation stock is up about 29% year to date, recently trading near $210 per share and holding close to the top of its $115 to $216 52-week range.

The rally reflects stronger-than-expected earnings, widening sour crude differentials, and growing confidence that refining margins can remain resilient into 2026.

The stock moved higher because the company delivered a clear earnings beat and reinforced its ability to capture strong refining economics.

Marathon reported Q4 adjusted EPS of $4.07 on approximately $3.5 billion of adjusted EBITDA. Refining utilization reached 95% in the quarter, and full-year margin capture came in at 105%.

Refining & Marketing generated $2 billion of Q4 adjusted EBITDA, while full-year cash flow from operations excluding working capital totaled $8.7 billion. High utilization, strong commercial execution, and improving heavy crude discounts supported the view that cash generation remains durable.

This week’s earnings call strengthened that narrative. CEO Maryann Mannen said the company “delivered results that underscore the strength of our business and the momentum ahead,” while outlining plans to invest about $700 million in 2026 refining capital, nearly 20% lower year over year.

Key Garyville projects are expected to increase crude throughput by 30,000 barrels per day and add 10,000 barrels per day of export-grade gasoline capacity by year-end 2027.

MPLX also announced $2.4 billion of growth capital focused on natural gas and NGL infrastructure and continues targeting 12.5% distribution growth, implying more than $3.5 billion of future annual cash distributions to MPC.

Institutional activity has remained active. Vestmark Advisory Solutions reduced its stake by 93.1%, while Rafferty Asset Management trimmed 7.4% and US Bancorp DE lowered its position by 4.6%. Vanguard trimmed 1.3% but still holds 38,344,677 shares worth about $7.39 billion, representing roughly 12.76% of the company.

At the same time, Mitsubishi UFJ Asset Management increased its stake by 2.4% to 610,186 shares valued at about $117.6 million, and Journey Advisory Group raised its position by 634.9%.

Institutional ownership stands near 76.77%, indicating continued large-cap sponsorship even as individual funds rebalance exposure.

See analysts’ growth forecasts and price targets for Marathon Petroleum (It’s free) >>>

Is MPC Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): (0.5%)

- Operating Margins: 6.1%

- Exit P/E Multiple: 12.9x

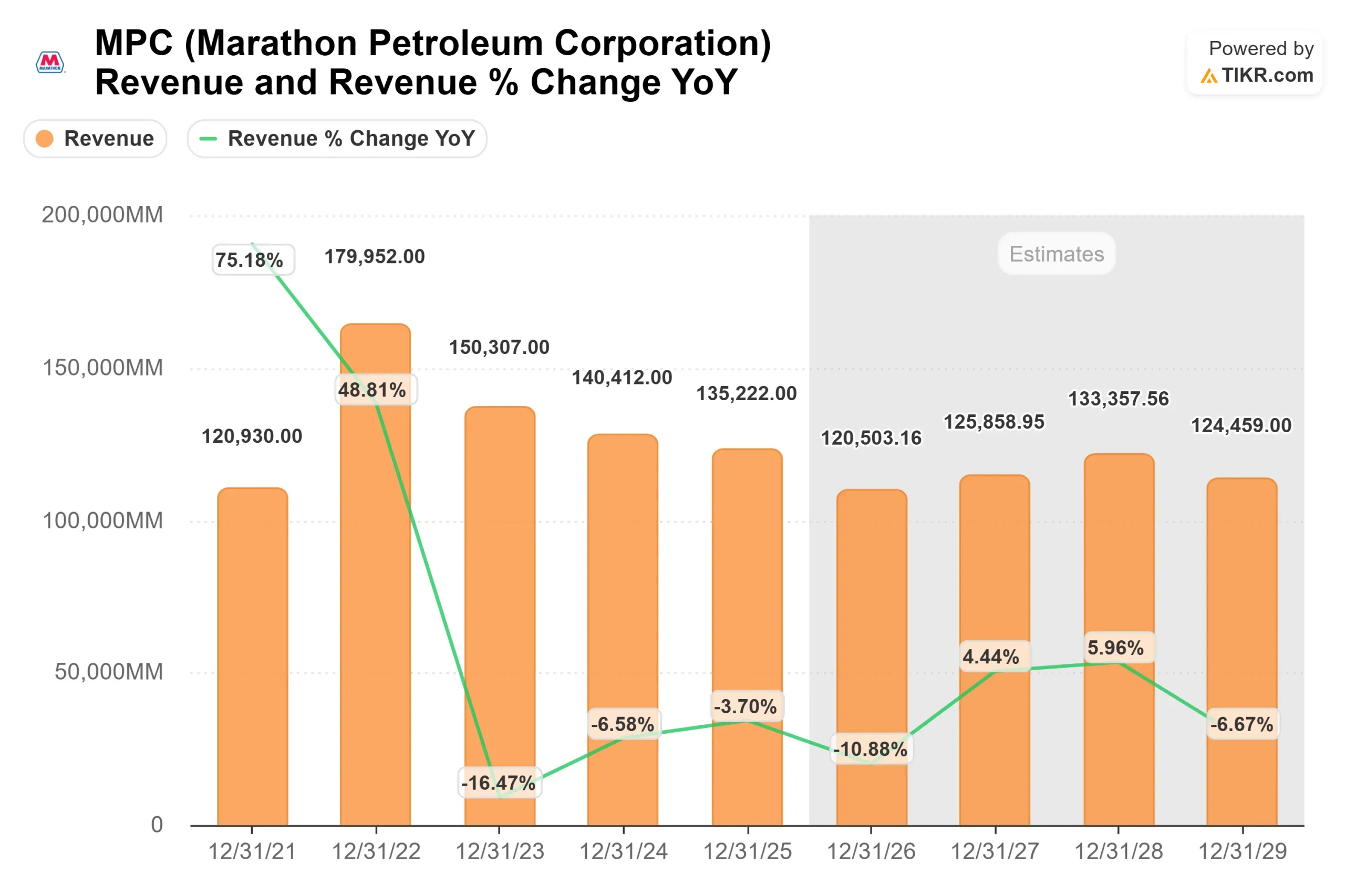

Revenue is expected to normalize following peak refining conditions, but the core investment case centers on margin durability rather than top-line expansion.

Marathon operates one of the most complex refining systems in North America, with approximately 50% of its crude slate tied to sour barrels.

When sour crude differentials widen by $1, management estimates roughly a $500 million annual earnings benefit, highlighting how feedstock flexibility can materially influence results.

Refining margin capture and utilization remain the key drivers for 2026. With refining capital spending reduced nearly 20% year over year and focused on value-enhancing upgrades, incremental investments are designed to improve reliability and expand high-value output rather than add speculative capacity.

Projects at Garyville and El Paso aim to increase throughput efficiency and export-grade gasoline production, strengthening product placement in global markets.

Midstream growth also supports the outlook. MPLX plans to invest $2.4 billion in growth capital in 2026, with 90% directed toward Natural Gas and NGL Services.

Distribution growth of 12.5% over the next two years implies more than $3.5 billion in annual cash distributions to MPC, which helps fund dividends, capital spending, and share repurchases.

At around $210 per share compared to a modeled value of $250, the stock implies roughly 19% upside based on normalized margin assumptions.

Performance in 2026 will largely depend on crack spread sustainability, sour crude differentials, export demand, and the company’s ability to convert high utilization into consistent free cash flow.

At current levels, Marathon Petroleum appears modestly undervalued, with future returns driven by refining margin structure and disciplined capital allocation rather than aggressive revenue growth.

Estimate a company’s fair value instantly (Free with TIKR) >>>

How Much Upside Does MPC Stock Have From Here?

Investors can estimate Marathon Petroleum potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See Marathon Petroleum true value, or any stock’s, in under 60 seconds (Free with TIKR) >>>