Key Stats for Sherwin-Williams Stock

- 52-Week Range: $302 to $380

- Current Price: $346

- Street Mean Target: $380

- Street High Target: $420

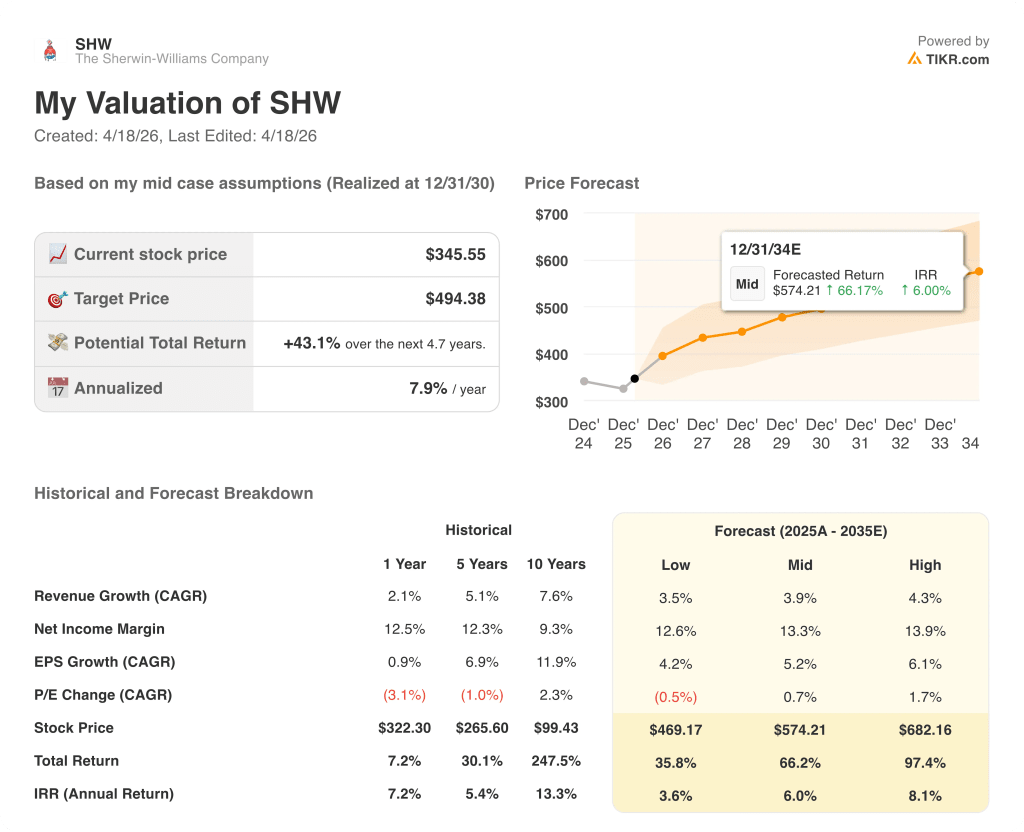

- TIKR Model Target (Dec. 2030): $494

What Happened?

Sherwin-Williams (SHW), whose stock has spent most of 2026 trading well below its 52-week high, delivered record full-year consolidated sales of $23.57 billion in 2025 even as demand stayed stubbornly weak across virtually every end market the company serves.

Fourth-quarter adjusted earnings per share came in at $2.23, beating the analyst consensus estimate of $2.16 and underscoring the company’s ability to extract margin even when volume refuses to cooperate.

The beat did not prevent a stock pullback: Sherwin-Williams’ 2026 full-year adjusted EPS guidance of $11.5 to $11.9 landed below the Street’s pre-announcement consensus of $12.42, sending shares lower on the report date.

What the initial reaction missed was the operating discipline underneath the guidance range, as the Paint Stores Group, which sells directly to professional painters through company-owned retail locations, expanded segment margin by 90 basis points in Q4 to 21% despite volume running down low single digits.

CEO Heidi Petz stated on the Q4 2025 earnings call that “for the third year in a row, the market is not going to give us much help — and for the third year in a row, we expect to outperform the market and grow sales and earnings per share,” signaling the share-gain playbook continues to work regardless of macro conditions.

The forward setup is built around three compounding drivers: a 7% price increase across the Paint Stores Group effective January 1 with low-single-digit realization embedded into guidance, 80 to 100 net new store openings planned for 2026, and a growing protective and marine pipeline tied to AI infrastructure and data center construction that Petz called a “boom” for coatings demand.

The Suvinil acquisition, completed in October 2025 and contributing $164.5 million to Consumer Brands Group sales in its first full quarter, opens a leadership position in Brazil that management is integrating using the same playbook that turned the 2017 Valspar acquisition into a margin contributor.

Wall Street’s Take on SHW Stock

The 2026 guidance miss reframed Sherwin-Williams stock as a show-me story, but the more accurate read is that three years of demand drought have obscured what the income statement is demonstrating: a company growing earnings faster than revenue in a tough tape, which is exactly what a high-quality compounder looks like before the cycle turns.

Sherwin-Williams’ normalized EPS compounded at 9.5% from 2023 to 2024 and an additional 1% in 2025 against a genuinely difficult volume backdrop, with consensus now projecting 3% growth to around $12 in 2026 before reaccelerating sharply to around 13% growth in 2027, a trajectory anchored directly by the store expansion program and the price increase realization already embedded in guidance.

Fifteen of 24 analysts covering SHW carry a buy or outperform rating, with 9 at hold and 1 at sell, and the mean price target of around $380 implies roughly 10% upside from current levels while the highest target of $420 signals real conviction among bulls that housing demand does not need to fully recover for the stock to rerate.

The spread between the $420 high and $268 low targets represents a genuine debate: bulls are pricing in eventual existing-home-sales normalization while the low target prices in another year of near-zero volume growth with no cycle recovery in sight.

Trading at roughly 29x forward 2026 earnings against a five-year historical range that stretched to 35x during prior growth years, and with 2027 EPS growth consensus running near 13%, Sherwin-Williams stock appears undervalued for investors with a 12- to 18-month horizon willing to wait for the housing catalyst that management itself is not currently budgeting for.

The signal worth watching: the 7% Paint Stores Group price increase is the sharpest in several years, and management’s guidance of low-single-digit realization is conservative given the explicit gross margin expansion commitment Petz reiterated on the call.

If raw material costs accelerate beyond the low-single-digit basket increase embedded in the 2026 guide, driven by tariff pressure on resins and non-TiO2 pigments that management specifically flagged, gross margin expansion guidance fails and the EPS midpoint becomes a ceiling.

Q1 2026 results on April 28 are the first real test: watch for price realization in Paint Stores Group, where even 50 basis points of incremental capture above guidance would trigger upward revisions to the full-year EPS range.

What Does the Valuation Model Say?

The TIKR mid-case model builds to a $494 target price using a 4% revenue CAGR and a ~13% net income margin assumption through 2030, implying a 43% total return and an 8% annualized IRR from the current price, a return profile built on margin assumptions the company’s own historical financials more than support.

At 29x forward earnings with a 13% EPS re-acceleration priced into 2027 consensus and a market-beating store expansion program running in the background, Sherwin-Williams stock is undervalued relative to what this business consistently delivers through adversity.

The central question for SHW investors is whether the “softer-for-longer” demand backdrop extends into a third or fourth year, because the valuation case does not require a housing recovery: it only requires the current operational playbook to keep working.

What Has to Go Right

- The 7% Paint Stores Group price increase achieves realization above the low-single-digit guidance assumption, driving upward revisions to 2026 EPS from the current consensus of around $12

- Protective and marine segment volumes compound as AI data center construction accelerates, with P&M already running at high-single-digit growth against a high single-digit prior-year comp in Q4 2025

- Suvinil contributes incremental Consumer Brands Group margin improvement as the Brazil integration matures through 2026 and into 2027, following the Valspar playbook management explicitly referenced on the call

- The 80-to-100 net new stores planned for 2026 maintain store productivity, adding approximately 1 point of organic revenue growth independent of any macro recovery

What Could Go Wrong

- Raw material costs exceed the low-single-digit basket increase in the 2026 guide, driven by tariff acceleration on resins and non-TiO2 pigments that management specifically identified as current pressure points

- Existing home sales remain near the low end of the wide industry forecast range, keeping residential repaint volumes flat-to-down and delaying the cycle recovery embedded in the 2027 EPS acceleration consensus expects

- The $85 million increase in interest expense from the new headquarters lease and the $1.1 billion delayed-draw term loan compresses EBT growth even if operating performance improves, capping the earnings upside bulls are currently pricing in

- The competitive environment Petz described as a “jump ball” intensifies as rivals pursue volume-focused pricing, limiting SHW’s ability to fully realize the January price increase and forcing a choice between margin and share

Should You Invest in The Sherwin-Williams Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SHW stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Sherwin-Williams Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SHW stock on TIKR for Free →